Emergency Fund Planning for Families With OFWs

For many Overseas Filipino Workers, working abroad is a sacrifice made for family security, stability, and long-term goals. While regular remittances help cover daily needs, one unexpected event can quickly disrupt a family’s finances. Medical emergencies, sudden job loss, delayed salaries, or global crises can instantly affect income flow. This is why building an emergency fund for OFW families is not optional. It is a financial safety net that protects both the OFW abroad and the loved ones at home.

Emergency fund planning is not just about saving money. It helps create peace of mind, reduce stress during crises, and prevent debt traps that many OFW families experience. This guide explains how OFW families can realistically build, manage, and protect an emergency fund that works in real life, not just on paper.

Why Emergency Fund Planning Is Critical for OFW Families

OFW families face financial risks that local households rarely experience. Distance, overseas contracts, currency changes, and global events can quickly disrupt income. An emergency fund for OFW families provides financial protection when remittances are delayed, employment becomes uncertain, or sudden expenses arise unexpectedly.

Common Financial Risks Faced by OFW Families

OFW households are exposed to several financial challenges that can affect stability and daily living:

- Sudden termination or non renewal of overseas contracts

- Delayed or reduced remittances due to employer or banking issues

- Medical emergencies involving the OFW or family members in the Philippines

- Natural disasters such as typhoons, floods, or earthquakes

- Exchange rate fluctuations reducing remittance value

- Unexpected travel costs for emergency return

Without an emergency fund, many families turn to loans, pawned assets, or high-interest credit. These short-term solutions often lead to long-term financial strain and make recovery more difficult after a crisis.

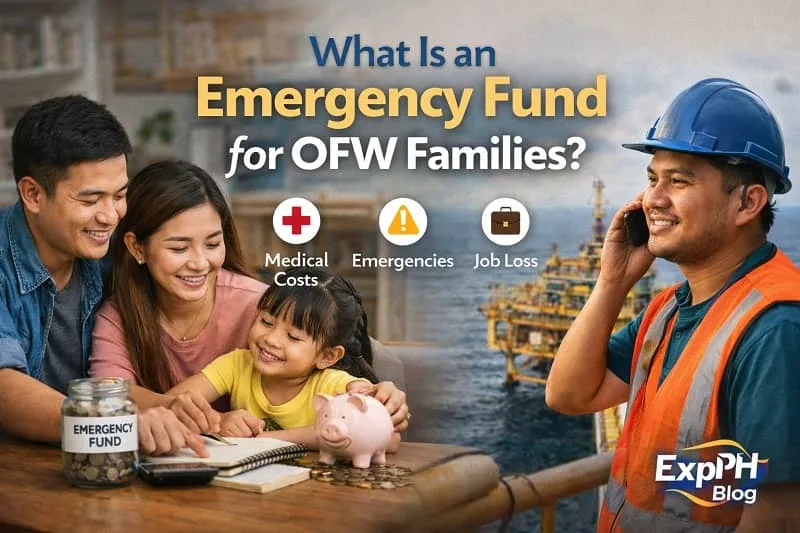

What Is an Emergency Fund for OFW Families?

An emergency fund is money set aside only for urgent and unexpected expenses. It is not meant for planned spending, celebrations, or investments. For OFW households, an emergency fund for OFW families must cover risks both overseas and in the Philippines.

What Qualifies as a Real Emergency?

A real emergency involves sudden situations that require immediate financial support and cannot be delayed:

- Job loss or contract suspension

- Major home repairs caused by disasters

- Hospitalization or medical treatment

- Emergency travel and documentation costs

- Immediate family crises needing urgent cash

What Does NOT Count as an Emergency?

These expenses should be planned separately and must not be taken from the emergency fund:

- Tuition that was already planned

- Gadgets, appliances, or upgrades

- Vacations or leisure travel

- Business expansion costs

- Lifestyle upgrades

Clear and consistent rules help protect the emergency fund from misuse and ensure it is available when truly needed.

How Much Emergency Fund Should OFW Families Have?

