How OFWs Can Avoid Lifestyle Inflation Overseas

For many Overseas Filipino Workers, working abroad brings higher income and new opportunities, but it also requires strong financial discipline. Better pay, favorable exchange rates, and modern conveniences can improve daily living. However, these benefits often introduce a hidden risk known as OFW lifestyle inflation. When spending increases at the same pace as income, savings stop growing and financial progress slows. Without careful control, higher earnings may not lead to long-term stability or real financial security.

Many OFWs do not notice lifestyle inflation until financial pressure begins to build. Small spending habits often feel harmless at first, but they gradually affect savings, goals, and future plans. Recognizing these patterns early is an important step toward long-term financial control and stability while working abroad.

This article serves as a practical guide on how OFWs can avoid lifestyle inflation overseas. It is written for real people facing real financial pressures, not for search engines. Whether you are newly deployed or have worked abroad for years, learning how to manage OFW lifestyle inflation can help protect your income, support your family, and keep your long-term goals within reach.

Understanding OFW Lifestyle Inflation

What OFW lifestyle inflation really means

OFW lifestyle inflation happens when spending increases mainly because income rises, not because needs change. This often appears through frequent upgrades like better housing, yearly phone replacements, regular dining out, or higher remittances. These habits feel manageable at first but slowly reduce savings and delay long-term financial goals.

Why lifestyle inflation is common among OFWs

Several factors make OFWs more vulnerable to lifestyle inflation, especially when adjusting to life overseas. These influences gradually shape spending habits if not managed early.

- Exposure to higher living standards abroad

- Sudden income increase versus local salaries

- Emotional need to reward sacrifices

- Easy access to credit and loans

- Family expectations back home

Without awareness, OFW lifestyle inflation slowly becomes routine spending behavior rather than a deliberate financial choice.

Why Avoiding OFW Lifestyle Inflation Is Critical

The hidden long-term cost

Lifestyle inflation rarely creates problems right away. Its impact often appears years later when OFWs realize that long overseas work did not translate into strong savings or clear retirement plans. Unchecked spending slowly weakens financial stability and future options.

OFWs who fail to control lifestyle inflation often experience the following challenges:

- Delayed home ownership

- Limited emergency savings

- Longer dependence on overseas employment

- Increased stress during contract or health issues

Avoiding OFW lifestyle inflation protects not only income but also long-term freedom and peace of mind.

The short overseas working window

Most OFW careers are not permanent. Age limits, health conditions, contract renewals, and economic shifts all affect job security. According to guidance from the Philippine government, overseas employment should ideally support long-term reintegration and financial stability, not endless dependency on foreign work. The Bangko Sentral ng Pilipinas regularly emphasizes the importance of saving, budgeting, and financial literacy for overseas Filipinos to prepare for eventual return and emergencies.

This makes managing OFW lifestyle inflation even more important.

Common Triggers of OFW Lifestyle Inflation

Upgrading housing too quickly

Many OFWs move to better housing once income becomes stable. Comfort matters, but upgrading too fast often causes rent to take a large share of earnings. This limits savings and investment growth. Delaying housing upgrades until savings and emergency funds are secure helps maintain financial balance.

Transportation and car ownership pressure

In some countries, owning a car feels necessary or linked to status. Monthly payments, insurance, fuel, and maintenance quickly increase expenses. Many OFWs overlook these combined costs. Before buying, consider whether public transport or shared rides can support daily routines at lower cost.

Gadget and brand-driven spending

New phones, watches, shoes, and branded items are easy to buy abroad. OFW lifestyle inflation grows through frequent upgrades influenced by convenience and social circles. Replacing gadgets only when they stop working, not when trends change, helps preserve monthly cash flow.

Family expectations back home

Family pressure is one of the hardest triggers to manage. Financial requests often rise as relatives assume overseas income is unlimited. Supporting family is meaningful, but it should be planned and consistent. Clear limits help protect long-term stability for both the OFW and loved ones.

