How OFWs Can Build Emergency Security While Overseas

Building financial security while working abroad is one of the biggest concerns for Overseas Filipino Workers. Life overseas often comes with higher income, but it also carries higher risks. Job contracts can end suddenly, medical emergencies can happen without warning, and family needs back home do not stop when distance separates you. This is why creating a strong OFW emergency fund is not optional. It is essential.

An OFW emergency fund acts as your financial safety net. It protects you from sudden job loss, health issues, delayed salaries, and unexpected family emergencies in the Philippines. Without it, many OFWs are forced to rely on loans, credit cards, or urgent requests to family and friends, which can create long term financial stress.

This guide explains how OFWs can build emergency security step by step while overseas. It covers planning, saving, protecting income, using skills wisely, and avoiding common mistakes. Whether you are a new OFW or have been abroad for years, this article will help you build a stable financial foundation that protects both you and your family.

Understanding Why an OFW Emergency Fund Is Critical

What an OFW Emergency Fund Really Means

An OFW emergency fund is money reserved only for unexpected situations that threaten your income or well being. It is not meant for travel, shopping, or planned expenses. Its purpose is to protect you during difficult moments without damaging your long term financial stability.

For OFWs, emergencies may include sudden contract termination, delayed salaries, medical treatment abroad, or urgent family needs in the Philippines. Because these situations often require immediate action, having accessible emergency savings becomes essential for financial survival.

Having an OFW emergency fund allows you to respond calmly instead of reacting in panic. It gives you time to assess options, make informed decisions, and avoid relying on debt during stressful situations overseas.

Why Overseas Work Increases Financial Risk

Working abroad does not always guarantee stability. Many OFWs rely on fixed contracts, single employers, or strict visa conditions. Sudden policy changes, economic shifts, or workplace issues can end employment faster than expected.

Healthcare costs overseas can also be high, especially where foreign workers lack full coverage. Even with insurance, out of pocket expenses may still strain finances. These risks make a strong emergency fund essential for overseas workers.

Because of distance, currency differences, and legal requirements, OFWs face greater financial pressure during emergencies. This reality means OFWs must build a stronger emergency fund compared to workers based in the Philippines.

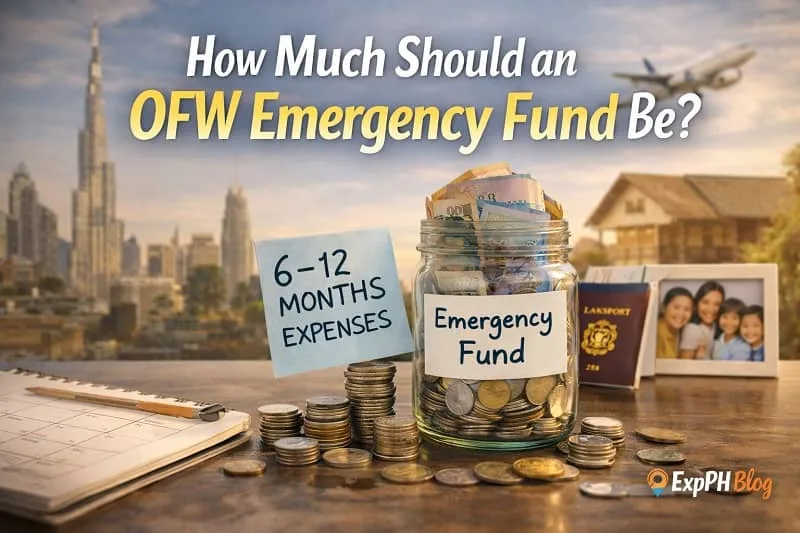

How Much Should an OFW Emergency Fund Be?

The Recommended Emergency Fund Size for OFWs

A common guideline is to save at least six months of living expenses. For OFWs, this includes overseas housing, food, transportation, remittances to family, insurance payments, and loan responsibilities that continue even during emergencies.

Some OFWs prefer saving nine to twelve months of expenses for added security. This approach is helpful when employment is unstable or when supporting extended family. Your OFW emergency fund should reflect your personal situation rather than follow a fixed formula.

Adjusting Emergency Fund Goals Based on Location

Emergency fund needs vary depending on where you work. An OFW in the Middle East may face different living and healthcare costs compared to someone in Europe or East Asia. Each location has unique financial demands.

Base your emergency fund goal on actual monthly expenses instead of estimates. Review spending regularly and adjust your savings target to stay realistic as living costs or responsibilities change over time.

Building an OFW Emergency Fund Step by Step

Step One: Separate Emergency Money From Daily Spending

The first rule of building an OFW emergency fund is keeping it separate from daily expenses. Emergency money should never be mixed with regular spending. Use a dedicated bank account that is accessible during emergencies but not easy to withdraw from casually.

Many OFWs choose savings or digital bank accounts with strong security features. While easy access matters in urgent situations, self discipline matters more. Clearly labeling the account as an emergency fund helps reduce the temptation to spend it unnecessarily.

