Balancing Family Support and Personal Savings the Smart Way

Balancing Family Support and Personal Savings is one of the most common financial struggles faced by Filipino families today, especially Overseas Filipino Workers. Many OFWs carry the responsibility of supporting parents, siblings, and extended relatives while also trying to secure their own future. The challenge becomes even harder when remittances consume a large portion of income, leaving little room for savings, investments, or personal goals.

This guide is written to help you approach this situation in a smarter and more sustainable way. Supporting your family does not mean sacrificing your own financial stability. At the same time, saving for yourself does not mean abandoning your loved ones. With the right mindset, clear systems, and practical strategies, it is possible to honor both responsibilities.

This article will walk you through realistic, culturally sensitive, and OFW-focused ways to balance Family Support and Personal Savings without guilt, burnout, or financial stress.

Understanding the Reality of Family Support and Personal Savings

Understanding the reality of Family Support and Personal Savings means recognizing the emotional, cultural, and financial pressures many Filipinos face. Supporting family is deeply valued, yet personal savings are essential for stability. A balanced approach helps protect your future while maintaining responsible and sustainable family support.

Why Family Support Is Deeply Rooted in Filipino Culture

Family support goes beyond money for many Filipinos. It reflects cultural values shaped by utang na loob, strong family bonds, and shared responsibility. For many OFWs, providing financial help feels like a moral duty, even when doing so puts pressure on their own finances.

This responsibility grows stronger when families depend on remittances for daily needs, schooling, healthcare, or emergencies. Refusing support may feel like betrayal. Understanding this emotional reality matters. The goal is not to stop helping family, but to manage support wisely while protecting long-term personal stability.

The Hidden Cost of Neglecting Personal Savings

When personal savings are repeatedly delayed, the long-term impact can be serious. Common outcomes include missing emergency funds, postponed retirement plans, rising debt, and financial vulnerability. Over time, this weakens financial security and increases stress during unexpected situations.

Ignoring savings today can lead to future dependence on the same family you once supported. This cycle is avoidable. Treating savings as a responsibility helps protect everyone involved. Balancing Family Support and Personal Savings is not selfish, it is a practical form of long-term care.

Setting Clear Financial Priorities Without Guilt

Setting clear financial priorities helps you support family without sacrificing your own stability. This section focuses on removing guilt from money decisions by defining limits, understanding real needs, and making thoughtful choices that protect both your future and your ability to help loved ones responsibly.

Redefining What Responsible Support Looks Like

Responsible family support does not mean giving away everything you earn. It means offering help that remains stable over time. This involves setting clear limits, fixed schedules, and realistic amounts that fit your income and long-term plans.

Support should be based on what you can truly afford after meeting your own needs. It should never be driven by pressure or comparison. A healthy approach to Family Support and Personal Savings begins with clarity and calm decisions.

Separating Needs From Wants

Many people struggle to separate essential support from optional spending. Essentials usually include food, utilities, basic education, and healthcare. Wants often cover lifestyle upgrades, new gadgets, and celebrations that are not financially urgent.

Meeting real needs is reasonable. Paying for wants while neglecting savings creates risk. Learning to say no to non-essential requests helps protect your finances and future stability.

Building a Smart Budget That Supports Both Sides

Building a smart budget helps balance Family Support and Personal Savings with clarity and control. By assigning clear roles to every peso, you reduce stress, avoid overspending, and make financial decisions with confidence. A well-structured budget supports your family today while protecting your long-term stability.

Creating a Dual-Purpose Budget System

A practical way to manage Family Support and Personal Savings is to use a dual-purpose budget. This system clearly separates funds meant for family support from money reserved for personal goals and future plans.

Income should be divided into clear categories such as support, savings, daily expenses, insurance, and personal growth. This structure shows limits early and reduces overspending. A written budget also limits emotional decisions because each peso already has a purpose.

Automating Savings Before Sending Remittances

Saving first before sending remittances is a powerful habit. Automating savings ensures your future is protected before money leaves your account. It also removes guilt because savings become a fixed responsibility like rent or utilities.

The Bangko Sentral ng Pilipinas emphasizes building savings and emergency funds for long-term stability, especially for OFWs facing income uncertainty. Prioritizing savings strengthens financial security for both you and your family.

