How OFWs Can Avoid Debt Traps Abroad

Working overseas gives many Filipinos the chance to earn higher income, support their families, and plan for a better future. Along with these opportunities come serious financial risks. Many Overseas Filipino Workers face financial trouble not because they lack income but because they struggle to manage money while abroad. Higher earnings can create false confidence, leading to overspending or borrowing without proper planning. Distance from family and pressure to provide can also influence financial decisions. Without clear budgeting and financial discipline, small money problems can quickly grow into long-term challenges.

OFW debt traps are among the most serious financial issues faced by Filipinos working overseas. These problems often begin with small loans for emergencies, placement costs, or family needs. At first, the debt seems manageable. Over time, interest, added fees, and repayment pressure increase the burden. Repeated borrowing to cover previous loans can quickly trap OFWs in a cycle that is difficult to escape and harmful to long-term financial stability.

This guide is written for real OFWs who want practical, realistic advice. It explains how OFW debt traps work, why they happen, and most importantly, how to avoid them while working abroad.

Understanding OFW Debt Traps

This section explains how OFW debt traps develop and why they are difficult to escape. It covers risky borrowing patterns, unfair loan conditions, and the unique pressures OFWs face abroad, helping readers understand how debt slowly builds and threatens long-term financial stability.

What Are OFW Debt Traps?

OFW debt traps occur when overseas workers become stuck in continuous borrowing that grows harder to escape over time. This often involves high-interest loans, repeated borrowing, or using new debt to pay existing obligations, which slowly drains income and limits financial stability abroad.

For many OFWs, the main issue is not borrowing itself but the loan conditions. These often include high interest, hidden charges, and repayment terms that require continuous overseas work. When new loans are used just to survive or send remittances, debt becomes a long-term trap.

Why OFWs Are More Vulnerable to Debt Traps

OFWs face financial pressures that make them more vulnerable than local workers. Distance from home adds emotional stress, while overseas living costs reduce savings. Income earned abroad can also create unrealistic expectations from family members, increasing the risk of borrowing.

Common factors that increase OFW debt risk include:

- Separation from family leading to emotional spending

- Pressure to send money home regularly

- Sudden job contract changes or termination

- Higher cost of living in host countries

- Limited access to fair financial institutions abroad

Earning income in foreign currency can give a false sense of financial security. Without careful planning, expenses rise quickly, savings shrink, and borrowing becomes an easy but dangerous solution that leads to long-term debt problems.

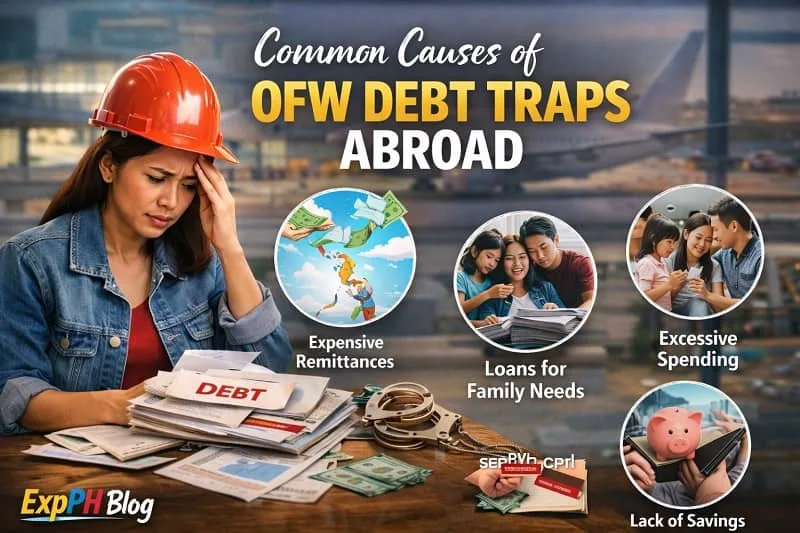

Common Causes of OFW Debt Traps Abroad

This section explains the main reasons OFWs fall into debt while working overseas. It covers risky lending practices, recruitment-related expenses, family financial pressure, and rising living costs abroad, helping readers understand how everyday situations can slowly lead to long-term debt problems.

High-Interest Loans from Informal Lenders

Many OFWs turn to informal lenders because approval is fast and requirements are minimal. These loans often come with very high interest and strict penalties. Some lenders operate within OFW communities and take advantage of urgent needs, especially during emergencies or sudden financial shortfalls.

