Best Remittance Options for OFWs in 2026 (Including US-Based OFWs)

Sending money home is one of the most important responsibilities of every Overseas Filipino Worker. In 2026, remittance is no longer just about transferring cash. It is about speed, safety, affordability, and ensuring that hard-earned money reaches loved ones in the most efficient way possible. With new digital platforms, updated banking policies, and changing OFW needs, choosing the best remittance options for OFWs has become more important than ever.

This guide is designed to help OFWs make informed decisions when sending money to the Philippines, whether you are based in the United States, the Middle East, Europe, or Asia. We will explore trusted remittance channels, compare traditional and digital methods, highlight special considerations for US-based OFWs, and show how remittances can support long-term family stability and income.

This article is written for real OFWs and their families, with practical advice, clear explanations, and updated insights for 2026.

Understanding Remittance Needs of OFWs in 2026

The way OFWs send money has changed greatly over time. Many older methods are no longer the most practical or affordable. In 2026, OFWs must consider speed, safety, and ease of access to ensure their families receive support without delays or unnecessary costs.

Changing Financial Priorities of OFWs

In 2026, OFWs send money for more than daily household needs. Remittances now support education, healthcare, savings, and small family businesses. This shift means OFWs need remittance options that are flexible, reliable, and suitable for both short-term needs and long-term financial goals.

Many remittances now support:

- Emergency savings

- Education and tuition fees

- Medical and health-related needs

- Housing and home improvements

- Small businesses and online selling

- Digital payments and e-wallet usage

Because OFWs support many different family needs, remittance services must be flexible and dependable. Families in the Philippines should be able to receive funds easily through banks, cash pickup, or digital wallets, ensuring money is accessible, secure, and useful for daily expenses, emergencies, and long-term financial plans.

What Makes a Remittance Option “Best”

Not all remittance services provide the same value. The best remittance option should offer reasonable fees, fast transfer times, and strong security. It should also be convenient for both OFWs and their families, making it easy to send and receive money without stress or unnecessary delays.

Key factors OFWs should consider include:

- Low transfer fees

- Fast processing time

- Strong customer support

- Competitive exchange rates

- Wide availability in the Philippines

- Secure and regulated platforms

Understanding these criteria helps OFWs choose a remittance service that suits their needs. When cost, speed, security, and access are considered together, OFWs can send money with confidence, knowing their families will receive support reliably and without complications that could affect daily living or long-term plans.

Traditional vs Digital Remittance Methods

Before choosing a remittance provider, OFWs should understand the two main types of services available today. Traditional and digital methods differ in cost, speed, and convenience. Knowing how each option works helps OFWs select a service that fits their lifestyle and family needs.

Traditional Remittance Services

Traditional remittance services have existed for many years and remain trusted by many OFWs. These methods are often familiar and widely available, especially in countries with large Filipino communities. However, they may involve higher costs and require more time to complete transactions.

Banks and International Wire Transfers

Banks provide secure and regulated money transfers that appeal to OFWs who value stability. However, fees are often higher and processing times can take several business days. Exchange rates may also be less favorable, making banks better for large transfers rather than frequent remittances.

Remittance Centers and Money Transfer Offices

Remittance centers allow OFWs to send money in person and receive assistance when needed. These services are common in areas with many OFWs and offer familiarity and cash-based transactions. However, long queues and limited hours can make them less convenient than digital options.

Pros:

- Face-to-face assistance

- Cash-based transactions

- Familiar process

Cons:

- Long lines during peak seasons

- Fixed operating hours

- Higher fees compared to digital options

Digital and Online Remittance Platforms

Digital remittance platforms are now the preferred choice for many OFWs in 2026. These services offer convenience, faster processing, and better control over transactions. With improved security and wider access in the Philippines, digital options continue to replace traditional remittance methods.