Step Two: Automate Savings Whenever Possible

Automating savings removes emotion from financial decisions. If your employer pays monthly, set a fixed amount to transfer directly into your OFW emergency fund before spending anything else.

Even small automatic deposits grow over time. Consistency matters more than the amount, especially in the beginning. Automation also protects your savings from impulse purchases and lifestyle inflation as income increases.

Step Three: Start Small but Start Immediately

Many OFWs delay saving because the emergency fund goal feels overwhelming. Waiting only increases risk. Start with any amount you can afford, even if it feels small.

Building the habit of saving is more important than the initial amount. Once the habit is established, increasing contributions becomes easier and more sustainable over time.

Common Mistakes OFWs Make When Saving for Emergencies

Treating Emergency Funds as Extra Cash

One common mistake OFWs make is using emergency funds for non emergencies. Expenses like travel, gadgets, celebrations, or investments should never come from this savings. Emergency money exists only to protect you during serious financial or personal crises.

When emergency funds are spent casually, rebuilding becomes difficult. Always ask whether the situation truly threatens your income, health, or family stability. If it does not, avoid using your OFW emergency fund at all.

Depending Only on Loans and Credit

Some OFWs rely on loans or credit during emergencies instead of saving in advance. This approach often leads to long term debt, high interest costs, and added financial pressure during already stressful situations.

Loans should remain a last option, not a financial strategy. A solid OFW emergency fund helps you avoid borrowing and protects your future income and financial independence.

Protecting Your Income While Building an OFW Emergency Fund

Why Income Protection Matters

Saving money alone is not enough when income is unstable. Protecting your ability to earn is just as important as building savings. This means maintaining good work performance, following contract rules, and avoiding actions that could lead to job loss or legal problems. Your income fuels your OFW emergency fund.

Skills as Financial Protection

Skill development is one of the strongest ways to protect income. OFWs with transferable skills can find new work faster if a contract ends. Skills related to freelancing, digital work, or career growth create backup income options and reduce dependence on a single employer.

Using Online Learning to Strengthen Emergency Security

Upskilling helps OFWs prepare for sudden job loss or reduced income. Learning while overseas builds confidence and choices before emergencies occur. Many OFWs use Udemy to learn freelancing, digital skills, and career development that support income continuity and strengthen an OFW emergency fund strategy.

Managing Remittances Without Sacrificing Emergency Security

Balancing Family Support and Self Protection

OFWs often place family needs before personal financial security. While supporting loved ones is important, ignoring your own emergency fund can cause long term harm for everyone involved. Without protection, one crisis can stop your ability to help at all.

Clearly explain to your family why emergency savings matter. Honest financial communication reduces pressure and misunderstandings. Supporting family should never mean risking your own stability or survival overseas.

Setting Clear Financial Boundaries

Clear boundaries protect both relationships and finances. Set a fixed remittance amount and follow it consistently unless a true emergency arises. This approach helps maintain balance and predictability for everyone involved.

Your OFW emergency fund should never serve as family backup money. Its purpose is to protect your income and ensure you can continue supporting your family in the future.

Where OFWs Should Keep Their Emergency Fund

Local Bank vs Philippine Bank Accounts

OFWs choose different locations for keeping emergency funds based on their needs. Some prefer overseas banks for quick access, while others use Philippine banks to support family emergencies back home. Each option offers practical benefits depending on the situation.

Overseas accounts provide faster access during work related emergencies abroad. Philippine accounts help with urgent family needs. Many OFWs split their emergency fund between both locations to improve flexibility and access.

Liquidity Over Returns

Emergency funds should focus on safety and easy access rather than high returns. Avoid placing emergency savings in investments that require long holding periods or penalties for early withdrawal.

A modest interest rate is acceptable for emergency savings. Quick access and account security are more important than earning higher returns during emergencies.

Health and Legal Preparedness as Part of Emergency Security

Insurance as a Support Tool

Health and life insurance support an OFW emergency fund but cannot replace it. Insurance helps reduce the financial impact of medical emergencies, accidents, or unexpected events that may occur while working overseas. It works best when combined with accessible emergency savings.

OFWs should review insurance coverage regularly and understand the benefits and limits clearly. Never assume all expenses are covered. Knowing what is included helps avoid surprises and prevents unnecessary financial strain during emergencies.

Knowing Official Support Options

OFWs should stay informed about government assistance programs available during emergencies. The Overseas Workers Welfare Administration offers services such as repatriation support, welfare assistance, and emergency aid for qualified overseas workers.

Understanding these official support options adds another layer of protection. During large scale crises or sudden job disruptions, this knowledge can help OFWs respond faster and reduce financial and emotional stress.

Rebuilding After Using Your OFW Emergency Fund

Why Rebuilding Is Non Negotiable

Using your OFW emergency fund is not a failure. It means the fund worked as intended during a difficult situation. Once your condition stabilizes, rebuilding should start right away to restore your financial safety net.

