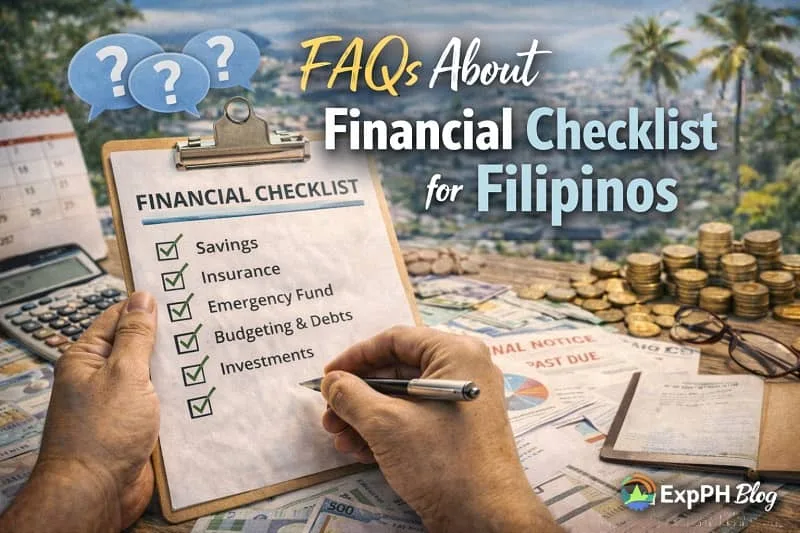

Financial Checklists Filipinos Should Complete Before Returning Home

Returning home to the Philippines after years of working abroad is a major life transition. For many Overseas Filipino Workers, it is a long-awaited milestone filled with excitement, relief, and new possibilities. At the same time, it can also be financially risky if the move is not carefully planned.

This Financial Checklist for Filipinos is designed to help you prepare with clarity and confidence. It focuses on real-life financial decisions that matter before you leave your host country and resettle back home. Whether you plan to retire, start a business, find local work, or spend more time with family, financial readiness will shape how smooth or stressful that transition becomes.

This guide is written for real people, especially OFWs, balikbayans, and returning migrants who want to protect their savings, avoid common mistakes, and build a stable next chapter in the Philippines.

Why a Financial Checklist for Filipinos Matters Before Returning Home

Many Filipinos return home with strong intentions but weak financial preparation. Some believe savings alone will last. Others overlook healthcare costs, income gaps, or daily expenses. Without a clear plan, even well-earned savings can disappear quickly during the adjustment period.

A proper Financial Checklist for Filipinos helps you:

- Avoid sudden cash shortages after returning

- Protect hard-earned savings from poor decisions

- Prepare for Philippine-specific expenses and systems

- Reduce financial stress for you and your family

- Transition income sources smoothly

Financial readiness is not about wealth. It is about preparation, discipline, and making informed decisions before coming home.

Understanding Your Return Timeline and Financial Goals

Clarifying your return timeline

Before managing your money, define your return timeline clearly. Are you coming home permanently within six months or returning temporarily to assess your situation? Your timeline determines how much cash should stay liquid and which expenses need priority. Short timelines require accessible funds. Longer timelines allow structured financial planning.

Defining your post-return lifestyle

Your lifestyle plans directly affect your financial readiness. Ask yourself these important questions before finalizing your Financial Checklist for Filipinos:

- Will you live in the city or province

- Will you support extended family

- Will you work immediately or rest first

- Do you plan to start a business

Your answers guide budgeting, savings use, and income planning decisions.

Reviewing All Sources of Income Before Leaving

Confirming your final overseas income

Before leaving, understand your complete final pay structure clearly. This includes all remaining earnings and benefits that may still be released after departure. Reviewing these details helps prevent missed payments and financial confusion later.

- Last salary payment

- Unused leave conversions

- End-of-service benefits or gratuity

- Tax refunds, if applicable

Always request written breakdowns and keep copies of payslips and employment contracts.

Avoiding premature income loss

Do not resign or end contracts without confirming how and when final payments will be released. Many OFWs lose access to income due to poor timing or account closures.

- Final payment release dates

- Bank access after departure

- Withdrawal rules for foreign accounts

Confirm these details first to protect your earnings.

Building a Return-Ready Emergency Fund

Calculating your minimum emergency fund

A solid Financial Checklist for Filipinos always includes an emergency fund. Before returning home, aim to save at least six months of essential living expenses based on Philippine costs. This fund protects you during job gaps or unexpected situations.

