How OFWs Can Build Savings Even With Family Obligations

For many Overseas Filipino Workers, saving money can feel nearly impossible. Each payday is often planned before the salary even arrives. Tuition fees, medical bills, rent, food, utilities, and urgent family requests usually take priority. After meeting these obligations, little remains for savings. This situation creates frustration and makes long-term financial planning feel out of reach for many OFWs.

Still, OFW savings is not a lost cause, even when family responsibilities are heavy. Many OFWs succeed by building savings gradually rather than all at once. They do this by improving how financial decisions are planned, communicated, and prioritized. Clear goals, better structure, and realistic expectations allow savings to grow steadily over time.

Many OFWs discover that saving becomes easier when it is treated as a shared responsibility rather than a personal struggle. When families understand financial limits and long-term goals, pressure decreases and cooperation improves. This shared awareness helps reduce guilt, prevents misunderstandings, and allows savings habits to remain consistent during challenging periods.

This guide is written for real OFWs facing real situations. It is not about cutting off family support or living an unrealistic lifestyle abroad. Instead, it focuses on practical strategies that allow OFWs to support loved ones while still protecting their own financial future.

Understanding the Reality of OFW Savings With Family Obligations

Before discussing strategies, it is important to recognize the emotional and cultural realities OFWs face. Savings challenges are rarely only about numbers. They are deeply connected to responsibility, guilt, and expectations placed on overseas workers to provide steady support for their families.

Why Family Obligations Are Heavier for OFWs

Many OFWs become the primary or sole breadwinner of the family. This situation develops due to several common factors that increase financial pressure and limit saving capacity over time.

Key reasons include:

- Higher income compared to local wages in the Philippines

- Relatives assuming overseas work means financial comfort

- Strong Filipino values focused on family support

- Limited alternative income sources at home

These pressures often result in fixed monthly remittances, plus additional requests for emergencies, celebrations, or unplanned expenses that reduce opportunities to build consistent savings.

The Cost of Ignoring OFW Savings

Without savings, OFWs face serious risks such as job loss, illness, contract termination, or sudden repatriation. According to the Bangko Sentral ng Pilipinas, building regular savings helps households manage emergencies and income disruptions, especially for overseas workers who face job and contract uncertainties.

Ignoring savings may feel like a short-term sacrifice for family, but over time it often creates bigger financial problems for everyone involved.

Reframing OFW Savings as Family Protection

One of the most important mindset shifts for OFWs is realizing that saving money is not selfish. Savings is a form of family protection. It prepares the OFW for unexpected events and reduces future financial stress that could affect loved ones at home.

Savings Is Not the Opposite of Support

Many OFWs believe that every peso saved is money taken away from their family. This belief creates guilt and blocks consistent saving habits. In reality, OFW savings protects the entire household by preparing for situations where regular income may suddenly stop.

Savings can help cover the following needs:

- Medical emergencies abroad

- Sudden job loss or contract problems

- Return migration and relocation costs

- Capital for small family businesses

- Retirement support later in life

When OFWs have savings, families are less exposed to financial shocks and urgent borrowing.

Creating a Shared Understanding With Family

Open communication plays a major role in protecting OFW savings. Families need to understand that saving is not about refusing help. It is about ensuring long-term stability and avoiding crisis situations that harm everyone involved, including dependents and future plans.

Helpful conversation starters include the following points:

- Explaining fixed limits on remittances

- Sharing long-term goals like home ownership or retirement

- Agreeing that only real emergencies fall outside the budget

Clear expectations reduce emotional pressure and help maintain financial balance for both OFWs and their families.

Building OFW Savings Without Reducing Family Support

Building OFW savings does not always mean sending less money home. In many cases, it simply requires better structure and planning. With clear systems in place, OFWs can support their families consistently while still setting aside money for future needs.

Start With a Fixed Savings Rule

Instead of saving what remains after expenses, OFWs should save first. Even a small amount builds discipline and momentum. The key is consistency, not size, because regular saving creates a strong habit over time.

