How OFWs Can Protect Their Income From Poor Decisions

For many Overseas Filipino Workers, earning abroad represents sacrifice, resilience, and hope for a better future. Every paycheck often carries the weight of family expectations, long-term dreams, and financial responsibilities back home. Because of this, protecting income is just as important as earning it.

OFW income protection is not only about saving money. It is about avoiding decisions that slowly drain hard-earned income, whether through impulsive spending, risky investments, scams, or lack of financial planning. Many OFWs earn well but still struggle financially due to poor decisions made without enough information or guidance.

This guide is written to help OFWs understand the most common threats to their income and how to protect it through practical, realistic, and sustainable actions. The goal is not perfection, but progress and awareness that lead to smarter financial choices.

Understanding Why OFW Income Is Vulnerable

OFW income faces higher risk because of distance from family, contract-based employment, and strong financial expectations at home. These factors often influence decisions and create pressure to act quickly. Understanding these vulnerabilities helps OFWs build stronger income protection strategies and maintain long-term financial stability.

Income Abroad Comes With Unique Pressures

OFWs face financial pressures that many local workers do not experience. Being far from family, combined with cultural expectations and emotional guilt, often affects money choices. Many OFWs feel responsible for supporting extended family, even when this support slowly weakens their own financial stability.

These pressures can lead to rushed decisions like lending money without agreements, investing in businesses without preparation, or sending more money than is safe. OFW income protection begins by recognizing that emotional choices can be just as damaging as clearly poor financial decisions.

Irregular Work and Contract-Based Employment

Many OFWs work under fixed-term contracts where income can be high but stability is uncertain. Contract renewals are not guaranteed, and job loss may happen due to company changes, economic downturns, or shifting labor demands in host countries.

Without proper planning, one poor decision during high-income periods can cause lasting damage. When income suddenly stops, lack of savings and preparation can quickly turn temporary job loss into a serious long-term financial problem.

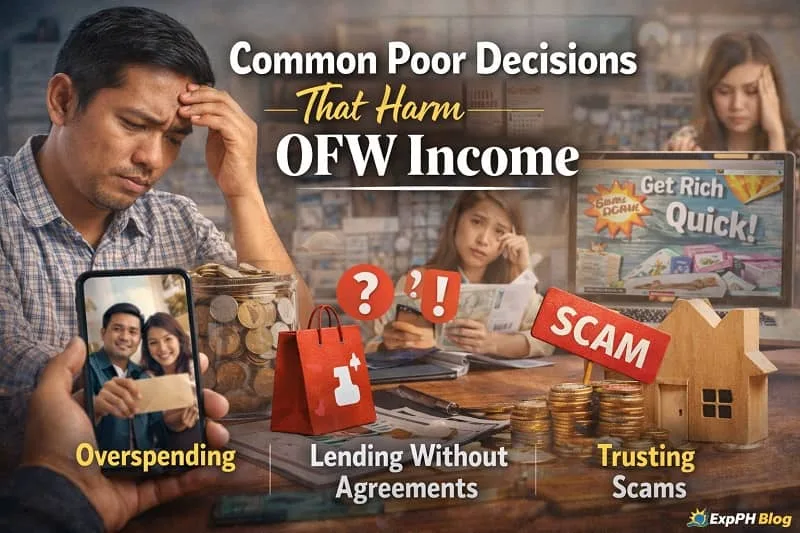

Common Poor Decisions That Harm OFW Income

Many OFWs lose income not because they earn less, but because of repeated poor decisions. These include overspending, trusting unverified investments, lending without agreements, and acting emotionally under pressure. Recognizing these common mistakes helps OFWs avoid financial losses and protect long-term income stability.

Living Beyond Sustainable Means

A higher salary abroad often leads to lifestyle inflation. New gadgets, branded items, frequent travel, and expensive dining can slowly eat away income. While enjoying rewards is normal, unchecked spending reduces the ability to save and invest wisely. Many OFWs only realize the impact years later when they return home without enough savings.