Returning to regular saving habits, even with small amounts, is important. Delaying the rebuilding process increases vulnerability and leaves you exposed to future emergencies while overseas.

Learning From the Experience

Every emergency offers valuable lessons. Take time to review what worked well and what caused difficulties during the situation. This reflection helps you improve future preparedness and decision making.

Adjust your emergency fund size, saving approach, or income strategy based on what you learned. Progress comes from thoughtful evaluation, not from blame or regret.

Teaching Financial Security to Your Family

Involving Family in Financial Planning

Emergency security becomes stronger when family members understand its purpose. Share your financial goals, savings limits, and long term plans with those you support. Clear communication helps build trust and encourages cooperation during both stable periods and unexpected situations.

When families understand why emergency funds matter, unrealistic expectations are reduced. This shared understanding allows better planning and helps protect the OFW from unnecessary financial pressure during difficult times.

Creating a Culture of Preparedness

Encouraging family members to save, budget, and plan strengthens overall financial stability. Emergency security should be treated as a shared responsibility rather than a burden carried by one person.

When preparedness becomes a family value, everyone contributes to stability. This approach helps families respond calmly to emergencies and reduces reliance on one income source alone.

Conclusion: Why Every OFW Needs an Emergency Fund

An OFW emergency fund is more than a simple savings account. It represents protection, peace of mind, and freedom from financial panic during uncertain times. Having this fund allows Overseas Filipino Workers to respond to job loss, medical issues, or family emergencies with confidence and dignity instead of fear or rushed decisions. It provides stability when income is disrupted and helps maintain control over financial choices while living and working overseas.

Building emergency security requires consistent saving, income protection, skill development, clear boundaries, and careful planning. This preparation protects not only the OFW but also the family who depends on continued support. Emergency security is not built overnight. It grows through discipline, awareness, and long term thinking. When emergencies happen, and they eventually will, an OFW emergency fund can be the difference between crisis and recovery.

Related OFW Finance Guides You May Find Helpful

- How OFWs Can Build a Stable Financial Routine Abroad

- How OFWs Can Control Spending Despite Rising Living Costs

- Best Ways to Increase Income for Filipinos and OFWs in 2026

- Smart Budget Adjustments OFWs Should Make When Costs Increase

- How to Build a Strong Financial Foundation Using OFW Income in 2026

FAQs About OFW Emergency Fund

What is an OFW emergency fund?

An OFW emergency fund is money set aside for unexpected job loss, medical needs, or family crises, helping overseas workers avoid debt and financial panic.

How much should an OFW emergency fund be?

OFWs should save at least six months of living expenses, including overseas costs and remittances, to stay financially secure during emergencies or sudden employment disruptions.

How can OFWs start building an emergency fund?

Start by tracking expenses, separating savings from spending, and automating small deposits regularly until the emergency fund grows steadily without causing financial strain over time.

Can OFWs use emergency funds for non emergencies?

No, an emergency fund should only cover real emergencies like job loss or health issues, not vacations, gadgets, or planned personal spending and luxury purchases.

How can OFWs protect income while overseas?

OFWs can protect income by maintaining strong work performance, following contracts, and developing transferable skills that create backup job or freelance opportunities during emergencies abroad.

Why is skill development important for emergency security?

Upskilling helps OFWs find alternative income faster, reduce unemployment risks, and continue saving for an emergency fund if overseas work suddenly ends unexpectedly or permanently.

Should OFWs keep emergency funds overseas or in the Philippines?

Yes, many OFWs keep funds both overseas and in Philippine banks to ensure fast access during emergencies affecting work or family needs and obligations immediately.

What should OFWs do after using their emergency fund?

OFWs should rebuild immediately after using emergency funds by resuming savings, reviewing lessons learned, and adjusting goals to better handle future risks and uncertainties abroad.

How can families support an OFW emergency fund?

Clear communication helps families understand limits, respect savings goals, and reduce pressure that could weaken an OFW emergency fund during unexpected financial or personal crises.

Does insurance replace the need for an emergency fund?

Insurance reduces medical costs and financial shock, supporting an emergency fund, but it should complement savings rather than replace cash reserves for overseas Filipino workers.

Test your understanding of How OFWs Can Build Emergency Security While Overseas

Results

#1. What is the main purpose of an OFW emergency fund?

#2. How many months of expenses should OFWs aim to save?

#3. What should an emergency fund never be used for?

#4. Why is overseas work financially risky?

#5. What helps protect OFW income during emergencies?

#6. Where should OFWs keep emergency funds?

#7. Why should emergency savings be separate?

#8. What should OFWs do after using emergency funds?

#9. How can families help emergency security?

#10. Does insurance replace an emergency fund?

Thank you for taking this quiz and investing time in your financial security.

Your learning journey helps build a safer and stronger future for you and your family. Share your quiz experience in the comments and tell us what you learned.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.