Mobile Apps and Online Transfers

Mobile apps and online transfer services allow OFWs to send money using smartphones or computers with ease. These platforms often provide lower fees and quicker transfers. They also offer tracking features, making it easier for OFWs and families to monitor transactions and manage finances confidently.

Advantages include:

- 24/7 availability

- Faster processing, sometimes within minutes

- Transparent fees and exchange rates

- Direct bank or e-wallet deposits

For many OFWs, digital platforms have become the best remittance options for OFWs. They offer convenience, lower fees, and faster transfers compared to traditional methods. These benefits allow OFWs to send money regularly while ensuring families receive funds quickly and without unnecessary costs or delays.

Best Remittance Options for OFWs Based on Speed and Cost

Every OFW has different priorities when sending money home. Some focus on fast delivery, while others aim to reduce transfer costs. Understanding how speed and fees affect remittance choices helps OFWs select services that match their family’s financial needs and timing requirements.

Best for Fast Transfers

When families need money urgently, transfer speed becomes essential. Digital remittance platforms and e-wallet services are usually the fastest options available. Many allow instant or same-day transfers directly to Philippine banks or mobile wallets, making them ideal for emergencies and urgent expenses.

These are ideal for:

- Medical needs

- Emergency expenses

- Time-sensitive payments

Best for Low Fees

For OFWs who send money regularly, transfer fees can become costly over time. Choosing remittance services with lower fees and fair exchange rates helps maximize the amount received by families. This approach allows OFWs to support household needs while keeping long-term remittance expenses under control.

Online remittance platforms usually offer:

- Lower service fees

- Better exchange rates than physical outlets

- Discounts for frequent users

When selecting a remittance service, OFWs should look beyond advertised fees. Total transfer cost includes exchange rates, processing charges, and delivery methods. Comparing the full amount received by families helps OFWs choose the best remittance options for OFWs with confidence and avoid hidden costs.

Special Guide for US-Based OFWs

OFWs based in the United States face different remittance considerations because of local banking systems and regulations. Available services vary in fees, processing time, and transfer methods. Understanding these differences helps US-based OFWs choose reliable options that suit their financial habits and family needs in the Philippines.

US-based OFWs often use:

- Online money transfer services linked to US bank accounts

- Debit card funded remittance platforms

- Direct bank-to-bank transfers

These remittance options give OFWs greater flexibility when sending money home. Many services offer competitive exchange rates and multiple transfer methods. This allows OFWs to choose solutions that match their schedules and budgets while ensuring families receive funds quickly and securely when needed.

Tips for US-Based OFWs Sending Money in 2026

US-based OFWs should compare exchange rates regularly and choose services with transparent fees. Sending money during weekdays can help secure better rates. It is also important to confirm that family members can easily access funds through banks, cash pickup locations, or digital wallets in the Philippines.

To maximize value, US-based OFWs should:

- Compare exchange rates daily

- Use services with transparent fee structures

- Avoid weekend transfers when rates may be less favorable

- Ensure recipients have access to banks or e-wallets

By following these practical tips, US-based OFWs can choose the best remittance options for OFWs with greater confidence. Careful planning, rate comparison, and choosing accessible services help reduce extra costs while ensuring families receive money on time and without complications.

Security and Compliance in Remittance Transactions

Security remains a major concern for OFWs and their families when sending money home. Choosing regulated remittance services helps protect funds and personal information. Secure platforms also provide peace of mind by reducing the risk of fraud, delays, and transaction errors during transfers.

OFWs should always:

- Use licensed and regulated remittance services

- Avoid sharing personal information through unsecured channels

- Double-check recipient details before confirming transfers

Keeping digital or printed records of remittance transactions is important for:

- Personal budgeting

- Dispute resolution

- Proof of support for family-related documentation

Reliable remittance providers give OFWs easy access to transaction histories and receipts. These records help track spending, confirm successful transfers, and resolve issues if problems arise. Keeping clear documentation also supports better financial planning and provides reassurance that money reaches the intended recipients.