Trusting the Wrong People With Money

One of the biggest threats to OFW income protection is misplaced trust. This includes:

- Lending large amounts without written agreements

- Allowing relatives to manage businesses without accountability

- Giving full control of finances to others without transparency

While helping family is part of Filipino culture, financial protection requires boundaries.

Falling for Get-Rich-Quick Schemes

Scams targeting OFWs often promise fast returns, low risk, and guaranteed income. These schemes usually spread through social media, group chats, or referrals from acquaintances.

According to the Philippine government’s migrant protection advisories, OFWs are frequently targeted due to their perceived earning capacity and distance from home. The Department of Migrant Workers regularly warns OFWs to verify investment opportunities and avoid unregistered financial schemes through official channels such as https://dmw.gov.ph.

Building a Strong Foundation for OFW Income Protection

A strong financial foundation helps OFWs protect income and avoid costly mistakes. This starts with clear priorities, realistic budgeting, and disciplined saving habits. When income is managed with purpose and structure, OFWs gain better control, reduce stress, and build long-term financial stability.

Setting Clear Financial Priorities

Protecting income starts with clear direction. OFWs should identify what truly matters financially, including the following priorities:

- Monthly essential expenses

- Fixed family support amount

- Personal savings goal

- Emergency fund target

Without clear priorities, money is easily spent without purpose. Writing financial goals helps reduce impulse decisions and supports stronger OFW income protection over time.

Creating a Realistic Budget That Works Abroad

A budget helps protect income rather than limit freedom. OFWs should consider these key factors when planning their budget:

- Cost of living in the host country

- Exchange rate changes

- Mandatory remittances

- Personal needs and rest days

Budgets should be reviewed regularly. Changes in income or expenses require adjustments to keep spending balanced and income protected.

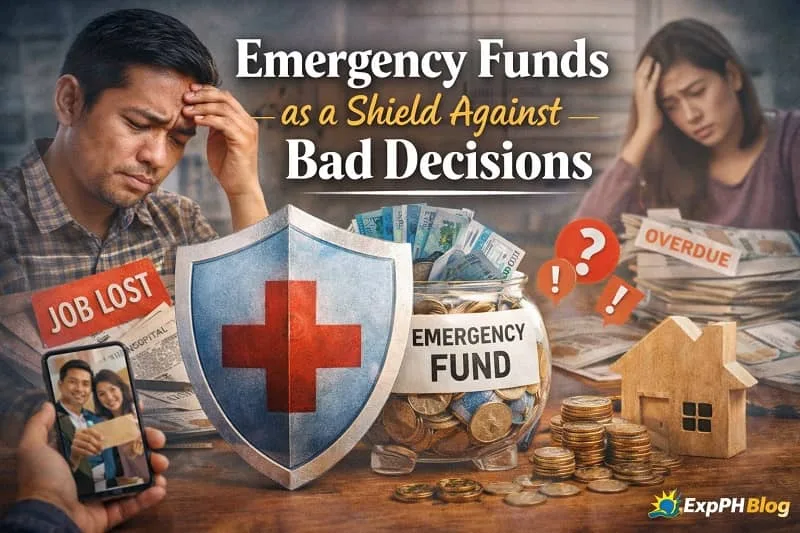

Emergency Funds as a Shield Against Bad Decisions

Emergency funds act as a financial safety net for OFWs, helping protect income during unexpected events such as job loss, medical needs, or family emergencies. Having ready savings reduces panic, prevents rushed decisions, and strengthens OFW income protection during uncertain periods.

Why Emergency Funds Prevent Desperation Choices

Many poor financial decisions happen during emergencies. Medical issues, sudden job loss, or family crises can push OFWs to borrow money, sell assets, or accept unfair deals. An emergency fund covering three to six months of expenses provides stability and helps prevent panic-driven choices that cause lasting financial damage.

Where to Keep Emergency Funds Safely

Emergency funds should be stored in places that protect both access and security. Ideal emergency fund storage includes:

- Easily accessible accounts

- Separate from daily spending funds

- Secure and regulated financial institutions

Avoid placing emergency funds in high-risk investments or locking them into long-term accounts that restrict access during emergencies.