Examples of simple saving rules include:

- Five percent of salary saved automatically

- One week of pay saved each month

- Fixed peso amount saved every payday

Separate Savings From Remittance Accounts

Many OFWs mix savings with remittance money, which makes it easier to spend savings without noticing. Keeping savings in a separate account creates clear boundaries and strengthens discipline by reducing temptation during emergencies or family requests.

Practical options for separate savings include:

- Offshore savings accounts

- Philippine digital banks

- Time deposit accounts

The goal is to make savings less accessible and easier to protect.

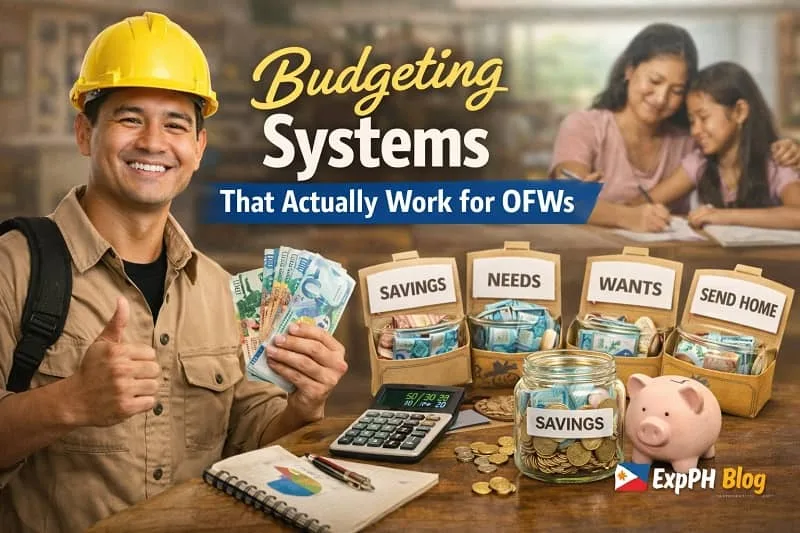

Budgeting Systems That Actually Work for OFWs

Not all budgeting methods fit the reality of OFW life. The most effective systems are simple, flexible, and easy to maintain. A practical budget helps OFWs manage family responsibilities while protecting savings without requiring daily tracking or complicated calculations.

Use a Remittance-Based Budget

Instead of budgeting every expense, OFWs can organize money around remittance categories. This approach keeps family support consistent while ensuring savings are protected and planned in advance, even when income or expenses change.

A simple remittance-based structure includes:

- Fixed family support

- Emergency fund contribution

- Personal savings

- Personal expenses abroad

Plan for Irregular Expenses

Many OFW savings plans fail because irregular expenses are ignored. Birthdays, school enrollment, and medical needs are predictable even if dates change. Planning ahead prevents sudden withdrawals from savings during urgent situations.

Create sinking funds for the following needs:

- Tuition and school supplies

- Annual family events

- Health-related expenses

Planning ahead reduces financial stress and protects long-term savings.

Managing Emergency Requests Without Destroying OFW Savings

Emergency requests are one of the biggest threats to OFW savings. Handling them well requires clear financial limits and emotional boundaries. Without clear rules, urgent requests can quickly drain savings and create stress for both the OFW and family members.

Define What Counts as an Emergency

Not all urgent requests are true emergencies. OFWs should work with their families to clearly define situations that require immediate financial help. This shared understanding prevents savings from being used for non-essential needs.

Examples of real emergencies include:

- Hospitalization

- Accidents

- Natural disasters

- Immediate health risks

Clear definitions help protect long-term savings.

Create a Family Emergency Fund

Instead of relying on personal savings, OFWs can set up a small family emergency fund in the Philippines. This fund should be used only for true emergencies and replenished gradually when income allows.

This approach supports family needs while protecting long-term OFW savings.

Increasing Income to Strengthen OFW Savings

Sometimes improving OFW savings is not about cutting expenses but about earning better. Increasing income gives OFWs more room to save while continuing family support. Even small income improvements can make savings more consistent and reduce financial pressure over time.