The right emergency fund amount depends on monthly household expenses, number of dependents, and income stability. Because overseas work carries higher risk, OFW families need a larger financial buffer to manage income gaps and unexpected emergencies without financial pressure.

General Emergency Fund Rule for OFW Families

Most experts recommend saving three to six months of essential expenses. However, OFW families are safer with six to nine months of coverage. Overseas income can stop without warning, and finding new work or income replacement often takes more time.

How to Compute Your Target Amount

Start by listing only essential monthly expenses needed for daily living:

- Food and groceries

- Rent or housing payments

- Utilities and internet

- School essentials

- Medical maintenance

- Transportation

Add the total monthly expenses and multiply it by your target number of months.

Example:

If monthly essentials total PHP 35,000

Six months equals PHP 210,000

Nine months equals PHP 315,000

This final amount becomes your emergency fund goal.

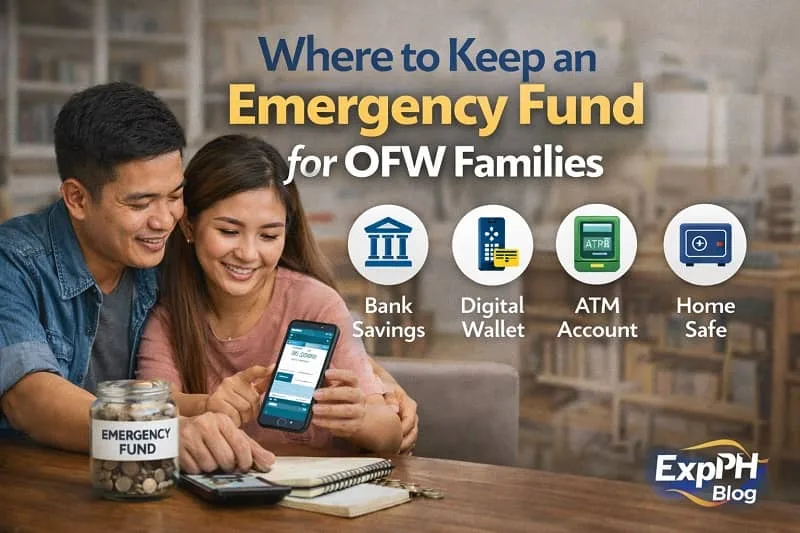

Where to Keep an Emergency Fund for OFW Families

When choosing where to store an emergency fund, accessibility and safety are more important than high returns. OFW families should prioritize accounts that allow quick withdrawals during urgent situations, ensuring funds are available when emergencies happen without delays.

Best Places to Store an Emergency Fund

Emergency funds should be placed in secure and easily accessible accounts:

- Digital banks with high liquidity

- Philippine savings accounts with ATM access

- Joint accounts trusted by both the OFW and family

- Separate accounts used only for emergencies

Avoid Placing Emergency Funds In

Some options are risky or difficult to access during emergencies and should be avoided:

- Cryptocurrency

- Stocks or mutual funds

- Long-term time deposits with penalties

- Business capital

An emergency fund must remain liquid and accessible so families can respond quickly when unexpected situations arise.

Step-by-Step Emergency Fund Planning for OFW Families

Building an emergency fund takes time and consistency. It is not a one-time task but a gradual process that requires discipline. OFW families benefit most when savings are planned, monitored, and adjusted as income and responsibilities change.

Step 1: Separate Emergency Fund From Regular Savings

Emergency savings should be kept separate from daily or long-term savings. Mixing funds increases temptation and leads to misuse. A clearly labeled emergency account helps protect the fund and reinforces its purpose during urgent situations.

Step 2: Start With a Starter Fund

Begin with a small but realistic goal before aiming for full coverage. Saving an initial amount such as PHP 20,000 to PHP 50,000 provides immediate protection and reduces stress while building confidence to continue saving regularly.

Step 3: Automate Savings From Remittances

Set aside a fixed amount from every remittance and treat it like a required expense. Automation helps maintain consistency and removes the temptation to skip savings, even during months with higher household spending.