Smart Remittance Practices for OFW Income Protection

Smart remittance practices help OFWs support their families without harming financial stability. Sending money with clear limits, planned amounts, and open communication reduces pressure and overspending. When remittances are managed with purpose, OFWs can protect income while still meeting family responsibilities.

Sending Money With Purpose, Not Pressure

Sending money home should always be intentional and planned. OFWs can protect their income by following these practices:

- Agreeing on fixed remittance amounts

- Avoiding emotional increases during family conflicts

- Communicating financial limits clearly

Supporting family is important, but it should never come at the cost of long-term financial stability.

Encouraging Financial Responsibility at Home

OFW income protection improves when family members understand basic budgeting and financial discipline. Encouraging loved ones to track expenses, save consistently, and avoid unnecessary debt helps ensure remittances are used wisely and support long-term goals instead of short-term spending.

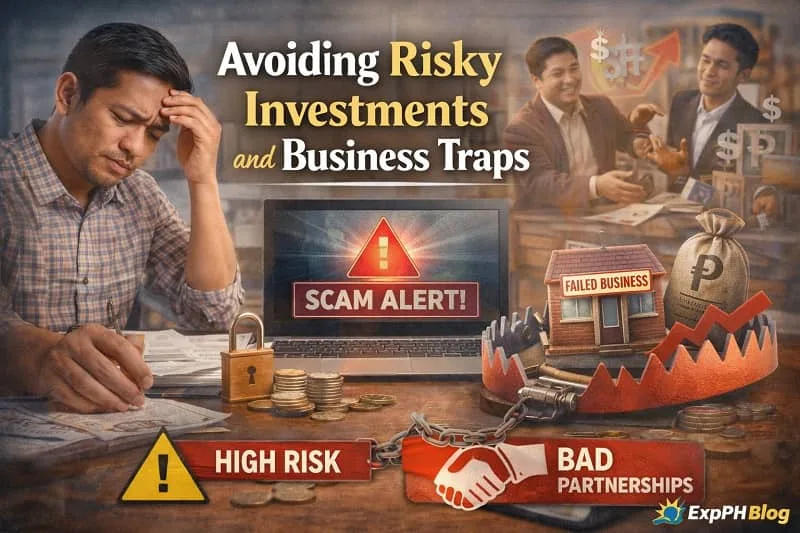

Avoiding Risky Investments and Business Traps

Risky investments and poorly planned businesses can quickly drain OFW income. Many losses happen due to lack of research, pressure-based offers, or unrealistic promises. Learning to evaluate opportunities carefully helps OFWs avoid scams, reduce financial risk, and protect hard-earned income over time.

Understanding Before Investing

Investing without proper understanding is risky and often leads to losses. OFWs should avoid the following warning signs:

- Investments they cannot explain clearly

- Opportunities that promise guaranteed returns

- Pressure-based offers with limited time claims

If an opportunity does not allow time for research, it is usually not worth pursuing.

Separating Business Dreams From Financial Reality

Many OFWs hope to start a business back home, but poor planning often causes failure. Before investing, OFWs should follow these steps:

- Study the business model

- Start small when possible

- Assign clear accountability

- Monitor performance regularly

Business investments should strengthen OFW income protection rather than weaken long-term financial stability.

Strengthening Decision-Making Through Skills and Knowledge

Strong decision-making depends on knowledge and skills. When OFWs continue learning, they gain confidence, flexibility, and better judgment in financial and career choices. Skills development helps reduce reliance on risky options and supports stable income, making long-term OFW income protection more achievable.

Why Knowledge Is a Form of Income Protection

Poor financial decisions often result from limited information. Learning new skills improves career flexibility, income stability, and confidence when making choices. Upskilling supports OFW income protection by helping workers:

- Qualify for higher-paying roles

- Transition to safer industries

- Build backup income sources

Knowledge reduces guesswork and leads to smarter long-term decisions.