Why Skills Matter for OFWs

Higher-paying roles, promotions, and flexible side work often depend on skills. Many OFWs stay in the same pay level for years because learning opportunities are limited. Skill development creates more options and improves long-term earning potential.

Learning new skills can lead to:

- Salary increases

- Better job contracts

- Remote or freelance opportunities

- Transition to less physically demanding work

Skills provide stability and support stronger OFW savings growth.

Investing in Skills That Improve OFW Savings

Using Online Learning to Increase Earning Potential

One practical way to improve OFW savings without adding financial pressure on family is through skill development. Online courses allow OFWs to learn at their own pace, even with shifting schedules.

Platforms like Udemy offer affordable courses in areas such as freelancing, digital skills, finance basics, and career development. These skills can open doors to higher income, side projects, or long-term career growth.

When learning is aligned with real income opportunities, it becomes a strategic investment rather than an expense. This approach strengthens savings over time without sacrificing family support.

Avoiding Common Mistakes That Kill OFW Savings

Even disciplined OFWs make small mistakes that slowly drain savings. These errors often feel harmless at first but create long-term damage when repeated. Recognizing common pitfalls helps OFWs protect their money while still meeting family responsibilities and personal needs.

Lifestyle Inflation Abroad

As income increases, expenses often rise as well. Eating out more often, upgrading gadgets, or paying for unused subscriptions can quietly reduce savings. OFWs should review lifestyle upgrades and check if these expenses support long-term goals.

Lending Money Without Clear Terms

Many OFWs lose savings by lending money to relatives without clear agreements. While helping family feels natural, unclear terms often lead to stress, conflict, and financial loss that affects savings goals.

If lending is unavoidable, follow these rules:

- Set clear repayment terms

- Only lend affordable amounts

- Do not use savings or emergency funds

Long-Term Planning That Protects OFW Savings

OFW savings is not only about today’s needs. It is about preparing for the time when overseas work ends. Long-term planning gives direction to savings and helps OFWs avoid rushed decisions that can harm financial security later.

Planning for Return to the Philippines

OFWs should begin planning early for their return to the Philippines. Clear goals help savings serve a purpose and support smoother reintegration after overseas work ends.

Savings can be used for:

- Small business capital

- Housing or land purchase

- Skills transition

- Family income diversification

Early planning reduces stress and costly mistakes.

Retirement Planning for OFWs

Many OFWs delay retirement planning because it feels distant. In reality, time moves quickly. Starting early makes retirement more manageable and reduces pressure later in life.

Retirement savings options may include:

- Long-term savings accounts

- Investment-linked insurance products

- Passive income projects

Early action makes future responsibilities lighter.

Teaching Financial Responsibility to Family Members

OFW savings improves when family members manage money wisely at home. Financial responsibility should not rest on the OFW alone. When families understand spending limits and priorities, savings last longer and financial stress is reduced for everyone involved.

Teaching financial responsibility helps families become active partners in achieving OFW savings goals. When family members understand how money is earned and managed, they make more thoughtful decisions. This awareness reduces impulsive spending and builds respect for the sacrifices made abroad. Over time, shared responsibility creates trust, stability, and healthier financial habits at home.

Encouraging Budget Discipline at Home

Families should understand the importance of budgeting even when income comes from abroad. Simple habits help control spending and reduce unnecessary requests that affect savings.

Encourage habits such as:

- Tracking daily expenses

- Avoiding unnecessary loans

- Planning purchases in advance

Shared discipline supports stronger OFW savings.

Supporting Income Generation at Home

When families earn income locally, financial pressure on OFWs decreases. Supporting local income sources builds independence and long-term stability for the household.

Effective options include:

- Small home businesses

- Freelancing or online work

- Skills training for dependents

Shared income leads to shared financial security.