- Transportation

- Food and utilities

- Healthcare and medicines

- Family support obligations

If you plan to change careers or start a business, consider extending coverage to nine or twelve months.

Keeping emergency funds accessible

Do not lock emergency funds into long-term investments before returning home. These funds must be available when needed without penalties or delays. Accessibility matters more than returns during this transition period.

- High-liquidity savings accounts

- Accounts accessible immediately in the Philippines

Easy access ensures financial stability during unexpected events.

Auditing All Savings, Investments, and Assets

Listing all financial accounts

Create a clear and complete inventory of your finances before returning home. Listing every account helps you track your money, avoid forgotten funds, and plan consolidation when needed. This step strengthens control over your Financial Checklist for Filipinos.

- Overseas bank accounts

- Philippine bank accounts

- Investment accounts

- Time deposits

- Digital wallets

Having everything documented makes future decisions easier and more organized.

Reviewing investment maturity and penalties

Review each investment carefully to understand maturity dates and possible penalties. Some investments may be better withdrawn before returning, while others should remain untouched for long-term growth. Knowing these details prevents unnecessary losses and supports smarter financial timing decisions.

Managing Currency Exchange and Remittances Wisely

Timing your currency conversions

Avoid converting large amounts of money at one time without reviewing exchange conditions. While exchange rates cannot be predicted with certainty, spreading conversions over time helps reduce risk. This approach protects your savings from sudden rate changes before returning home.

Using reputable financial institutions

Always use trusted banks and licensed remittance centers when transferring or converting money. The Bangko Sentral ng Pilipinas offers updated guidance on regulated institutions and consumer protection through its official website. Using authorized channels helps safeguard your money and personal identity.

Closing or Maintaining Overseas Financial Accounts

Deciding which accounts to keep open

Some overseas accounts may remain useful even after returning home. Keeping the right accounts open can support future plans and provide flexibility, especially if you continue earning or traveling abroad.

- Receive foreign income

- Do freelance or remote work

- Travel internationally

Before deciding, review minimum balance rules and confirm reliable online access.

Avoiding dormant account penalties

If you keep overseas accounts open, make sure they remain active. Inactive accounts may incur dormancy fees or be closed automatically. Regular transactions and updated contact details help prevent unexpected penalties or loss of access to your funds.

Settling Taxes and Government Obligations Abroad

Confirming tax clearance

Before returning home, confirm that all tax and government obligations in your host country are fully settled. Unresolved issues can create problems later, even after you leave. Completing this step protects your finances and future travel plans.

- All required taxes are filed

- No outstanding penalties remain

- Required clearance documents are secured

Tax compliance gives peace of mind and avoids long-term complications.

Keeping official documentation

Organize and keep both digital and printed copies of all important records before leaving. Proper documentation helps resolve future questions related to employment, income, or legal matters.

- Tax filings

- Employment certificates

- Contracts

Secure storage ensures quick access whenever these documents are needed.

Reassessing Philippine Government Contributions

Checking SSS, PhilHealth, and Pag-IBIG status

Before returning home, review your SSS, PhilHealth, and Pag-IBIG contribution records. Make sure your payments are updated and your membership category is correct. Many returning OFWs need to shift from overseas status to voluntary or locally employed to avoid benefit gaps.

Planning contribution continuity

Maintaining regular government contributions supports long-term financial security after returning home. Continuous payments help ensure access to essential benefits and reduce problems during future claims or applications.

- Healthcare coverage

- Housing loan eligibility

- Retirement benefits

Consistent contributions protect your future and support a smoother financial transition.

Preparing Healthcare and Insurance Coverage

Reviewing health insurance needs

Healthcare expenses in the Philippines can be high, especially when using private hospitals. Before returning home, review your health coverage options carefully to avoid large out-of-pocket costs during emergencies or illness.

- PhilHealth coverage

- Private health insurance

- Critical illness plans

Having the right mix of coverage protects both your savings and your family.

Securing coverage before returning

It is usually easier and more affordable to secure insurance while you are still employed and in good health. Applying early increases approval chances and provides peace of mind before transitioning back to life in the Philippines.

Creating a Clear Post-Return Budget

Adjusting to Philippine cost structures

Living costs in the Philippines differ from overseas expenses. Some costs may drop, while others increase. Review common spending areas carefully to build a realistic and sustainable post-return budget.

- Transportation costs

- Family obligations

- School expenses

- Utility price changes

Understanding these differences helps prevent surprises and supports better money control.