Learning Skills That Support Long-Term Stability

Skills related to digital work, freelancing, management, and financial literacy offer lasting value. These skills help OFWs reduce dependence on physical labor and contract-based jobs. Over time, stronger skills improve income stability and open opportunities beyond traditional overseas employment.

Recommended Learning Resource for OFWs

Structured learning is a practical way to strengthen decision-making and career security. Online platforms such as Udemy provide courses in financial literacy, freelancing, career development, and digital skills that OFWs can study at their own pace.

Choosing education over impulsive investments is one of the most effective OFW income protection strategies for long-term stability.

Protecting Income Through Legal and Contract Awareness

Understanding employment contracts and legal rights helps OFWs avoid income loss and workplace abuse. Being aware of contract terms, deductions, and support channels allows OFWs to respond wisely to problems. Legal awareness strengthens income protection and prevents decisions based on fear or misinformation.

Understanding Employment Contracts Fully

Many OFWs sign employment contracts without fully understanding the terms, which can lead to unpaid overtime, unexpected deductions, or unfair termination. Before signing any contract, OFWs should take these important steps:

- Read all clauses carefully

- Ask questions when unclear

- Keep copies of contracts and payslips

Understanding employment rights helps protect income from abuse and workplace exploitation.

Knowing Where to Seek Help

OFWs should know where to seek help when facing labor disputes or contract issues. Government agencies and embassies provide support for documented workers experiencing unfair treatment. Staying informed helps prevent decisions driven by fear, confusion, or misleading advice.

Managing Debt Wisely to Protect OFW Income

Managing debt wisely helps OFWs protect income and reduce financial stress. Avoiding unnecessary loans and focusing on paying high-interest debt improves cash flow. With a clear repayment plan, OFWs can prevent long-term financial strain and maintain better control over their hard-earned money.

Avoiding Debt That Does Not Add Value

Not all debt is harmful, but unnecessary debt weakens income protection. OFWs should avoid loans used for the following purposes:

- Lifestyle upgrades

- Non-essential purchases

- Covering repeated overspending

Debt should support productivity or true emergencies rather than habits that slowly drain income.

Paying Off High-Interest Debt Strategically

High-interest debt reduces income over time and increases financial pressure. Prioritizing repayment improves monthly cash flow and lowers stress. A clear and realistic repayment plan helps protect future income from long-term financial strain and prevents repeated reliance on borrowing.

Mental and Emotional Health in Financial Decisions

Mental and emotional health plays a major role in financial choices. Stress, loneliness, and fatigue can lead OFWs to make impulsive decisions. By prioritizing rest, support, and clear communication, OFWs can think clearly, manage pressure better, and protect their income more effectively.

Emotional Fatigue Leads to Poor Choices

Loneliness, stress, and burnout can affect judgment and lead to poor financial choices. OFWs under emotional strain may spend impulsively or agree to unfair requests. Protecting income also means caring for mental health through the following practices:

- Taking regular rest days

- Maintaining social connections

- Having honest conversations with family

A clear and rested mind supports better financial decisions.

Saying No Without Guilt

OFW income protection sometimes requires saying no, even when it feels uncomfortable. This does not mean abandoning family responsibilities. It means choosing long-term sustainability over short-term relief. Setting healthy boundaries helps protect income while supporting both the OFW and their family’s future.

Preparing for the Future Beyond Overseas Work

Preparing early for life after overseas work helps OFWs protect income and reduce uncertainty. Planning savings, building transferable skills, and exploring other income options provide stability. When future plans are clear, OFWs can transition with confidence and avoid financial pressure when contracts end.

Planning for Repatriation Early

OFW income protection includes preparing for the day overseas work ends. Early planning helps reduce financial risk and stress. OFWs should focus on the following areas:

- Clear savings goals

- Skills transferable to local or online work

- Basic retirement planning

Waiting until a contract ends often increases pressure and limits available financial options.