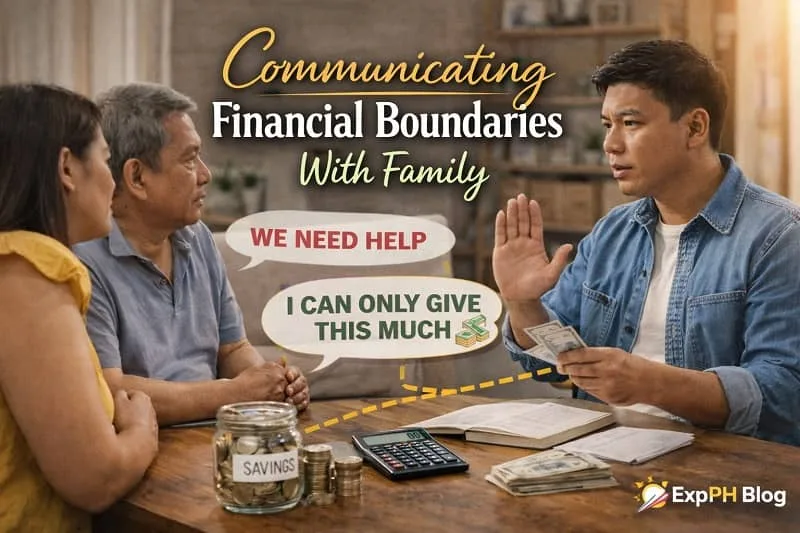

Communicating Financial Boundaries With Family

Clear communication helps balance Family Support and Personal Savings without harming relationships. This section explains why honest conversations matter and how setting respectful boundaries can reduce pressure, prevent misunderstandings, and protect long-term family harmony while supporting financial stability.

Why Honest Conversations Matter

Many challenges around Family Support and Personal Savings come from unclear expectations. Families may assume OFWs earn endlessly, especially when they do not see daily living costs abroad. This misunderstanding can create pressure and conflict over financial support.

Open conversations about income, expenses, and savings goals help set realistic expectations. You do not need to share every detail. Being honest about limits builds respect and reduces misunderstandings over time.

How to Say No Without Damaging Relationships

Saying no does not need to sound harsh or uncaring. It can be explained as a temporary limit or a change in how support is given. Offering budgeting help instead of cash is one example.

You can explain that saving now allows continued support later. This frames savings as shared protection rather than selfishness. Healthy boundaries reduce resentment and protect family relationships.

Strengthening Personal Savings While Supporting Family

Strengthening personal savings allows you to support your family without risking your own stability. This section highlights how emergency funds and long-term savings protect against unexpected events while ensuring you remain financially secure and capable of helping loved ones over time.

The Importance of Emergency Funds

Emergency funds play a vital role in balancing Family Support and Personal Savings. Without them, unexpected expenses quickly turn into financial stress and urgent problems that affect both you and your family.

Building three to six months of living expenses provides protection. This fund should stay separate from remittances and be used only for real emergencies. Having savings reduces the need for loans or emergency requests.

Saving for Long-Term Goals

Long-term savings include retirement, home ownership, and future business plans. These goals may seem far away, but starting early makes them realistic and less stressful to achieve over time.

Small and consistent contributions grow steadily. What matters most is discipline, not perfection. Strong long-term savings support your future independence and help you continue supporting family with confidence.

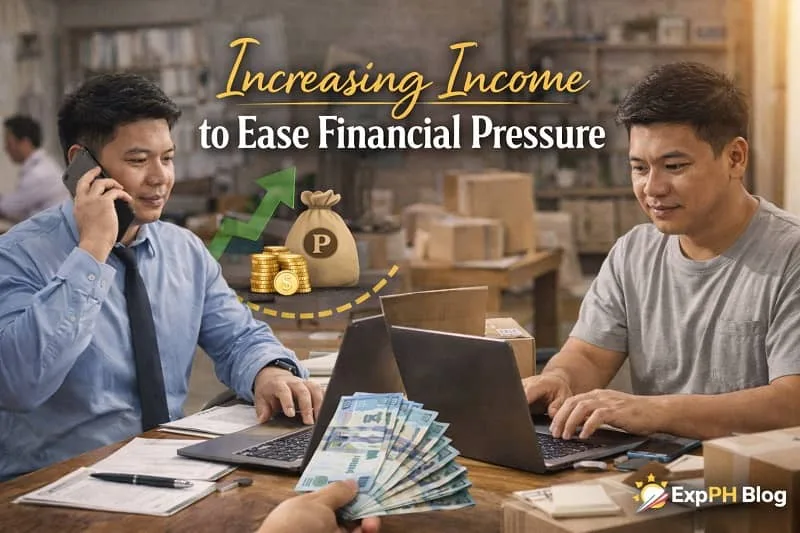

Increasing Income to Ease Financial Pressure

Increasing income provides breathing room when balancing Family Support and Personal Savings. This section explains why earning more matters and how income growth through skills and career development can reduce stress, improve stability, and support long-term financial goals for OFWs and their families.