Avoiding lifestyle inflation

Many returning Filipinos overspend during the first year because of celebrations, home improvements, or family expectations. A clear budget keeps spending aligned with priorities and protects savings while income stabilizes after returning home.

Planning for Income After Returning Home

Identifying realistic income options

Income planning is a core part of any Financial Checklist for Filipinos. Relying only on savings creates risk, especially during adjustment periods. Identify income sources that match your skills, location, and timeline before returning home.

- Local employment

- Remote or freelance work

- Consultancy or part-time roles

- Small business

Clear income planning supports stability and reduces pressure on savings.

Upskilling for income continuity

If your overseas experience does not easily transfer to local opportunities, upskilling becomes essential. Learning new or updated skills improves employability and opens alternative income paths. Preparing early helps you avoid long gaps without income after returning home.

Using online courses to prepare before returning home

One practical way to upskill is through online learning platforms like Udemy, which offers courses in freelancing, digital skills, bookkeeping, online business, and career transitions. Studying while abroad allows flexible and affordable preparation.

Many returning Filipinos use online courses to:

- Build income-ready skills before returning

- Prepare for freelancing or remote work

- Learn practical business and financial skills

- Increase confidence when changing careers

This approach reduces pressure and improves readiness once you are back home.

Evaluating Business Plans Carefully

Avoiding emotional business decisions

Many OFWs feel pressure to start a business as soon as they return home. While entrepreneurship can be rewarding, decisions driven by emotion often result in losses. Taking time to assess readiness helps protect savings and supports smarter long-term planning.

Conducting small-scale testing

Whenever possible, test business ideas on a small scale before committing large amounts of money. Observe local demand, pricing, operating costs, and competition. Small trials provide valuable insights and reduce the risk of costly mistakes.

Protecting Your Savings from Family Pressure

Setting financial boundaries

Returning home often brings expectations from relatives who may need help. While supporting family is important in Filipino culture, unplanned financial commitments can quickly reduce your savings. Setting clear limits protects your future and helps ensure long-term financial stability.

Communicating clearly

Explain your financial plan calmly and honestly to family members. Sharing your goals and limits builds understanding and reduces conflict. A clear Financial Checklist for Filipinos helps support your decisions and shows that your choices are based on careful planning.

Preparing Housing and Living Arrangements

Avoiding rushed property purchases

Avoid buying property immediately after returning home. Renting first gives you time to adjust and make better decisions based on real experience rather than emotion. This approach protects your savings and reduces regret.

- Reassess location preferences

- Observe actual living costs

- Avoid impulsive purchases

Taking time helps ensure long-term housing satisfaction.

Reviewing home renovation budgets

If you plan to renovate a family home, set clear budgets and realistic timelines before starting. Cost overruns are common when plans are vague. Clear limits help control spending and prevent renovation costs from draining your savings.

Consolidating Financial Records and Documents

Organizing physical and digital files

Before returning home, organize all important financial and personal records. Keeping documents in one secure place helps avoid delays when opening accounts, filing claims, or verifying income and identity.

- IDs and passports

- Employment records

- Bank statements

- Insurance documents

- Investment certificates

Well-organized records save time and reduce stress.

Backing up digitally

Create digital backups of all important documents and store them securely. Use encrypted cloud storage and offline devices such as external drives. Multiple backups protect your records from loss, damage, or theft during travel or relocation.

Preparing Mentally and Emotionally for Financial Adjustment

Understanding reverse culture shock

Returning home can feel unfamiliar even after years of planning. Daily routines, spending habits, and financial expectations may differ from what you imagined. This adjustment period can create stress, especially when reality does not match long-held expectations.

Practicing patience

Financial stability after returning home rarely happens immediately. Income rebuilding, budgeting, and lifestyle adjustments take time. Give yourself space to adapt, learn, and improve your situation gradually without rushing major financial decisions.

Common Financial Mistakes Filipinos Make When Returning Home

Spending too fast, too soon

Many returning Filipinos spend heavily during the first months through celebrations, gifts, and lifestyle upgrades. While generosity is part of Filipino culture, uncontrolled spending can quickly reduce savings and create financial stress before income stabilizes.

Ignoring long-term planning

Some returning Filipinos focus only on immediate comfort and daily needs. When retirement and long-term goals are ignored, savings may not last. Planning beyond the first year helps protect financial security and future independence.