Placement Fees and Recruitment-Related Debt

Some OFWs start working abroad already in debt due to placement fees, training costs, or processing expenses. When the job fails to meet income expectations, repayment becomes difficult. Lower earnings often push OFWs to borrow again, increasing the risk of falling into long-term debt traps.

Family Financial Dependence

Many OFWs feel a strong obligation to support extended family members, which can create ongoing financial pressure. Common responsibilities include:

- Paying off relatives’ debts

- Funding siblings’ education

- Covering medical expenses

- Supporting unemployed family members

Without clear boundaries and financial planning, these responsibilities can lead to repeated borrowing and growing debt.

Lifestyle Inflation Abroad

Higher income abroad can easily lead to higher spending. Some OFWs feel pressure to live comfortably or keep up with peers in high-cost countries. Expensive housing, new gadgets, and frequent leisure spending can quickly reduce savings and push workers toward debt.

Warning Signs That You Are Falling Into an OFW Debt Trap

This section highlights early warning signs that debt is becoming unmanageable for OFWs. It explains how repeated borrowing, heavy loan repayments, and avoiding financial records can signal growing financial stress that may lead to long-term debt problems if ignored.

You Are Borrowing to Pay Existing Loans

Using new loans to repay old ones is a serious warning sign. This pattern shows that your income can no longer cover current obligations. Over time, interest and penalties grow, making debt harder to manage and increasing the risk of long-term financial stress.

Most of Your Salary Goes to Debt Repayment

When most of your monthly salary is used to pay loans, saving becomes difficult. Emergency expenses may force you to borrow again. This cycle limits financial progress and keeps OFWs stuck managing debt instead of building stability abroad.

You Avoid Checking Your Loan Balances

Avoiding loan statements often signals stress or fear about finances. When OFWs stop tracking balances and due dates, problems grow unnoticed. Regular review helps you stay aware, plan repayments, and recognize early signs of falling into deeper debt.

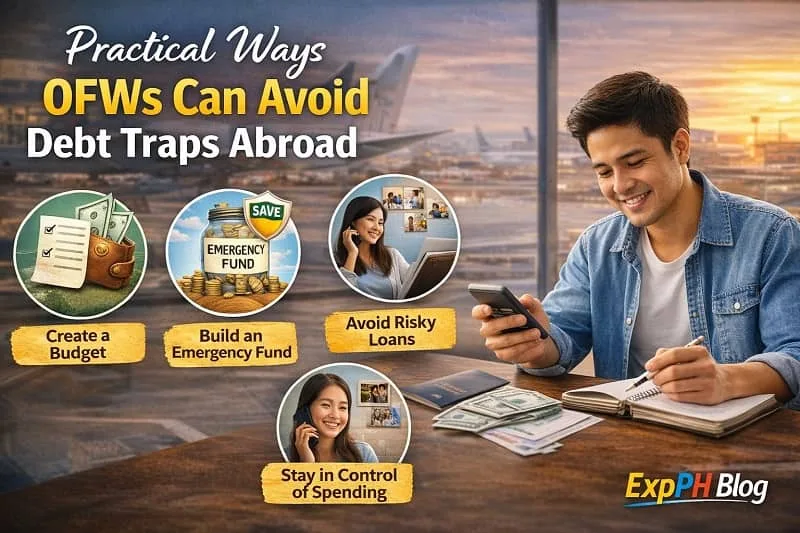

Practical Ways OFWs Can Avoid Debt Traps Abroad

This section provides practical steps OFWs can follow to stay financially stable while working overseas. It focuses on budgeting, emergency savings, and setting healthy financial boundaries with family to reduce borrowing, manage income wisely, and avoid falling into long-term debt problems.

Build a Clear Monthly Budget

Budgeting is the foundation of avoiding OFW debt traps. Every OFW should clearly track:

- Monthly income

- Fixed expenses

- Variable expenses

- Remittance amount

- Savings target

Even a simple budget helps identify spending leaks, control expenses, and prevent unnecessary borrowing while working overseas.

Create an Emergency Fund First

An emergency fund protects OFWs from unexpected expenses such as medical needs or job disruptions. Financial authorities like the Bangko Sentral ng Pilipinas stress saving to reduce reliance on high-interest debt. Building at least three months of basic expenses over time improves financial security abroad.

Set Boundaries With Family Financial Requests

Supporting family is important, but it should not damage your financial future. OFWs can manage this by:

- Setting a fixed remittance amount

- Explaining their budget honestly

- Avoiding loans for non-essential expenses

Clear communication helps prevent repeated borrowing, emotional stress, and long-term financial problems.