Why Income Growth Matters in Family Support and Personal Savings

Sometimes financial strain comes from limited income rather than poor budgeting. Increasing income creates flexibility, making it easier to support family while still saving consistently. Higher earnings reduce stress and provide more room for emergencies, goals, and long-term financial planning.

For OFWs, income growth can come from promotions, job changes, freelancing, or skill development. Improving skills often produces better long-term results than working longer hours. Higher income allows support and savings to grow together without constant financial pressure.

Upskilling as a Long-Term Financial Strategy

Learning High-Income Skills for OFWs

Developing new skills is one of the smartest ways to strengthen Family Support and Personal Savings. High-income skills can lead to better roles, remote work, or side income. Digital skills, freelancing, project management, and online business offer opportunities beyond location limits.

Udemy is a useful platform for structured learning and practical skill building. Many OFWs use it to study in-demand skills at their own pace while working abroad. Learning new skills is an investment that can ease financial pressure for many years.

Helping Family Become Financially Independent

Helping family become financially independent reduces long-term pressure on both sides. This section focuses on empowering loved ones through skills, guidance, and income opportunities so support becomes sustainable, balanced, and less dependent on continuous financial assistance from you.

Teaching Instead of Always Sending Money

One sustainable way to balance Family Support and Personal Savings is to help family members manage money better. Teaching budgeting, saving, and simple income skills reduces long-term dependence and builds confidence.

This may include encouraging small businesses, side hustles, or improved spending habits. Support that builds skills and independence is stronger than constant financial assistance.

Supporting Income Opportunities at Home

Helping family start small income activities can gradually reduce the need for regular support. Options may include online selling, service work, or local micro businesses that match available skills.

Providing guidance and planning support matters more than money alone. Over time, family support shifts from constant help to occasional backup when truly needed.

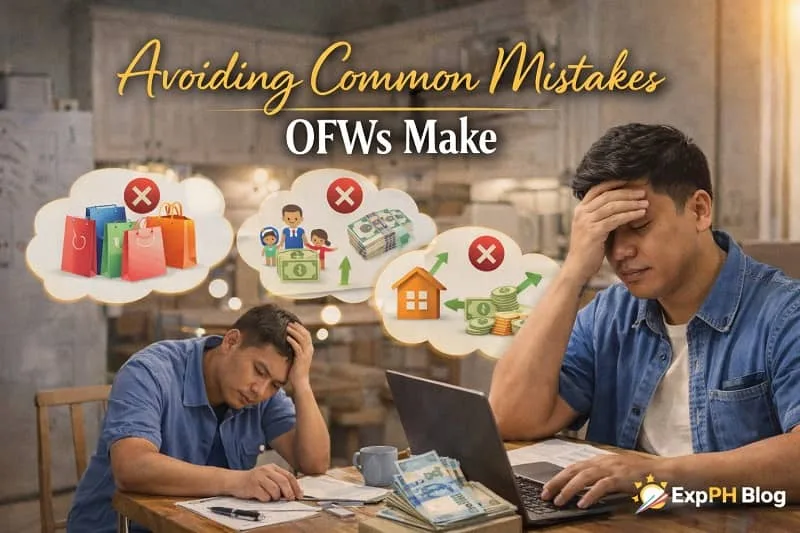

Avoiding Common Mistakes OFWs Make

Avoiding common financial mistakes helps OFWs maintain stability while supporting family. This section highlights risky habits that lead to stress and debt, and explains why flexible support, savings, and personal protection are essential for long-term financial balance and security.

Overcommitting to Support

One common mistake is committing to fixed support amounts that exceed your income. This often leads to debt, stress, and financial instability over time. Supporting family should not place your own future at risk.

Support amounts should remain flexible and reviewed regularly based on income and expenses. Sustainable support protects both the giver and the receiver while reducing long-term financial strain.

Ignoring Personal Financial Protection

Many OFWs focus on remittances while ignoring insurance, health coverage, and savings. This leaves them exposed during illness, job loss, or emergencies that require immediate financial resources.

Personal financial protection is part of responsible family support. When you are financially secure, you can continue helping others without risking your own stability.