Using Remittance Beyond Daily Expenses

In 2026, many OFWs are planning beyond immediate needs. Remittance is now used to build financial stability and prepare for the future. When managed well, regular money transfers can support savings, reduce financial stress, and help families work toward long-term security.

Supporting Savings and Emergency Funds

Setting aside a portion of remittance for savings or emergency funds helps families handle unexpected expenses. This habit creates a financial safety net for medical needs, repairs, or temporary income loss, giving families greater confidence and stability during difficult situations.

Funding Small Businesses and Side Hustles

Many OFWs now use remittance to support small family businesses. Online selling and simple ventures allow families to earn additional income. This approach helps reduce reliance on remittance alone and encourages long-term financial independence at home.

This approach helps:

- Create additional household income

- Reduce dependence on remittance alone

- Build long-term financial independence

Using Remittance to Support Online Selling and Family Income

One practical way families use remittance funds is by supporting online selling through local platforms in the Philippines. For example, families may use remittance money to purchase initial inventory, packaging materials, or marketing tools for online stores.

Platforms like Shopee Philippines make it easier for OFW families to start small online businesses without large capital. Families can use remittance funds to buy supplies, test products, and gradually build income streams.

If your family plans to explore online selling as a side income, you can check Shopee Philippines as a helpful resource for sourcing products and managing small online stores: https://shopee.ph

This approach allows remittances to serve not only immediate needs but also long-term financial growth.

Choosing the Best Remittance Options for OFWs Based on Family Access

The best remittance option does not depend only on the sender. It must also suit the needs of the recipient. Families should be able to receive funds easily through banks, cash pickup locations, or digital wallets without added difficulty or delay.

Banked vs Unbanked Recipients

Some families have bank accounts, while others depend on cash pickup services or digital wallets. OFWs should consider how their families access money when choosing a remittance service. Matching the service to recipient access helps ensure funds are received smoothly and on time.

OFWs should confirm:

- Whether recipients prefer bank deposits or cash pickup

- Proximity to banks or remittance centers

- Familiarity with mobile wallets

Urban vs Provincial Considerations

Families in urban areas often have easy access to banks and digital payment services. In provincial locations, options may be limited to cash pickup centers or mobile wallets. OFWs should choose remittance services that work well in their family’s location to avoid delays or inconvenience.

Families in provinces may have limited access to banks but easier access to:

- Cash pickup locations

- Mobile wallet agents

- Local payment centers

Choosing a remittance service that works well in your family’s location is essential. Accessibility affects how quickly and easily funds are received. When OFWs consider local availability, payment options, and service coverage, they can select the best remittance options for OFWs with greater confidence and fewer complications.

Exchange Rates and Hidden Costs Explained

Many OFWs pay attention to transfer fees but often overlook exchange rates. Exchange rates directly affect how much money families receive. Even small differences can reduce the total value of remittance, making it important to consider the full cost of every transfer.

Why Exchange Rates Matter

A slightly lower exchange rate may seem minor at first but can cause meaningful losses over time. For OFWs who send money regularly, these small differences add up, reducing the overall support families receive throughout the year.

Always check:

- Real-time exchange rates

- Differences between advertised and actual rates

- Total amount received by the beneficiary

How to Compare Total Transfer Value

Instead of asking, “How much is the fee,” ask:

“How much will my family actually receive in pesos?”

Adopting this mindset helps OFWs recognize the true best remittance options for OFWs. By focusing on total value received rather than advertised fees alone, OFWs can make smarter choices that protect their earnings and ensure families benefit fully from every transfer.

Remittance Planning Tips for Long-Term OFWs

Careful remittance planning can greatly improve long-term financial results. When OFWs send money with clear goals, they can support daily needs while also building stability. Planning ahead helps families manage expenses, avoid financial pressure, and prepare for future responsibilities.

