How OFWs Can Maintain Discipline With Money Abroad

Living and working overseas is never easy. Every Overseas Filipino Worker carries more than luggage at the airport. You carry responsibility, expectations, and the strong desire to build a better future for your family. The sacrifices include long hours, homesickness, and missed milestones. Because of this, every peso you earn represents effort and emotional strength. Your income abroad is not just money. It is a symbol of commitment and hope for long-term stability.

However, earning abroad does not automatically guarantee financial security. A high salary can disappear quickly without proper planning and control. This is why OFW money discipline is essential while working overseas. Discipline is not about being overly strict or denying yourself comfort. It means being intentional with spending, tracking where your hard-earned money goes, making wise decisions, and protecting the future you are working so hard to build.

In this guide, you will learn practical and realistic strategies that help OFWs stay financially disciplined abroad. Whether you are new to overseas work or already experienced, these principles can strengthen your financial foundation and protect your long-term goals.

Table of Contents

Understanding OFW Money Discipline

Before discussing techniques and strategies, we must clearly understand what OFW money discipline truly means. It refers to managing income with intention, controlling spending, setting financial priorities, and making responsible decisions even when facing temptation, pressure, or emotional situations while working abroad.

For OFWs, money discipline involves practical and consistent financial habits such as:

- Managing remittances properly

- Avoiding lifestyle inflation

- Saving consistently

- Investing wisely

- Preparing for retirement or business

These actions create structure and direction for every peso earned overseas.

OFW money discipline is not simply about saving larger amounts each month. It focuses on building lasting financial stability that continues even after your overseas contract ends, allowing you to return home with security, confidence, and clear long-term financial direction.

Why OFW Money Discipline Is Harder Abroad

Working abroad comes with challenges that can weaken even strong financial habits. Different environments, higher salaries, and social pressures influence spending behavior. Understanding these realities allows you to build stronger systems that protect your income and strengthen long-term OFW money discipline.

Emotional Pressure and Family Expectations

Many OFWs feel deep responsibility to provide for their families. Relatives may request financial support for tuition, medical needs, celebrations, or non-essential expenses. Without clear limits and structured agreements, repeated requests can reduce savings and slowly weaken financial stability.

Lifestyle Inflation

Higher income abroad often leads to higher spending. It becomes tempting to:

- Upgrade gadgets frequently

- Send extra money without planning

- Buy branded items regularly

- Eat out more often

When income rises without control, expenses increase at the same pace.

Easy Access to Loans and Credit

In many countries, financial institutions offer convenient borrowing options such as:

- Credit cards

- Salary loans

- Installment plans

Easy approval can create a false sense of affordability. Without careful budgeting and discipline, debt can accumulate quickly and reduce your ability to save consistently.

Building a Strong Foundation for OFW Money Discipline

Strong OFW money discipline begins with structure and clarity. Without a clear system, income can easily disappear through daily spending and unexpected requests. A solid foundation helps you stay focused, protect your savings, and align every financial decision with your long-term goals.

Create a Clear Financial Vision

Start by asking yourself important questions:

- Why did I go abroad?

- What is my five-year plan?

- Do I want to build a house, start a business, or retire early?

Clear purpose makes discipline easier. You are not saving randomly but working toward meaningful goals. Write them down and make them specific and measurable.

Instead of saying, “I want to save money,” define a concrete target. For example, “I will save 500,000 pesos in three years for a small business.” Specific goals create direction, motivation, and stronger financial commitment.

Separate Needs, Wants, and Pressure Spending

To improve OFW money discipline, classify your expenses honestly.

Needs:

- Rent

- Food

- Utilities

- Essential remittances

Wants:

- Latest phone

- Branded clothing

- Luxury items

Pressure spending:

- Unplanned financial support

- Repeated family requests

- Social events beyond budget

When expenses are categorized clearly, you gain better control and understand exactly where your income goes each month.

Create a Structured Budget System

A structured budget protects your income and supports long-term OFW money discipline. It is not a restriction but a guide that ensures every peso has a purpose. With a clear system, you reduce waste, prevent confusion, and make confident financial decisions each month.

Use the 50-30-20 Rule Adapted for OFWs

You can adjust this rule based on your responsibilities and goals:

- 50 percent for essentials and remittances

- 30 percent for savings and investments

- 20 percent for personal spending

If you aim to grow savings faster, consider:

- 50 percent essentials

- 40 percent savings

- 10 percent lifestyle

Consistency matters more than perfection.

Track Every Remittance

Many OFWs forget the exact total they send home each month. Tracking prevents misunderstandings and helps you stay within budget. Use a simple spreadsheet and record:

- Date

- Amount sent

- Purpose

- Total monthly remittance

Regular tracking increases awareness, strengthens control, and reinforces strong OFW money discipline over time.