Building the Right Mindset Against OFW Lifestyle Inflation

Separate income growth from lifestyle upgrades

One effective way to avoid OFW lifestyle inflation is to separate income growth from spending habits. A salary increase does not require lifestyle changes. Planning ahead helps direct extra income toward savings, investments, or debt reduction instead of unnecessary upgrades.

Understand needs versus rewards

OFWs deserve comfort and personal rewards, but balance is essential. Needs support daily health and function, while rewards should be occasional and intentional. Improving sleep with a better mattress is a need. Replacing a working phone every year is usually a reward.

Focus on financial freedom, not appearance

Many OFWs feel pressure to appear successful. Real success is not always visible. It is reflected in emergency savings, manageable debt, and the freedom to return home when ready. Avoiding OFW lifestyle inflation means valuing long-term security over outward display.

Practical Strategies to Avoid OFW Lifestyle Inflation

Create a zero-based budget abroad

A zero-based budget gives every peso or dollar a clear purpose. Income minus expenses equals zero because all money is planned in advance. This system helps OFWs control spending and limit lifestyle inflation by making financial choices intentional and visible.

Key budget categories should include:

- Savings

- Remittances

- Living expenses

- Emergency fund

- Personal spending

- Skill development or investment

This structure keeps money organized and prevents uncontrolled spending habits.

Automate savings and remittances

Automation removes the temptation to spend first. Setting automatic transfers to savings and emergency accounts right after payday ensures priorities are met. When savings happen before daily expenses, OFW lifestyle inflation becomes harder to sustain and easier to control.

Maintain a simple cost-of-living baseline

Choose a comfortable but modest lifestyle and stay consistent with it. Even as income grows, keep core expenses stable. This approach allows additional income to support long-term goals like savings and investments rather than short-term lifestyle upgrades.

Managing Family Expectations Without Conflict

Set clear financial boundaries early

Clear communication helps prevent misunderstandings with family members. Explain how much support you can provide each month and why consistency matters more than sudden increases. A stable remittance plan protects the OFW’s finances while allowing family members to plan responsibly.

Encourage financial responsibility at home

Supporting family does not mean carrying every financial burden alone. Encourage budgeting, small income activities, and basic financial education at home. Shared responsibility reduces pressure on the OFW and prevents lifestyle inflation caused by ongoing external demands.

Investing in Growth Instead of Lifestyle Upgrades

Why self-investment beats consumption

One effective way to reduce OFW lifestyle inflation is choosing skill development over material purchases. Skills can increase income and career options, while most consumer items lose value. Self-investment builds long-term stability, supports side income, and prepares OFWs for future work in the Philippines.

Choosing practical and income-focused skills

Practical skills connected to online work, freelancing, management, or technical fields offer strong value for OFWs. These skills can be learned during free time without leaving current jobs. Focused learning creates income opportunities without increasing daily living expenses.

Using online learning as a strategic tool

Affordable skill-building for OFWs abroad

Instead of spending on frequent lifestyle upgrades, many OFWs redirect a small portion of their budget toward learning platforms like Udemy. Online courses allow OFWs to build skills in freelancing, digital tools, business, and career development at their own pace.

This approach supports income growth without increasing daily living costs, which directly counters OFW lifestyle inflation. Learning once can create long-term earning potential, making it one of the smartest financial choices for overseas workers.

Avoiding Debt Traps That Fuel Lifestyle Inflation

Credit cards and installment plans

Credit cards offer convenience but can encourage overspending when used for lifestyle upgrades. Installment plans make costly items seem manageable even when unnecessary. OFWs should use credit only for planned expenses that fit within a clear budget and support financial goals.

Loans for non-essential purchases

Loans for gadgets, travel, or luxury items quickly increase lifestyle inflation. Interest payments reduce future income and create added pressure. Debt should be reserved for emergencies or productive purposes, not for purchases that do not improve long-term financial stability.

Tracking Progress and Staying Accountable

Monthly financial check-ins

Set a monthly routine to review expenses, savings, and financial goals. Comparing spending patterns helps identify lifestyle creep early. Regular tracking keeps OFW lifestyle inflation visible, allowing timely adjustments before small habits turn into long-term financial problems.