Creating a Long-Term Balance Plan

Creating a long-term balance plan helps you manage Family Support and Personal Savings as life changes. This section focuses on regular financial reviews and future planning to ensure your support remains sustainable while protecting your own stability, goals, and financial independence over time.

Reviewing and Adjusting Regularly

Balancing Family Support and Personal Savings is an ongoing process, not a one-time choice. As income, family needs, and priorities change, your financial plan must adjust to remain effective and realistic.

Review your finances quarterly or annually to stay aligned with your goals. Regular adjustments help you respond to changes while maintaining stability and control over your finances.

Building a Future That Supports Everyone

The long-term goal is to support family without sacrificing your own security. This means building savings, investments, and income sources that provide stability through every life stage.

A balanced financial plan benefits you and the people who rely on you. When your future is secure, your support becomes stronger and more sustainable.

Conclusion: Choosing Smart Balance Over Sacrifice

Balancing Family Support and Personal Savings is one of the most valuable financial skills OFWs can build over time. It requires awareness, discipline, and thoughtful decision-making. Supporting your family should not come at the cost of your own future security. In the same way, saving for yourself does not mean turning away from your responsibilities. A healthy balance allows you to care for loved ones while protecting your long-term stability and peace of mind.

By setting clear boundaries, following a realistic budget, improving income through skill development, and planning ahead, both goals can exist without conflict. When support and savings work together, financial stress decreases and confidence grows. Smart balance, not constant sacrifice, leads to lasting stability and stronger family support.

If you want to deepen your financial knowledge, the following guides may also help.

- How OFWs Can Build Savings Even With Family Obligations

- Simple Financial Systems Small Businesses Should Set Up Early

- Financial Checklists Filipinos Should Complete Before Returning Home

- How to Start Investing with Just ₱1,000 in the Philippines

- How to Set Realistic Financial Goals for 2026

FAQs About Family Support and Personal Savings

What does balancing family support and personal savings really mean?

Balancing family support and personal savings means helping loved ones financially while consistently setting aside money for emergencies, goals, and long-term security without guilt pressure.

How can OFWs balance family support and personal savings effectively?

OFWs should save first, set clear remittance limits, communicate honestly with family, and review budgets regularly to avoid debt, burnout, and long-term financial instability risks.

Why is personal savings important even when supporting family?

Supporting family is important, but ignoring personal savings can lead to emergencies, dependence, and stress later, which may ultimately burden the same family you support.

What is a good budget setup for family support and personal savings?

A good budget separates family support, savings, expenses, and protection, ensuring money has clear purpose and limits, reducing emotional spending and financial conflicts over time.

How can I set financial boundaries with my family respectfully?

Set boundaries calmly, explain financial goals, share realistic limits, and emphasize sustainability so family understands your support continues longer when finances are balanced and stable.

Why are emergency funds critical for OFWs?

Emergency funds protect both you and your family by covering unexpected costs without loans, missed remittances, or panic-driven decisions during difficult situations and stressful times.

How does skill development help with family support and personal savings?

Improving skills increases income potential, making it easier to support family consistently while growing savings, reducing reliance on overtime or constant financial sacrifices and stress.

Can helping family become financially independent reduce pressure?

Yes, encouraging budgeting, side income, or small businesses helps family become self-reliant, gradually reducing financial pressure on you while strengthening household stability and long-term resilience.

What common mistakes should OFWs avoid when supporting family?

Common mistakes include overcommitting to remittances, skipping savings, avoiding boundaries, and assuming income abroad is unlimited, leading to debt and emotional strain over time periods.

How can I maintain long-term balance between family support and savings?

Long-term balance comes from clear priorities, disciplined saving, honest communication, income growth, and regular financial reviews that adapt to changing family needs and life stages.

Test your understanding of smart money habits, boundaries, and long-term planning.

Results

#1. What is the main goal of balancing family support and personal savings?

#2. Why should OFWs prioritize personal savings?

#3. What budgeting method helps manage family support better?

#4. What should be done before sending remittances?

#5. Why are financial boundaries important with family?

#6. What type of fund protects against emergencies?

#7. How can OFWs reduce long-term financial pressure?

#8. What approach helps family rely less on remittances?

#9. What is a common mistake when supporting family?

#10. What ensures long-term balance between support and savings?

Thank you for taking the time to test your knowledge.

We would love to hear from you. Please comment below and share your quiz experience, score, or personal insights with the ExpPH Blog community.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Powerful Benefits of Cashless Payments in the Philippines.