Best Insurance Options for OFWs in 2026

Overseas Filipino Workers face risks that are very different from those of workers based in the Philippines. Long working hours, foreign healthcare systems, contract uncertainty, and family separation all make financial protection a serious priority. As global conditions continue to change, choosing the right insurance is no longer optional. It is a form of responsibility both for the OFW and for the family depending on them.

This guide to OFW insurance 2026 is designed to help overseas Filipinos make informed, practical, and future ready decisions. Instead of confusing policy jargon, this article focuses on real life needs, realistic budgets, and long term protection.

Whether you are newly deployed, renewing a contract, or planning to return home in the future, understanding your insurance options is one of the smartest moves you can make this year.

Understanding Why OFW Insurance Matters More in 2026

Insurance has always played an important role for overseas workers. In 2026, growing global uncertainty makes proper coverage more necessary than ever. Changes in healthcare systems, employment contracts, and migration policies increase risks that OFWs must prepare for through reliable insurance protection.

Healthcare costs overseas continue to increase, while job security remains uncertain in many destinations. Families in the Philippines often depend on regular remittances. When illness, injury, or job loss occurs, even short interruptions can quickly lead to serious financial pressure for both OFWs and their loved ones.

OFW insurance 2026 goes beyond basic compliance or required documents. It focuses on protecting income, maintaining access to medical care, and preventing families from facing financial hardship during emergencies. Proper insurance provides stability, confidence, and peace of mind while working abroad.

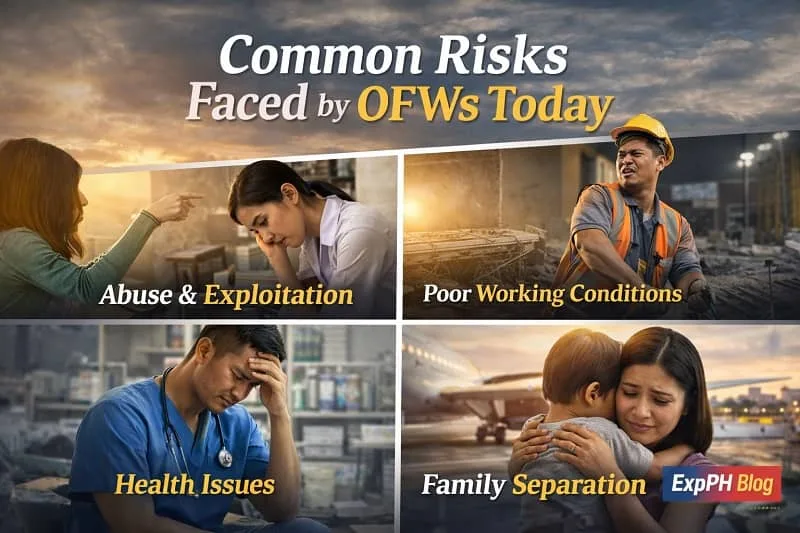

Common Risks Faced by OFWs Today

Before choosing any insurance policy, OFWs should understand the real risks they face while working abroad. Knowing these challenges helps workers select coverage that matches their job conditions, destination country, and personal responsibilities, instead of relying on assumptions or incomplete protection.

Many OFWs face medical emergencies in countries with costly healthcare systems. Workplace accidents are common in labor intensive jobs. Sudden contract termination, employment disputes, and long term illness can also affect income stability and the ability to support families back home.

Mental health has become a growing concern for overseas workers, especially those working long hours with limited support. Insurance serves as a financial buffer during these situations, allowing OFWs to focus on recovery and well being rather than worrying about medical bills or lost income.

Legal and Mandatory Insurance Requirements for OFWs

Some insurance coverage is legally required for OFWs based on deployment status and host country rules. The Philippine government mandates specific protections for overseas workers, especially those deployed through licensed recruitment agencies.

According to official guidelines from the Department of Migrant Workers, which oversees OFW deployment and welfare, agency hired OFWs are entitled to compulsory insurance coverage that includes life, accident, and repatriation benefits, as outlined on the official government website.

While this mandatory insurance provides a basic level of protection, it is often not enough to cover long term medical needs, income replacement, or broader family security goals, which is why many OFWs choose additional private coverage.

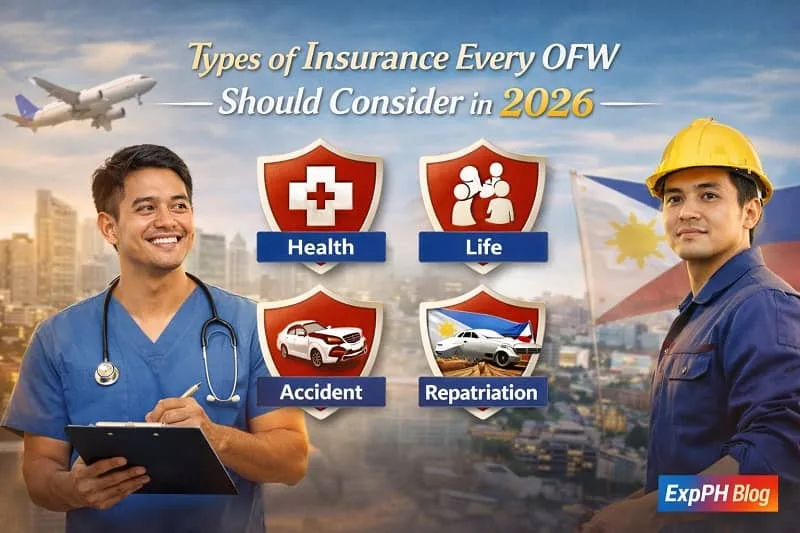

Types of Insurance Every OFW Should Consider in 2026

Not all insurance policies serve the same purpose. Understanding how each type works helps OFWs choose proper coverage without overpaying or leaving important risks unprotected. Knowing the role of every policy allows overseas workers to build balanced protection based on work conditions and family responsibilities.