Building OFW Savings Is a Long Game, Not a One-Time Decision

Saving money while supporting family is challenging, but it is achievable with the right mindset, clear structure, and patience. OFW savings does not happen overnight. It grows gradually through consistent actions and realistic expectations built over time. Small, repeatable decisions often matter more than large one-time efforts.

Many OFWs struggle because they expect immediate results. When savings grow slowly, discouragement sets in and habits are abandoned. Understanding that progress takes time helps OFWs stay disciplined, even during months when expenses are high or income feels stretched.

OFW savings grows through the following practices:

- Consistent habits

- Honest communication

- Smart income strategies

- Clear boundaries

- Long-term thinking

Consistency turns saving into a routine rather than a struggle. Open communication reduces guilt and misunderstanding with family. Income strategies provide flexibility, while boundaries protect savings from emotional decisions.

No OFW needs to choose between family support and financial security. With the right approach, both can exist together and strengthen future stability. When savings are part of the plan, family support becomes more sustainable and less stressful.

The journey may feel slow, but every peso saved builds freedom, security, and peace of mind. Over time, OFW savings becomes a foundation that protects not only the worker abroad but the entire family at home.

Explore similar OFW topics below.

- How OFWs Can Protect Their Income From Poor Decisions

- How OFWs Can Prepare Financially Before Returning Home

- Financial Checklists Filipinos Should Complete Before Returning Home

- Top 10 Small Business Ideas in the Philippines for 2026

- Digital Tools OFWs Can Use to Track Career Progress

FAQs About OFW Savings

What is the first step OFWs should take to start saving?

OFWs can start small by saving a fixed amount every payday, separating savings accounts, setting clear family budgets, and treating savings as protection goal together.

Does building OFW savings mean sending less money to family?

Building OFW savings does not mean reducing support, it means planning limits, budgeting emergencies, communicating expectations, and ensuring long term stability for worker and family.

How can OFWs handle emergency requests without losing savings?

OFWs should define real emergencies with family, create a separate emergency fund, avoid touching personal savings, and review requests calmly before sending additional money home.

What budgeting method works best for OFWs?

A remittance based budget works best for OFW savings because it prioritizes fixed family support, savings first, and flexible personal expenses without complicated tracking systems.

Why should OFWs use separate accounts for savings?

Separate accounts protect OFW savings by reducing temptation, preventing accidental spending, and creating mental boundaries that help OFWs stay disciplined during emergencies or family pressure.

How does skill improvement help OFW savings?

Improving skills increases income potential, promotions, and side opportunities, allowing OFWs to grow savings faster without cutting family support or increasing financial stress long term.

Can lending money to relatives affect OFW savings?

Lending money can hurt OFW savings when expectations are unclear, repayments fail, or emotional pressure replaces financial judgment and disciplined decision making within family relationships.

Why is early planning important for returning OFWs?

Planning early helps OFWs use savings for reintegration, business capital, housing, or career transition, reducing stress when overseas work eventually ends for families back home.

How can families support OFW savings goals?

Teaching family budgeting and responsibility reduces dependency, controls spending, and supports OFW savings by aligning household habits with long term financial goals and shared priorities.

How long does it usually take to build strong OFW savings?

OFW savings grows gradually through consistency, patience, clear communication, income improvement, and realistic expectations rather than quick fixes or extreme sacrifices for working families everywhere.

Test your understanding of how OFWs can build savings even with family obligations.

Results

#1. What is the best way to start OFW savings?

#2. Why is saving important for OFWs?

#3. What should OFWs do before sending extra money?

#4. Which account helps protect savings?

#5. What budgeting style suits OFWs best?

#6. How can OFWs increase savings faster?

#7. What harms OFW savings most?

#8. Why should families learn budgeting?

#9. What fund protects savings during crises?

#10. What mindset supports long-term OFW savings?

Thank you for taking the time to improve your financial knowledge.

Share your experience. Comment below and tell us how this quiz helped you or what savings challenge you face as an OFW. Your story can help others.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Smart Ways to Balance Family Support and Personal Savings.