Automate Savings to Remove Temptation

Strong OFW money discipline becomes easier when systems reduce daily decision-making. Automation removes temptation and limits emotional spending. When savings happen automatically, you rely less on willpower and more on structure, which strengthens consistency and long-term financial stability.

Set Automatic Transfers

If your bank allows it, arrange automatic transfers and follow these steps:

- Transfer a fixed salary portion

- Keep savings in another account

- Separate spending and savings funds

When money moves immediately into savings, you are less likely to spend it impulsively.

Use Dedicated Savings Accounts

Open separate accounts for specific goals:

- Emergency fund

- Business fund

- Retirement fund

Dividing accounts creates clarity and purpose. You clearly see progress for each goal, avoid confusion, and protect funds from accidental spending or unnecessary withdrawals.

Build a Strong Emergency Fund

A strong emergency fund is a core part of OFW money discipline. It protects your family from sudden financial stress and gives you peace of mind while working abroad. With savings prepared for unexpected events, you can make calm and rational decisions.

Why OFWs Need a Bigger Safety Net

OFWs face risks that local workers may not experience, including:

- Contract termination

- Employer disputes

- Visa problems

- Health emergencies

The Department of Migrant Workers advises OFWs to understand employment risks and contract terms before deployment. You can review official guidance at https://dmw.gov.ph/. Preparation reduces vulnerability and strengthens financial confidence.

This guidance is not meant to create fear. It encourages awareness and readiness. When you understand potential risks, you plan better and avoid financial panic during difficult situations abroad.

How Much Should You Save?

Set clear emergency fund targets:

Minimum target:

- Three to six months of expenses

Safer target for OFWs:

- Six to twelve months

This level of preparation improves OFW money discipline because decisions are based on strategy rather than urgency or fear.

Control Remittance Expectations

Managing remittance expectations is one of the most challenging parts of OFW money discipline. Many workers feel emotional pressure to give more than planned. Without clear boundaries, savings goals become difficult to achieve and financial stress increases over time.

Set Clear Family Agreements

Before sending monthly support, establish simple and clear agreements:

- Decide on a fixed amount

- Clarify covered expenses

- Avoid open-ended promises

Instead of saying, “Tell me if you need money,” state, “I will send 20,000 pesos monthly for bills and tuition.” Clear communication prevents confusion and protects your budget.

Avoid Becoming the Family Bank

Supporting family is honorable, but unlimited financial access can create dependency. Healthy OFW money discipline includes guiding loved ones toward responsibility. Encourage them to:

- Work if capable

- Follow a household budget

- Avoid unnecessary debt

Your financial discipline should inspire better money habits at home.

Strengthen OFW Money Discipline Through Skill Investment

Increasing income wisely can strengthen OFW money discipline. When you grow your earning potential, financial pressure decreases and savings become easier to maintain. Skill investment allows you to build long-term stability instead of depending only on your current overseas contract.

Upgrade Your Skills for Higher Income

Rather than spending extra money on temporary rewards, invest in knowledge that improves your income capacity. Consider learning practical skills such as:

- Freelancing

- Digital marketing

- Coding

- Project management

- Language proficiency

These skills can open remote work or promotion opportunities.

Many OFWs explore affordable online courses through platforms like Udemy to upgrade their abilities. Skill development builds personal assets that generate income beyond your overseas job. The goal is not to collect certificates but to gain practical abilities that create real earning opportunities.

Avoid Debt Traps Abroad

Debt can erase years of sacrifice if handled carelessly. Many OFWs fall into financial trouble not because of low income but because of unmanaged borrowing. Strong OFW money discipline requires careful evaluation before using credit or accepting loan offers abroad.

Be Careful With Credit Cards

Credit cards are financial tools, not additional income. Used properly, they offer convenience. Used carelessly, they create long-term debt. If you decide to use one, follow these rules:

- Pay full balance monthly

- Avoid minimum payments

- Do not fund impulse buys

Unpaid balances grow quickly due to interest charges.

Think Twice Before Taking Loans

Before applying for any loan, pause and evaluate your purpose. Ask yourself:

- Is this for an asset?

- Will income increase?

Borrowing for investment may be strategic. Borrowing for lifestyle or image often creates unnecessary financial pressure.

Develop Daily Habits That Support OFW Money Discipline

Long-term financial success does not happen overnight. It is built through small daily actions repeated consistently. Strong OFW money discipline grows when simple habits guide your spending decisions and keep you focused on your financial priorities.

Practice Conscious Spending

Before making any purchase, pause and reflect. Ask yourself:

- Do I truly need this?

- Does this match my goals?

- Will I regret this later?

This short evaluation reduces impulse buying and protects your savings from unnecessary expenses.

Review Your Finances Monthly

Set aside time each month to evaluate your financial position. Check the following:

- Total income

- Total expenses

- Savings rate

- Debt balance

Regular reviews strengthen awareness and allow early correction before small problems become serious financial setbacks.