Set a Regular Remittance Schedule

Sending money on a consistent schedule helps families plan their budgets with confidence. Regular transfers reduce uncertainty and allow households to manage expenses more effectively. This approach also helps OFWs track spending and maintain better control over their finances over time.

Combine Remittance with Financial Education

Pairing remittance with financial education empowers families to manage money wisely. Learning basic budgeting, saving, and planning skills helps families use remittance more effectively. This combination supports long-term stability and reduces dependence on overseas income alone.

Encourage family members to:

- Track expenses

- Save consistently

- Invest in income-generating activities

Remittance becomes more effective when families understand how to manage money responsibly. Financial awareness helps recipients budget properly, save consistently, and make informed decisions. When combined with regular remittance, these skills support long-term stability and allow families to maximize the benefits of every amount received.

Future Trends in OFW Remittance Beyond 2026

The remittance landscape will continue to change as technology and regulations improve. OFWs can expect more convenient services, faster transfers, and better cost transparency. Staying aware of these trends helps OFWs adapt and make informed decisions when sending money home.

Digital Wallet Expansion

The remittance landscape will continue to change as technology and regulations improve. OFWs can expect more convenient services, faster transfers, and better cost transparency. Staying aware of these trends helps OFWs adapt and make informed decisions when sending money home.

Faster Cross-Border Transfers

Digital wallets are becoming more widely accepted across the Philippines. More merchants now support cashless payments, making e-wallet remittance more practical for daily expenses. This shift allows families to receive and use funds easily without relying solely on cash or bank visits.

Greater Transparency

Advancements in financial technology continue to shorten transfer times. Many remittance services now offer same-day or near-instant transfers. Faster processing helps OFWs respond quickly to family needs, especially during emergencies or time-sensitive situations.

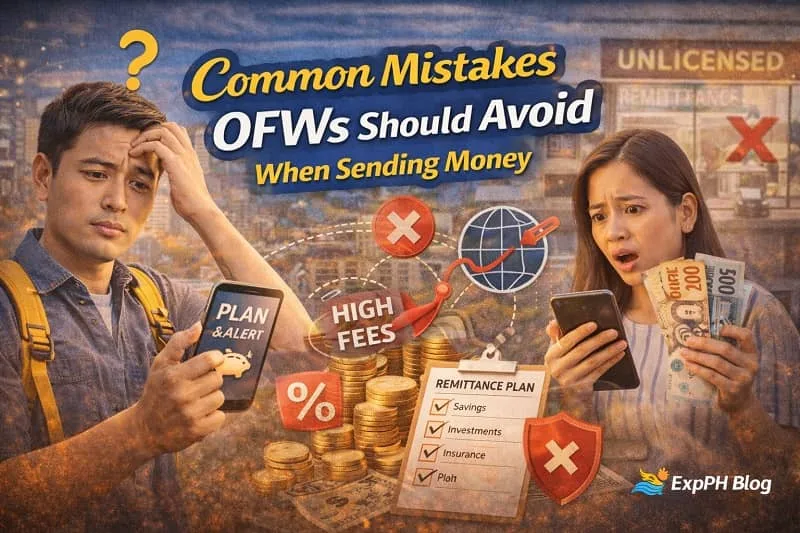

Common Mistakes OFWs Should Avoid When Sending Money

Even experienced OFWs can make mistakes when sending money home. Common issues include choosing services without comparing costs, ignoring exchange rates, or using unfamiliar channels. Being cautious and informed helps OFWs protect their earnings and ensure families receive funds safely and on time.

Common pitfalls include:

- Ignoring exchange rates

- Choosing services based only on brand familiarity

- Sending money without confirming recipient access

- Using unverified or informal channels

Avoiding these mistakes helps protect both your money and your family’s financial security. Careful planning, service comparison, and attention to details reduce the risk of delays or losses. When OFWs stay informed, they can send remittance with confidence and peace of mind.