Smart Alternatives to Borrowing Abroad

This section highlights better financial choices that help OFWs avoid debt. It explains how increasing income through skill development and career growth reduces reliance on loans, strengthens financial stability, and creates safer long-term opportunities while working overseas.

Increase Income Instead of Borrowing

A practical way to avoid OFW debt traps is to focus on increasing income rather than borrowing. Improving earning capacity reduces financial pressure and builds long-term stability. OFWs can do this by:

- Gaining new skills

- Preparing for higher-paying roles

- Building career flexibility for future work

Using Skill Development to Reduce Debt Risk

Using skill development to reduce debt risk helps OFWs improve income without borrowing. Online learning platforms like Udemy offer courses in freelancing, digital skills, and business that OFWs can study during free time. These skills help qualify for better roles, prepare for career shifts, and build side income while maintaining long-term financial security abroad.

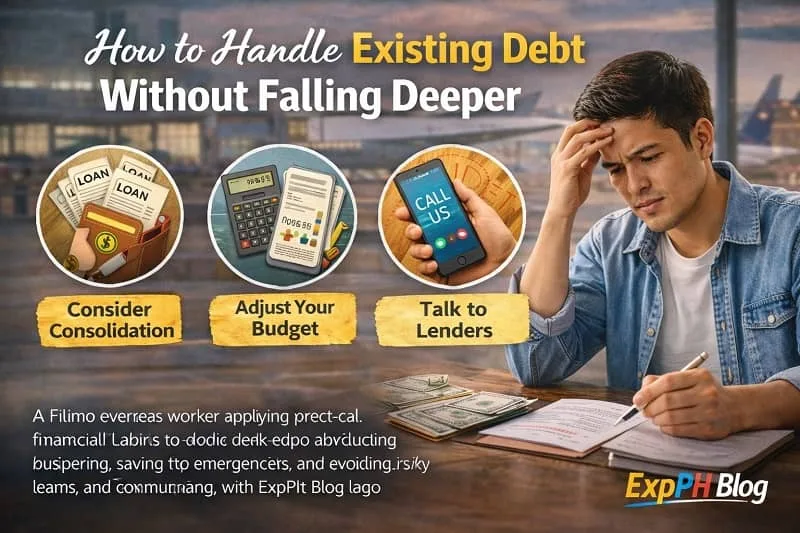

How to Handle Existing Debt Without Falling Deeper

This section guides OFWs on managing existing debt safely. It focuses on understanding all current loans, prioritizing high-interest payments, and avoiding misleading consolidation offers that can worsen financial stress and increase long-term debt instead of providing real relief.

List All Debts Honestly

Start by listing every debt you have to gain full clarity. Include the following details:

- Lender name

- Interest rate

- Monthly payment

- Remaining balance

Seeing the complete picture helps OFWs take control, plan repayments, and avoid making financial decisions based on stress or guesswork.

Prioritize High-Interest Debt

Focus on paying off loans with the highest interest first while continuing minimum payments on others. This approach reduces total interest paid over time and prevents balances from growing faster than your income can manage.

Avoid Loan Consolidation Scams

Some services claim to simplify debt but actually add higher fees. Always verify lenders, read contracts carefully, and avoid offers that promise instant relief. Legitimate solutions are clear, transparent, and never pressure OFWs into quick decisions.

Protecting Yourself From Financial Scams Abroad

This section helps OFWs recognize and avoid common financial scams while working overseas. It explains the importance of verifying lenders, being cautious with online loan apps, and protecting personal documents to prevent fraud, illegal borrowing, and serious financial losses abroad.

Verify Lenders and Contracts

Always read loan contracts carefully before signing. Check interest rates, fees, and repayment terms. When unsure, seek advice from trusted Filipino community groups or official labor offices. Careful review helps OFWs avoid unfair agreements that can lead to serious financial trouble.

Be Cautious of Online Loan Apps

Some online loan apps attract OFWs with quick approval and minimal requirements. Many hide high fees and strict penalties. Research the provider, read reviews, and understand all charges before applying to prevent falling into costly loan traps.

Keep Personal Documents Secure

Protect your personal documents at all times. Never share passport copies, work permits, or banking details with unverified lenders. Identity misuse can lead to fraud, illegal loans, and long-term financial problems that are difficult to resolve abroad.

Long-Term Financial Habits That Keep OFWs Debt-Free

This section focuses on habits that help OFWs stay financially stable over time. It highlights consistent saving, early planning for contract transitions, and financial education as key practices that reduce borrowing, build confidence, and protect overseas workers from long-term debt problems.