Underestimating healthcare costs

Medical expenses can rise quickly, especially when using private hospitals. Without proper insurance or savings set aside for health needs, unexpected illness can drain funds and disrupt financial plans after returning home.

Creating Your Personalized Financial Checklist for Filipinos

Customizing based on your situation

Every return journey is different, so your Financial Checklist for Filipinos should reflect your personal circumstances. A checklist that fits your situation helps you plan realistically and avoid unnecessary stress after returning home.

- Age and family size

- Career stage

- Health condition

- Financial goals

Personalized planning improves clarity and decision-making.

Reviewing the checklist regularly

Review and update your checklist every few months as your return date approaches. Financial situations change over time, and regular updates help you stay aligned with new goals, expenses, and priorities before and after returning home.

Final Thoughts: Returning Home With Confidence and Financial Clarity

Returning home is more than a physical move. It is a major financial reset that shapes your next chapter. A well-prepared Financial Checklist for Filipinos helps protect your savings, reduce uncertainty, and guide better decisions as you adjust to life in the Philippines. Careful planning allows you to manage expenses, rebuild income, and avoid common mistakes that often cause stress during the first year of returning home.

For OFWs, financial preparation reflects self-respect and responsibility. Years of hard work abroad, time away from family, and personal sacrifices deserve lasting security. Planning your return with clear goals and disciplined actions helps turn those efforts into long-term stability. With patience, smart choices, and the right financial mindset, returning home can become one of the most fulfilling and rewarding chapters of your life.

Additional content connected to this topic is available next.

- Digital Tools OFWs Can Use to Track Career Progress

- How OFWs Can Prepare Financially Before Returning Home

- Healthy Routines for Filipinos Working Long Hours Overseas

- Simple Financial Systems Small Businesses Should Set Up Early

- Smart Budget Adjustments OFWs Should Make When Costs Increase

FAQs About Financial Checklist for Filipinos

What is the purpose of a financial checklist before returning home?

It helps returning Filipinos organize savings, income plans, obligations, and risks, so they avoid cash shortages, poor decisions, and stressful financial surprises after coming home.

When should Filipinos start preparing their financial checklist?

Ideally six months before returning home, giving enough time to settle obligations, build emergency funds, plan income, and adjust investments without rushing important financial decisions.

What are the most important items OFWs should prioritize?

OFWs should focus on emergency funds, tax clearance, government contributions, healthcare coverage, income transition plans, and protecting savings from impulsive spending or family pressure expectations.

Is income planning necessary if I have enough savings?

Yes, income planning is critical, because savings alone may not last, especially with rising costs, family needs, healthcare expenses, and business or job delays risks.

How can online courses help before returning home?

Online courses help returning Filipinos update skills, prepare for freelancing, remote work, or business, and reduce income gaps while adjusting to life back home financially.

What financial mistakes should returning Filipinos avoid?

Avoid rushing property purchases, spending too much early, ignoring healthcare costs, failing to plan income, and closing overseas accounts without checking access rules carefully first.

Should I keep my overseas bank accounts after returning?

It depends on future plans, but keeping active accounts can help with remote income, international payments, emergencies, or travel after returning home for added flexibility.

How much should my emergency fund cover?

An emergency fund should cover housing, food, utilities, transportation, healthcare, and family support, based on realistic Philippine living costs and personal circumstances during transition period.

Do I need to update my government contributions before returning?

Yes, reviewing SSS, PhilHealth, and Pag-IBIG contributions ensures continuous benefits, healthcare access, housing eligibility, and smoother financial reintegration after returning to the Philippines permanently prepared.

How can I stay financially disciplined after returning home?

Start early, write everything down, stay disciplined, seek reliable information, and review your financial checklist regularly as plans, goals, and circumstances change over time wisely.

Test your knowledge about Financial Checklists Filipinos Should Complete Before Returning Home

Results

#1. Why is a financial checklist important before returning home?

#2. How many months of emergency funds are recommended?

#3. Which fund should stay easily accessible?

#4. What should OFWs review before closing overseas accounts?

#5. Which expense is often underestimated after returning?

#6. What should be settled before leaving host country?

#7. What helps avoid fast money loss?

#8. What is a smart first housing move?

#9. Why is income planning important?

#10. What supports smoother career transition?

Thank you for taking time to learn and prepare for your return home.

Your financial awareness today builds a more secure tomorrow. Share your quiz experience and score in the comments. We would love to hear from you.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Proven Ways to Build OFW Savings Despite Family Obligations