Final Thoughts on the Best Remittance Options for OFWs in 2026

Choosing the best remittance options for OFWs in 2026 goes beyond convenience. It involves protecting hard-earned income, supporting families effectively, and planning for the future. The right remittance service helps ensure money reaches loved ones safely and on time while reducing unnecessary costs that can affect long-term financial stability.

Understanding available remittance options allows OFWs to make smarter financial decisions. By comparing services, focusing on security, and aligning remittance with long-term goals, money transfers become tools for stability and growth. As systems improve, OFWs who stay informed can adapt easily and ensure every peso sent home provides real value for their families.

Discover more reading options right after this content.

- Top OFW Banking Apps: Banking, Remittance, Communication & Safety Apps

- Cashless Payments in the Philippines in 2026

- How to Send Money to the Philippines Safely

- How to Manage Finances Abroad for OFWs

- Top 5 Budgeting Apps for Filipinos in 2026

For all official references, click the link below.

- Bangko Sentral ng Pilipinas – Personal Remittances (Official data and updates)

- Bangko Sentral ng Pilipinas – OF Portal FAQs on Remittances (Official guide for OF remittances)

- Overseas Filipino Bank (state-owned bank focused on OFWs and financial services)

- Philippine Statistics Authority – Overseas Filipino Workers (OF) Statistical Tables

- National Economic and Development Authority – NEDA News on Remittances

FAQs About Best Remittance Options for OFWs in 2026

What are the best remittance options for OFWs in 2026?

The best remittance options for OFWs in 2026 offer low fees, competitive exchange rates, fast transfers, secure platforms, and convenient access for families nationwide.

Which remittance method is fastest for OFWs sending money home?

Digital remittance platforms are usually fastest, offering same-day or instant transfers directly to Philippine banks or e-wallets, especially for urgent family needs.

Are online remittance services safe for OFWs in 2026?

Yes, reputable online remittance services are safe when licensed and regulated, using encryption, identity verification, and transaction tracking to protect OFWs and recipients.

What should OFWs consider when choosing a remittance provider?

OFWs should consider transfer fees, exchange rates, delivery speed, recipient access options, customer support, and overall reliability when choosing a remittance provider.

Are remittance fees higher for US-based OFWs?

Remittance fees for US-based OFWs vary by provider, but many online platforms offer competitive rates and lower costs compared to traditional bank transfers.

Can OFWs send remittance directly to e-wallets in the Philippines?

Yes, many remittance services allow OFWs to send money directly to Philippine e-wallets, making funds easily accessible for daily expenses and digital payments.

How often should OFWs send remittance to their families?

Remittance frequency depends on family needs, but many OFWs send money monthly to support budgeting, stability, and consistent household financial planning.

What is the safest way to avoid remittance scams?

OFWs can avoid scams by using licensed remittance providers, verifying recipient details carefully, and avoiding unofficial channels or unverified online transfer offers.

Can remittance be used for OFW family businesses?

Yes, many OFWs use remittance funds to support family businesses, online selling, or small ventures that help generate additional household income.

Why is comparing exchange rates important for OFWs?

Comparing exchange rates is important because even small differences affect total peso value received, especially for OFWs sending money regularly over time.

Test your knowledge about the Best Remittance Options for OFWs in 2026.

Results

#1. What is the main goal of remittance for OFWs?

#2. Which factor matters most when choosing remittance services?

#3. Which remittance option is usually fastest?

#4. Why do OFWs compare exchange rates?

#5. Which method suits emergency remittance needs?

#6. What should OFWs avoid when sending money?

#7. What benefit do digital remittance apps offer?

#8. How can remittance support long-term goals?

#9. What do US-based OFWs often use?

#10. Why is recipient access important?

We would love to hear from you.

Please comment below and share your quiz experience with us, including what you learned or what topic you want next.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: Best Digital Banks for Filipinos and OFWs 2026 Guide Updated

Pingback: Best Investment Options for OFWs in 2026 Practical Guide Now