Step 4: Increase Contributions When Income Rises

When income improves through bonuses, overtime, or favorable exchange rates, increase emergency fund contributions. Allocating part of these extra earnings strengthens the fund faster without affecting regular household expenses.

Step 5: Review and Adjust Annually

Review the emergency fund at least once a year. Changes in family size, expenses, or income levels may require higher savings. Regular adjustments ensure the fund continues to meet the family’s real financial needs.

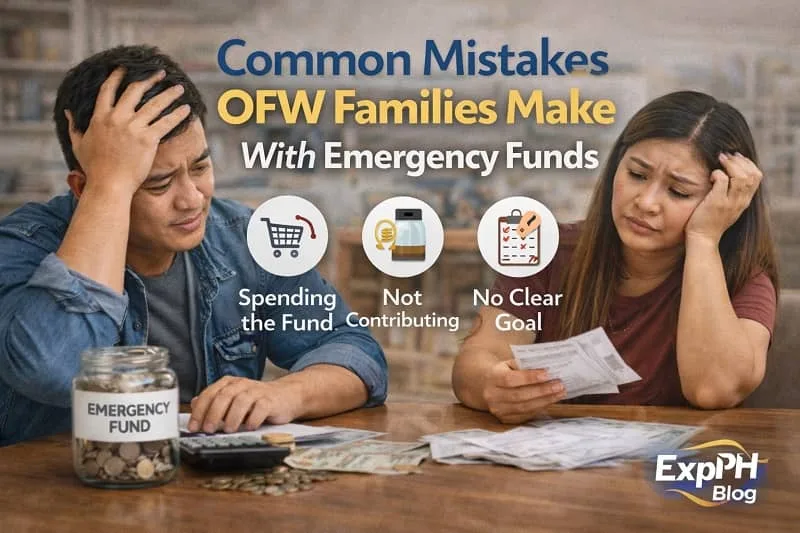

Common Mistakes OFW Families Make With Emergency Funds

Knowing the common mistakes OFW families make with emergency funds helps prevent setbacks. Many problems come from poor planning, unclear rules, or overconfidence. Avoiding these errors keeps the emergency fund effective and ready when real financial emergencies occur.

Using the Emergency Fund for Non Emergencies

Using emergency funds for non urgent expenses is the most common mistake. Once the rules are ignored, the fund loses its purpose. This habit weakens financial protection and leaves families unprepared when true emergencies arise.

Keeping the Fund Inaccessible

Placing emergency funds in investments or overseas accounts can cause delays during local emergencies. When money cannot be accessed quickly, families may still need loans even though they technically have savings.

Relying on Credit Instead of Savings

Relying on loans instead of emergency savings creates long-term financial pressure. Interest payments increase costs and reduce future income. A well maintained emergency fund helps families avoid debt cycles during difficult periods.

Assuming Remittances Are Guaranteed

Overseas income is never guaranteed. Job loss, contract issues, or global events can interrupt remittances. Emergency fund planning must assume income disruptions and prepare families to manage expenses without immediate overseas support.

How Emergency Fund Planning Protects OFWs Abroad

Emergency fund planning supports not only families in the Philippines but also OFWs working overseas. Knowing that savings are available during emergencies provides security and stability. This protection allows OFWs to manage challenges abroad without constant worry about sudden financial demands.

Reduced Stress and Mental Burden

When OFWs know their families can handle emergencies financially, stress is reduced. This peace of mind helps them stay focused on work, maintain emotional balance, and avoid constant anxiety caused by unexpected financial problems at home.

Avoiding Emergency Loans Overseas

Without emergency savings, some OFWs turn to high interest loans abroad. These loans increase financial pressure and reduce take home pay. Emergency funds help OFWs avoid debt and manage urgent expenses without borrowing.

Protection During Job Loss or Contract Issues

Emergency funds provide a safety buffer when job loss or contract problems occur. They allow OFWs time to search for new work or return home calmly without making rushed or costly financial decisions.

Teaching Financial Discipline to OFW Families

Emergency fund planning helps OFW families develop long-term financial discipline. Saving regularly encourages responsible spending and better decision making. Over time, families learn to prioritize needs, manage money wisely, and work together toward shared financial goals.