Building Multiple Income Paths

Relying on a single income source is risky for OFWs. Creating additional income options improves stability and flexibility. OFWs can explore the following opportunities:

- Online freelancing

- Remote work roles

- Small scalable ventures

Diversifying income sources helps protect earnings against sudden job loss or contract non-renewal.

Final Thoughts on OFW Income Protection

Protecting income is not driven by fear but by respect for hard-earned money and the sacrifices behind it. OFW income protection means making informed decisions, setting healthy boundaries, and choosing long-term stability instead of short-term comfort that may cause regret later.

Poor financial decisions often come from pressure, limited information, or emotional stress rather than irresponsibility. By improving financial awareness, strengthening skills, and planning ahead, OFWs can protect their income and build a more secure future for themselves and their families.

Every peso protected today is a step closer to freedom, security, and peace of mind tomorrow.

These related articles provide deeper insights and practical guidance for OFWs who want to strengthen income protection and long-term financial planning:

- Digital Tools OFWs Can Use to Track Career Progress

- How OFWs Can Prepare Financially Before Returning Home

- Financial Checklists Filipinos Should Complete Before Returning Home

- Best Productivity Habits Filipinos and OFWs Should Practice in 2026

- Simple Financial Systems Small Businesses Should Set Up Early

FAQs About OFW Income Protection

What is OFW income protection and why is it important?

OFWs protect income by budgeting carefully, setting remittance limits, building emergency funds, avoiding scams, and making informed decisions based on verified information.

What are common poor financial decisions made by OFWs?

Poor decisions include overspending, trusting unverified investments, lending money without agreements, ignoring contracts, and reacting emotionally, which often leads to long term financial stress abroad.

How does an emergency fund protect OFW income?

Emergency funds help OFWs avoid borrowing, selling assets, or accepting bad deals during crises, giving financial breathing space and protecting income stability over time periods.

How can OFWs avoid scams that target their income?

OFWs can avoid scams by researching opportunities, checking registrations, verifying sources, avoiding guaranteed returns, and refusing pressure based offers that demand quick decisions from strangers.

Why should OFWs set limits on remittances?

Setting remittance limits helps OFWs protect income by preventing overspending, encouraging family budgeting, reducing guilt driven decisions, and maintaining personal financial stability over the years.

How does learning new skills help with OFW income protection?

Learning new skills improves OFW income protection by increasing job options, supporting career shifts, boosting confidence, and reducing dependence on risky income sources abroad today.

Why is contract awareness important for OFWs?

OFWs should read contracts carefully, understand pay terms, check deductions, keep records, and ask questions to prevent income loss from unfair employment conditions overseas workplaces.

How does debt affect OFW income protection?

High interest debt weakens OFW income protection by reducing cash flow, increasing stress, and forcing poor decisions that affect long term financial security for families.

Can emotional stress lead to poor financial decisions?

Emotional stress affects judgment, causing impulsive spending or risky choices, so OFWs must prioritize rest, support systems, and clear thinking during overseas work periods abroad.

Why should OFWs plan early for life after overseas work?

Early planning helps OFWs protect income by preparing savings, skills, and alternatives before overseas work ends unexpectedly or contracts are not renewed in foreign countries.

Test your knowledge about How OFWs Can Protect Their Income From Poor Decisions

Results

#1. What is the main goal of OFW income protection?

#2. Which habit weakens OFW income protection most?

#3. Why are OFWs often targeted by scams?

#4. What helps prevent panic financial decisions?

#5. What should OFWs verify before investing?

#6. Why is budgeting important for OFWs?

#7. Which action protects income during job loss?

#8. How can skills protect OFW income?

#9. What weakens OFW income fastest?

#10. Why should OFWs plan early?

Thank you for taking time to learn and grow with ExpPH Blog.

Your commitment to smarter decisions today helps secure a stronger future tomorrow. Share your quiz experience with us in the comments. We would love to hear what you learned.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 10 Business Money Mistakes New Business Owners Must Avoid Now

Pingback: 7 Proven Ways to Build OFW Savings Despite Family Obligations