Plan for Life After Your Overseas Contract

OFW money discipline should focus not only on present needs but also on your long-term future. Overseas work is often temporary. Planning early ensures you return home with financial stability instead of uncertainty or dependence on extended contracts.

Build an Exit Plan

Create a clear roadmap for life after working abroad. Ask yourself:

- When will I return home?

- What income source will support me?

Possible exit strategies include:

- Small business

- Rental properties

- Online freelancing

- Investments

Without preparation, savings may fall short and contract extensions become necessary.

Start Retirement Planning Early

Retirement may feel distant, but early preparation offers strong advantages. Time allows your money to grow steadily and reduces financial stress later. Consider building long-term security through:

- Government programs

- Private investments

- Insurance with savings features

Starting early strengthens financial confidence and reduces future pressure.

Protect Your Money From Emotional Decisions

Financial decisions made during stress often lead to regret. Strong OFW money discipline requires calm thinking and clear boundaries. When emotions control spending, savings and long-term plans can suffer. Learning to pause before reacting protects both your income and your peace of mind.

Avoid Sending Money During Guilt Moments

Family members may sometimes say:

- “You earn a lot there.”

- “Life is harder here.”

Listen with empathy and respect their situation. However, make financial decisions based on your budget and goals. Logical planning should guide remittances, not guilt or pressure.

Do Not Compare With Other OFWs

You may see posts showing:

- Expensive vacations

- New cars

- Designer items

Social media rarely reveals debt or hidden struggles. Focus on your own progress. True OFW money discipline is steady, private, and built on consistent smart decisions.

Create Multiple Income Streams

Depending on one salary increases financial risk, especially for OFWs working under contracts. Building additional income sources strengthens OFW money discipline by reducing pressure on your primary job and increasing long-term security. Diversified income creates flexibility and improves financial confidence.

Explore Side Opportunities

Consider practical income options such as:

- Online freelancing

- Digital services

- Small family business support

- Online selling

Extra income can:

- Accelerate savings goals

- Reduce financial stress

- Increase flexibility

However, protect your health and rest. Financial discipline also requires balance and sustainable work habits.

Maintain Mental and Emotional Discipline

Strong OFW money discipline is closely linked to emotional stability. When stress builds, financial decisions can become impulsive. Managing your mental well-being helps you stay focused on long-term goals and prevents short-term emotions from damaging years of hard work.

Avoid Burnout Spending

After demanding workweeks, rewarding yourself with expensive purchases may feel justified. However, repeated stress spending can weaken savings. Consider healthier alternatives such as:

- Regular exercise

- Video calls with family

- Personal hobbies

These activities refresh your mind without harming your finances.

Stay Connected to Your Purpose

Remind yourself why you chose to work abroad. Write a simple message and place it somewhere visible, such as, “I am working abroad to secure my family’s future.” Clear purpose strengthens focus, improves resilience, and supports consistent financial discipline.

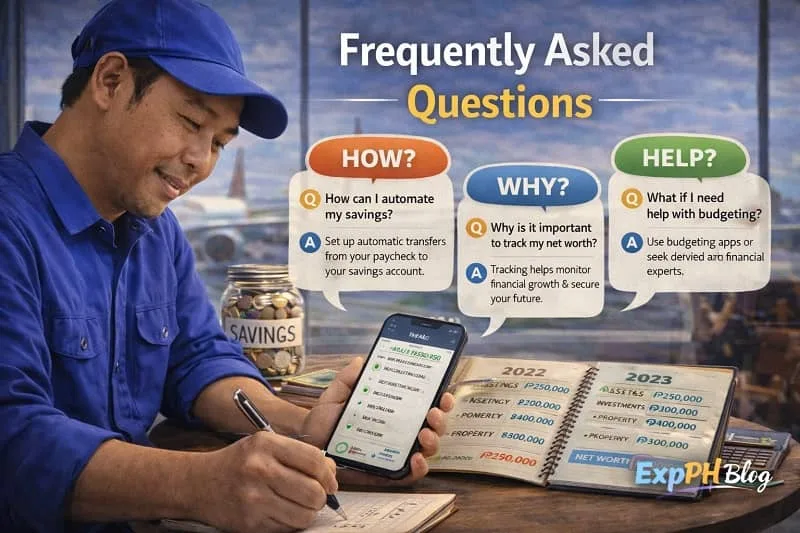

Track Your Net Worth Annually

Many OFWs monitor monthly income yet overlook overall financial position. Strong OFW money discipline requires measuring total progress, not just salary and expenses. Reviewing net worth each year provides a clear picture of growth and highlights areas that need improvement.

Net worth is calculated as:

- Total assets

- Minus total liabilities

To track progress annually, review:

- Savings

- Investments

- Property

- Debts

Watching your net worth grow builds motivation, strengthens accountability, and reinforces consistent financial discipline over time.