Save Consistently, Even in Small Amounts

Saving regularly builds strong financial habits for OFWs. Even small amounts add up over time and create a safety net. Consistent saving improves discipline, supports emergency needs, and reduces the urge to borrow during unexpected situations while working abroad.

Plan for Repatriation Early

Many OFWs struggle financially near contract endings due to lack of planning. Preparing early for repatriation or renewal helps manage expenses, protect savings, and avoid sudden borrowing. Clear plans reduce stress and support smoother transitions back home or into new contracts.

Focus on Financial Education

Learning how money works empowers OFWs to make better decisions. Basic knowledge of budgeting, saving, and debt management lowers financial risk. OFWs who prioritize financial education are more confident and far less likely to fall into long-term debt traps.

Conclusion: Staying Free From OFW Debt Traps Abroad

Avoiding OFW debt traps is not only about earning a higher income. It is about building discipline, planning carefully, and making informed financial decisions while working overseas. Many OFWs fall into debt because they focus only on earning and not on managing what they earn. Learning how to budget, track expenses, and understand loan risks helps prevent small financial issues from turning into long-term problems. Financial awareness allows OFWs to stay in control of their money, reduce stress, and make choices that support both present needs and future goals.

Debt can quietly take away years of hard work when it is ignored or poorly managed. By setting clear financial boundaries, building emergency savings, and choosing skill development over borrowing, OFWs can protect their income and stability. Every peso saved and every wise decision made abroad strengthens financial security. Over time, these habits create a safer path toward financial freedom and a better life for OFWs and their families back home.

Explore the related OFW financial guides below to deepen your understanding of money management abroad. These resources offer practical tips, real-life insights, and helpful checklists to support smarter financial decisions and long-term stability while working overseas for OFWs seeking clarity confidence security and better financial control.

- How OFWs Can Build a Stable Financial Routine Abroad

- How OFWs Can Prepare Financially Before Returning Home

- Balancing Family Support and Personal Savings the Smart Way

- Financial Checklists Filipinos Should Complete Before Returning Home

- Common Money Mistakes New Business Owners Must Avoid

FAQs About OFW debt traps

What are OFW debt traps and why are they common abroad?

OFW debt traps happen when repeated borrowing becomes hard to escape. They are common due to high expenses, family pressure, and limited access to fair loans.

Why do many OFWs rely on loans while working overseas?

Many OFWs borrow to cover emergencies, placement fees, or family needs. Without savings, loans feel like the fastest solution despite long-term financial risks.

How can budgeting help OFWs avoid debt traps abroad?

Budgeting helps OFWs track income and expenses clearly. It prevents overspending, supports regular savings, and reduces the need to borrow during unexpected situations.

What warning signs show an OFW is falling into a debt trap?

Warning signs include borrowing to repay loans, delayed payments, constant financial stress, and having little or no savings despite steady overseas income.

Is sending too much money home a risk for OFWs?

Yes, sending more than planned can reduce savings and cause borrowing. Setting a fixed remittance amount helps OFWs stay financially stable abroad.

How important is an emergency fund for OFWs overseas?

An emergency fund protects OFWs from sudden expenses like illness or job loss. It reduces reliance on high-interest loans during difficult situations.

Can skill development help OFWs avoid debt traps?

Yes, learning new skills can increase income opportunities. Higher earning potential reduces financial pressure and lowers the need to depend on loans abroad.

Are online lending apps safe for OFWs to use?

Some online lending apps charge high interest and hidden fees. OFWs should research carefully and avoid apps that lack transparency or proper regulation.

How can OFWs manage existing debt responsibly?

OFWs should list all debts, prioritize high-interest loans, pay consistently, and avoid borrowing again unless absolutely necessary to prevent deeper financial trouble.

What long-term habits help OFWs stay debt-free abroad?

Consistent saving, disciplined spending, financial education, and early planning for contract endings help OFWs maintain stability and avoid future debt problems.

Test your knowledge about How OFWs Can Avoid Debt Traps Abroad.

Results

#1. What is an OFW debt trap?

#2. Which habit helps prevent debt traps?

#3. Why do OFWs often borrow money?

#4. What is a major warning sign of debt trouble?

#5. Which fund reduces loan dependence?

#6. What increases debt risk abroad?

#7. How should OFWs handle family requests?

#8. What helps increase income safely?

#9. Which loans are most dangerous?

#10. What habit supports long-term stability?

Thank you for taking your time to learn with us.

Share your experience in the comments. Let us know which question made you think the most and what financial lesson you learned abroad.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Smart Ways to Survive an OFW Financial Emergency Abroad.

Pingback: 7-Step Emergency Fund for OFW Families Planning Tips Guide.