Creating a Family Agreement

A clear family agreement sets rules for how the emergency fund should be used. Discuss these rules openly with all members. When everyone understands the purpose of the fund, misuse is reduced and commitment becomes stronger.

Transparency Builds Trust

Sharing the emergency fund balance from time to time builds trust within the family. Transparency encourages accountability and cooperation, helping family members respect savings goals and support each other during both normal periods and emergencies.

Financial Education for Spouses and Dependents

Teaching spouses and dependents basic budgeting and saving skills helps protect the emergency fund. Financial education ensures everyone understands why the fund matters and how responsible money habits support long-term family stability.

Building Skills to Strengthen Emergency Fund Stability

Saving money alone is sometimes not enough to protect OFW families during emergencies. Income stability plays a major role in financial security. Developing practical skills helps families maintain savings, manage expenses, and respond to financial challenges without quickly draining their emergency fund.

Why Skills Matter for Emergency Preparedness

When OFW families have more than one income option, emergencies become easier to manage. Skills provide flexibility and reduce dependence on a single income source. This makes it less likely that emergency savings will be exhausted during extended financial disruptions.

Practical Skills That Help OFW Families

Developing the right skills supports income stability and better money management:

- Budgeting and personal finance management

- Freelancing and online work

- Side hustle planning

- Financial literacy for spouses

Learning Budgeting and Income Skills Online

Many OFW families strengthen their emergency fund by improving financial knowledge and income skills. Online learning platforms offer practical courses on budgeting, freelancing, and money management that can be applied immediately and adjusted to busy OFW schedules.

One helpful resource is Udemy, which provides flexible online courses on personal finance, budgeting, freelancing skills, and income planning. These courses allow OFWs and their families to learn at their own pace while supporting long-term financial security.

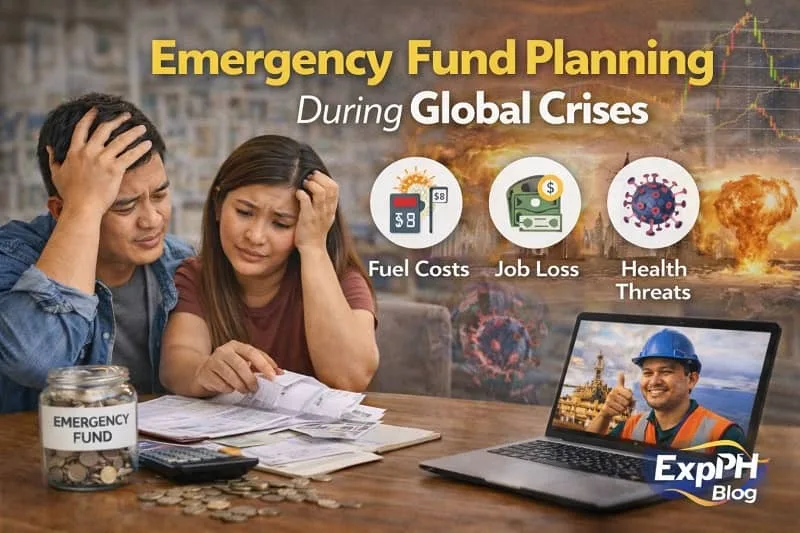

Emergency Fund Planning During Global Crises

Recent global events have shown how vulnerable overseas employment can be. Sudden economic changes can affect jobs, income, and mobility. Emergency fund planning helps OFW families stay financially stable and prepared when global crises disrupt work, travel, or remittance flow.

Lessons From Past Global Disruptions

Past global disruptions highlight the importance of financial preparedness for OFW families:

- Sudden layoffs without warning

- Travel restrictions affecting contract renewals

- Medical emergencies without immediate support

- Delayed remittances

Emergency fund planning gives families financial breathing room during unpredictable and stressful situations.

Government Safety Nets Are Limited

Government assistance can help during crises, but support is often delayed or insufficient. The Bangko Sentral ng Pilipinas emphasizes financial preparedness and household savings as key factors in economic resilience, showing why personal emergency funds remain essential for OFW families during crises. This reinforces the importance of maintaining personal emergency funds.