Build Financial Knowledge Continuously

The financial world changes quickly, and OFWs must keep learning to stay prepared. Strong OFW money discipline depends on updated knowledge and informed decisions. Continuous learning helps you adapt to new opportunities, avoid costly mistakes, and protect your income abroad.

Focus on learning topics such as:

- Budgeting

- Investments

- Business

- Taxes

Financial knowledge reduces fear and builds confidence. When you understand how money works, you make smarter decisions and manage risks more effectively.

Common Mistakes That Break OFW Money Discipline

Even hardworking OFWs can weaken their financial progress through repeated mistakes. Recognizing these patterns helps protect your income and strengthen long-term OFW money discipline. Awareness allows you to correct habits before they become serious financial problems.

Common pitfalls include:

- Increasing remittances without a budget

- Ignoring emergency savings

- Taking loans for lifestyle

- Skipping retirement planning

- Delaying investments

- Avoiding financial tracking

If you notice any of these behaviors, do not feel discouraged. Awareness is the first step toward improvement and stronger financial discipline.

Final Thoughts on OFW Money Discipline

Working abroad requires courage, patience, and deep sacrifice. Every peso you earn represents time away from family, missed milestones, and emotional strength. That is why OFW money discipline is essential, not optional. Discipline protects your hard work and secures your family’s future. It transforms temporary overseas employment into long-term financial stability. Without discipline, income can disappear quickly. With discipline, each month abroad becomes a step toward freedom and lasting security.

You do not need perfection to succeed. You need consistency. Start with one simple habit today such as tracking expenses, automating savings, setting clear remittance boundaries, or upgrading your skills. Small actions repeated regularly produce meaningful progress. Your journey as an OFW deserves more than income alone. It deserves stability, confidence, and long-term peace of mind. Stay focused on your goals and trust that steady discipline will reward you in the future.

At ExpPH Blog, our mission is to guide OFWs toward financial stability through practical and realistic strategies.

Find more learning options in the links below.

- How OFWs Can Build Multiple Income Streams Safely

- Income Diversification Ideas That Do Not Require Big Capital

- Simple Financial Systems Small Businesses Should Set Up Early

- How OFWs Can Handle Financial Emergencies From Abroad

- Emergency Fund Planning for Families With OFWs

Frequently Asked Questions

1. What is OFW money discipline?

OFW money discipline means managing income wisely abroad, controlling spending, prioritizing savings, and making consistent financial decisions that support long-term security and family stability goals.

2. Why is money discipline important for OFWs?

Money discipline protects hard-earned income, prevents unnecessary debt, builds savings, and ensures overseas sacrifices translate into lasting financial security and stability for families.

3. How can OFWs avoid overspending abroad?

OFWs can avoid overspending by creating a clear budget, tracking expenses monthly, limiting impulse purchases, and aligning every financial decision with long-term goals.

4. How much should OFWs save monthly?

Ideally, OFWs should save at least 30 percent of income, but higher savings rates improve financial security and accelerate progress toward long-term goals.

5. What is the best way to manage remittances?

Set a fixed monthly remittance amount, clarify family expenses, track transfers carefully, and avoid sending extra funds without proper discussion and budgeting.

6. How can OFWs build a strong emergency fund?

OFWs should save six to twelve months of expenses in a separate account to protect against job loss, medical emergencies, or unexpected financial challenges.

7. Should OFWs use credit cards abroad?

OFWs can use credit cards responsibly by paying balances in full monthly, avoiding minimum payments, and never using credit for unnecessary purchases.

8. How can skill development improve financial discipline?

Investing in new skills increases earning potential, creates additional income streams, and supports long-term financial stability after overseas contracts end.

9. What common mistakes weaken OFW money discipline?

Common mistakes include lifestyle inflation, uncontrolled remittances, lack of budgeting, excessive debt, and failing to plan for retirement or future income sources.

10. How can OFWs stay motivated financially?

OFWs stay motivated by remembering their purpose, tracking financial progress regularly, setting realistic goals, and celebrating small milestones toward long-term financial freedom.

Learning Hub

Test your understanding of How OFWs Can Maintain Discipline With Money Abroad.

Results

#1. What is the main goal of OFW money discipline?

#2. What should OFWs build first?

#3. How many months of expenses should OFWs save for emergencies?

#4. What weakens money discipline?

#5. What helps control overspending?

#6. What is a smart credit card habit?

#7. Why should OFWs track remittances?

#8. What supports long-term financial stability?

#9. What protects against job loss?

#10. What strengthens daily money discipline?

Thank you for taking the quiz

If you are an OFW, we would love to hear your experience. What money habit helped you the most abroad? Share your journey in the comments and inspire fellow kababayans.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.