Adjusting goals as life changes

Life abroad is not static. Income levels, family needs, and personal priorities change over time. Adjust budgets and goals as needed without losing discipline. This balance allows flexibility while maintaining control over spending and long-term financial direction.

Planning for the Long Term as an OFW

Building a strong emergency fund

An emergency fund protects OFWs from job loss, health problems, or sudden return home. It should cover at least six months of living expenses. Without this buffer, lifestyle inflation becomes risky and can quickly disrupt financial stability during unexpected situations.

Preparing for reintegration in the Philippines

Many OFWs plan to return to the Philippines in the future. Savings, skills, and investments should support this move. Avoiding OFW lifestyle inflation helps ensure a smoother transition, reduces financial stress, and provides more options when starting a new chapter at home.

Emotional Traps That Lead to Lifestyle Inflation

Rewarding stress with spending

Working overseas can be emotionally exhausting. Many OFWs cope by shopping or eating out more often. Recognizing stress-driven spending is important. Replacing these habits with healthier rewards helps control expenses and prevents lifestyle inflation from becoming an emotional response.

Comparing lifestyles with other OFWs

Social media often shows only highlights, which creates unrealistic comparisons. Not shown are debts or financial struggles behind those images. Focusing on personal goals rather than other OFWs’ lifestyles helps maintain discipline and reduces pressure to spend for appearance.

Teaching Financial Discipline to the Next Generation

Setting an example for family members

Children and relatives often learn money habits by observation. When OFWs practice discipline, budgeting, and controlled spending, they set a strong example. Avoiding lifestyle inflation shows the value of long-term thinking and responsible decision-making that family members can follow.

Encouraging savings and planning at home

Simple practices like saving part of allowances or planning household expenses help build shared financial values. These habits reduce reliance on overseas income. Encouraging responsibility at home eases pressure on the OFW and supports long-term family independence.

Long-Term Benefits of Avoiding OFW Lifestyle Inflation

Greater financial security

OFWs who control lifestyle inflation build stronger savings and maintain lower debt levels. This creates more room for investments and emergency funds. Financial security reduces daily stress, improves confidence, and allows OFWs to handle unexpected challenges without relying on loans or continued overseas work.

Freedom of choice

Financial discipline gives OFWs real options in life. They can choose to stay abroad, return home, start a business, or change careers with less fear. Avoiding lifestyle inflation provides the freedom to decide based on goals rather than financial pressure.

Conclusion: Choosing Control Over Comfort

OFW lifestyle inflation is not a sign of personal failure. It is a common challenge faced by many Filipinos adjusting to higher income and unfamiliar environments overseas. The real difference between financial struggle and long-term success lies in awareness, discipline, and intentional decision-making. When OFWs understand how spending habits grow over time, they gain the ability to control money instead of reacting to convenience, pressure, or comparison with others.

By managing spending, setting clear financial boundaries, investing in useful skills, and keeping long-term goals in focus, OFWs can enjoy the rewards of working abroad without sacrificing their future stability. Comfort has its place, but control creates security and peace of mind. Avoiding OFW lifestyle inflation is not about denying enjoyment or living in hardship. It is about choosing direction and purpose. Every peso saved, every skill developed, and every thoughtful choice moves OFWs closer to financial freedom and a secure life beyond overseas employment.

Continue engaging with similar content below.