How Emergency Funds Prevent Long-Term Financial Damage

Emergency funds help OFW families avoid deeper financial problems during difficult times. Having savings available allows families to handle urgent expenses calmly. This protection reduces panic decisions and prevents financial issues from turning into long-term burdens.

Avoiding High-Interest Debt

Without emergency savings, families often rely on loans to cover urgent needs. These loans may solve short-term problems but lead to long-term stress through interest payments. Emergency funds help families manage crises without borrowing.

Protecting Assets

Families without emergency funds may be forced to sell land, appliances, or vehicles quickly. These assets are often sold below value. Emergency savings protect family property and prevent losses caused by rushed financial decisions.

Maintaining Credit Reputation

Emergency savings help families pay bills on time during difficult periods. This prevents missed payments, protects credit standing, and reduces future borrowing problems that can limit financial options.

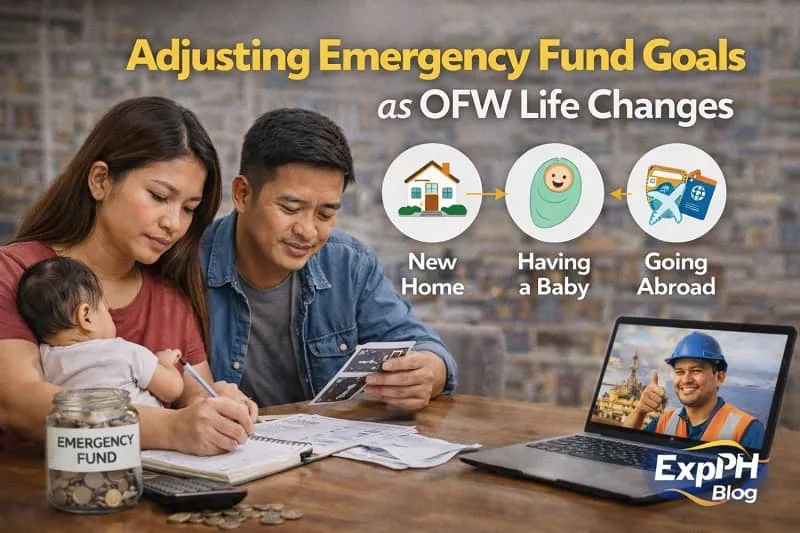

Adjusting Emergency Fund Goals as OFW Life Changes

Emergency fund planning is not static and should change as an OFW’s life situation evolves. Income, responsibilities, and living arrangements affect financial needs. Regular adjustments ensure the emergency fund remains enough to support the family during new challenges.

When Family Size Changes

Marriage, having children, or supporting elderly dependents increases household expenses. As family size grows, emergency fund targets should also increase. More dependents mean higher financial responsibility and a greater need for protection during unexpected situations.

When Income Becomes Unstable

Short-term contracts and irregular income create higher financial risk. OFW families in this situation should build larger emergency buffers. A stronger fund helps manage income gaps and reduces stress when employment conditions change unexpectedly.

When Returning to the Philippines

Returning home often involves income uncertainty and adjustment costs. Higher emergency savings help cover job searches, temporary income loss, or business setup expenses. This preparation allows a smoother transition without financial pressure.

Emergency Fund vs Insurance for OFW Families

Emergency funds and insurance are both important for financial protection, but they serve different purposes. OFW families need both to stay prepared. Understanding how each works helps families respond properly to emergencies without confusion or delays.

Emergency Fund

An emergency fund provides quick access to cash for urgent needs. It is flexible and easy to use during different situations. Emergency funds can cover medical costs, job loss, or travel expenses without waiting for approval.

- Covers immediate cash needs

- Flexible and accessible

- Used for various emergencies

Insurance

Insurance protects against specific risks such as health issues or loss of life. Claims often require documents and approval. Because payouts take time, insurance does not always provide immediate cash during emergencies.

Making Emergency Fund Planning a Family Habit

Emergency fund planning works best when it becomes a family habit. Consistency matters more than speed. Regular saving builds discipline and confidence over time. When the whole family supports the goal, maintaining and growing the emergency fund becomes easier and more sustainable.

Monthly Check Ins

Monthly check ins help families stay aware of their savings progress. Reviewing contributions and balances allows timely adjustments. These regular discussions keep everyone aligned and prevent small issues from becoming larger financial problems later.

Celebrate Milestones

Recognizing milestones keeps motivation high. Reaching the first 50,000 or 100,000 pesos shows progress and commitment. Simple celebrations encourage families to continue saving and reinforce the value of long-term financial preparation.

Keep Goals Visible

Keeping savings goals visible helps families stay focused. Visual trackers such as charts or notes serve as reminders. Seeing progress regularly encourages consistency and strengthens commitment to emergency fund planning.

Final Thoughts: Building Security Through an Emergency Fund for OFW Families

Emergency fund planning is one of the most important financial actions OFW families can take. It protects household income during uncertainty, reduces stress during emergencies, and helps prevent reliance on debt. An emergency fund for OFW families is not based on fear but on preparation, responsibility, and long-term stability. With savings in place, families can face unexpected events with confidence and make better financial decisions without pressure.

By starting with small and realistic savings goals, staying disciplined, and involving the entire family, OFWs can build a strong financial foundation. Emergency fund planning becomes more effective when everyone understands its purpose. No matter where the OFW works, knowing the family is financially protected brings peace of mind that supports both work performance and family well-being.

Discover new insights in the list below.

- How OFWs Can Avoid Debt Traps Abroad

- Common Money Mistakes New Business Owners Must Avoid

- Simple Financial Systems Small Businesses Should Set Up Early

- How OFWs Can Handle Financial Emergencies From Abroad

- Productivity Habits for Filipinos Working Overseas

FAQs About Emergency Fund for OFW Families

What is emergency fund planning for families with OFWs?

Emergency fund planning for families with OFWs means setting aside money specifically for unexpected expenses, income disruptions, or emergencies affecting both the OFW and family members.

Why is an emergency fund important for OFW families?

An emergency fund helps OFW families handle medical emergencies, job loss, delayed remittances, or disasters without relying on loans or creating long-term financial stress.

How much should an emergency fund for OFW families be?

An emergency fund for OFW families should ideally cover six to nine months of essential household expenses to manage income gaps and overseas employment uncertainties.

Where should OFW families keep their emergency fund?

OFW families should keep emergency funds in accessible savings accounts, digital banks, or joint accounts that allow quick withdrawals during urgent situations.

Can OFW families use emergency funds for non urgent expenses?

Emergency funds should only be used for urgent and unexpected situations, not for planned purchases, lifestyle upgrades, or regular household spending.

How can OFW families start building an emergency fund?

OFW families can start by saving small amounts from each remittance, separating emergency savings, and gradually increasing contributions as income becomes stable.

What happens if an OFW loses their job suddenly?

An emergency fund provides temporary financial support for household needs while the OFW looks for new employment or prepares for a safe return home.

Is insurance enough without an emergency fund?

Insurance helps cover specific risks, but emergency funds provide immediate cash, making both essential for complete financial protection for OFW families.

How often should OFW families review their emergency fund?

OFW families should review their emergency fund at least once a year or whenever household expenses, income, or family responsibilities change.

Can emergency fund planning reduce financial stress for OFWs?

Yes, emergency fund planning reduces stress by ensuring families can manage crises independently, allowing OFWs to focus on work and personal well-being.

Test your knowledge of emergency fund planning and see how ready your family is for unexpected expenses.

Results

#1. What is the main purpose of an emergency fund?

#2. Who benefits most from an emergency fund?

#3. How many months should an emergency fund cover?

#4. Which expense qualifies as an emergency?

#5. Where should emergency funds be stored?

#6. When should emergency funds be used?

#7. Why are emergency funds vital for OFWs?

#8. What happens without an emergency fund?

#9. How should OFW families start saving?

#10. How often should funds be reviewed?

We’d Love to Hear From You. Comment below and share your thoughts with us.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.