- Daily Expenses OFWs Often Underestimate Abroad

- What Most OFWs Wish They Knew Before Working Abroad

- Best Saving Strategies for Filipinos With Overseas Income in 2026

- Best Financial Mistakes Filipinos Should Avoid in 2026

- Best Reintegration Plans for Returning OFWs in 2026

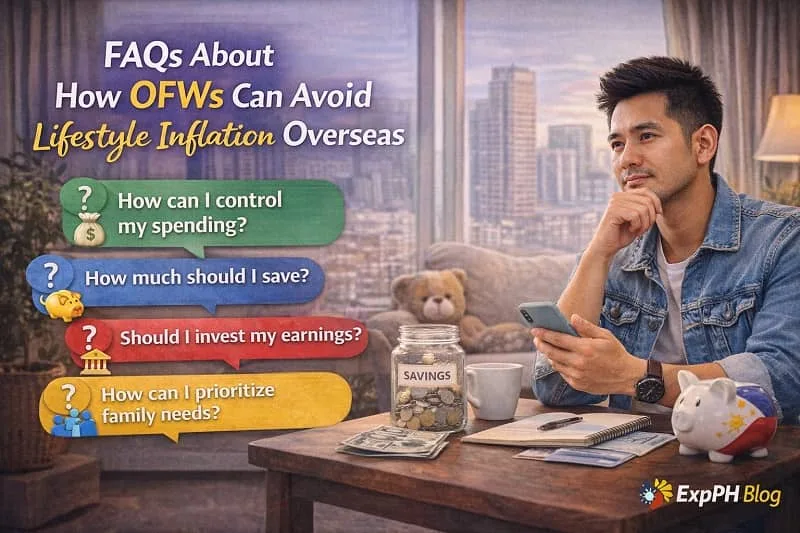

FAQs About How OFWs Can Avoid Lifestyle Inflation Overseas

What is lifestyle inflation for OFWs?

Lifestyle inflation happens when OFWs increase spending as income rises abroad, reducing savings and delaying long-term financial goals despite earning higher salaries.

Why are OFWs more prone to lifestyle inflation overseas?

OFWs experience higher incomes, better amenities, and social pressure abroad, which can encourage frequent upgrades in housing, gadgets, travel, and daily spending habits.

How can OFWs recognize early signs of lifestyle inflation?

Early signs include reduced savings, frequent nonessential purchases, increasing monthly expenses, and difficulty maintaining a consistent budget despite stable or rising income.

What is the best way for OFWs to control spending abroad?

Creating a clear monthly budget, automating savings, and separating needs from wants help OFWs maintain financial discipline and avoid unnecessary lifestyle upgrades.

How does family pressure contribute to OFW lifestyle inflation?

Increased financial requests from family can raise monthly obligations, making it harder for OFWs to save, invest, and control long-term spending patterns.

Should OFWs avoid enjoying their income while working abroad?

No. OFWs should enjoy reasonable comforts, but rewards should be planned, balanced, and aligned with savings goals instead of becoming constant spending habits.

How can skill-building help OFWs avoid lifestyle inflation?

Learning new skills redirects money from consumption to self-improvement, increases future income potential, and supports financial growth without raising living expenses.

Why is avoiding debt important in controlling lifestyle inflation?

Debt from nonessential purchases increases monthly expenses, adds interest costs, and limits savings, making lifestyle inflation harder to reverse over time.

How can OFWs maintain financial discipline long-term?

Regular expense tracking, clear financial goals, and periodic budget reviews help OFWs stay disciplined and adjust spending as income or circumstances change.

What are the long-term benefits of avoiding OFW lifestyle inflation?

OFWs gain stronger savings, reduced stress, greater financial freedom, and better preparation for emergencies, reintegration, or retirement after overseas employment.

Test your knowledge and see how well you understand OFW lifestyle inflation.

Results

#1. What does OFW lifestyle inflation mean?

#2. Why is lifestyle inflation risky for OFWs?

#3. Which habit best prevents lifestyle inflation?

#4. What usually triggers lifestyle inflation abroad?

#5. Which expense should OFWs control first?

#6. How can OFWs manage family expectations?

#7. Why is debt dangerous for OFWs?

#8. What mindset helps avoid lifestyle inflation?

#9. Which action supports long-term OFW goals?

#10. What is the main benefit of avoiding lifestyle inflation?

Thank you for taking your time with us.

Share your experience. Comment below and tell us how this quiz helped you reflect on your spending habits overseas.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Easy Steps to Build an OFW Financial Routine Abroad Today.

Pingback: 7 Proven OFW Budgeting Tips to Beat Rising Living Costs 2026

Pingback: 7 Proven Ways to Improve OFW Productivity During Long Hours!