Life Insurance for OFWs

Life insurance provides financial support to dependents if the policyholder passes away. For OFWs, this coverage is vital because families often rely on one income. Coverage amounts should match long term needs such as education, housing, and daily living costs. Term plans are affordable, while whole life includes savings features.

Health and Medical Insurance

Medical insurance is one of the most important forms of OFW insurance 2026. Some host countries offer basic healthcare, but access is often limited or tied to employment. Private international health insurance helps cover hospitalization, outpatient treatment, and mental health care. OFWs should confirm coverage both overseas and in the Philippines.

Accident and Disability Insurance

Many OFW jobs involve physical risk, especially in construction, manufacturing, caregiving, and maritime work. Accident insurance provides financial support if injury or disability occurs. It offers lump sum benefits that help replace lost income and cover recovery or rehabilitation expenses during periods of limited work ability.

Repatriation and Travel Insurance

Unexpected events like political unrest, health crises, or employer disputes may require emergency return to the Philippines. Repatriation insurance covers travel and medical evacuation costs during these situations. This protection ensures OFWs can return home safely without facing overwhelming expenses during emergencies.

Choosing the Right OFW Insurance Based on Your Situation

No single insurance policy fits every overseas worker. The best OFW insurance 2026 depends on job type, destination country, family responsibilities, and financial capacity. Understanding personal circumstances helps OFWs choose coverage that offers real protection without unnecessary costs or gaps in benefits.

For First Time OFWs

First time OFWs should focus on health and accident insurance for immediate protection while adjusting to a new work environment. Affordable term life insurance is also recommended early on to provide basic family security and peace of mind during the first overseas contract.

For Long Term or Returning OFWs

OFWs who have worked abroad for several years may benefit from higher life insurance coverage and expanded health plans. Policies that include retirement age extensions help support long term planning and allow a smoother transition back to permanent life in the Philippines.

For OFWs with Dependents

OFWs supporting children or elderly parents should consider insurance plans with family riders or separate dependent coverage. This approach helps ensure continuous care and financial support during medical emergencies, hospital stays, or unexpected income disruptions.

Common Mistakes OFWs Make When Buying Insurance

Understanding common mistakes helps OFWs avoid costly decisions when choosing insurance. Awareness allows overseas workers to select proper coverage based on real needs instead of assumptions, incomplete information, or rushed choices that may lead to financial problems later.

Many OFWs rely only on mandatory agency insurance, believing it provides full protection. Others choose policies based solely on low price without reviewing exclusions, coverage limits, or claim conditions. These decisions often result in unexpected expenses during emergencies.

Some OFWs fail to disclose medical history accurately, which may cause claim rejection later. Others forget to update or review policies after job changes or relocation. OFW insurance 2026 should be reviewed regularly, especially when income level or family responsibilities change.

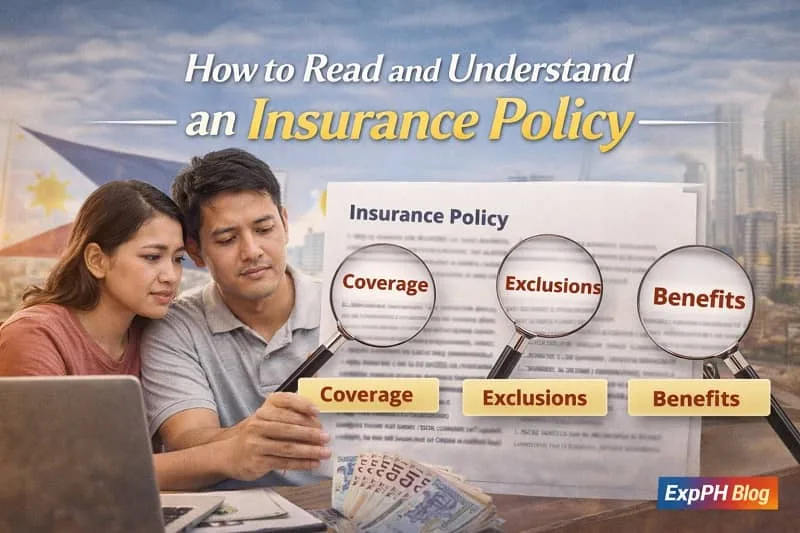

How to Read and Understand an Insurance Policy

Insurance documents can feel overwhelming, especially for first time buyers. Focusing on the most important sections makes policies easier to understand. Taking time to read and review details helps OFWs avoid confusion and ensures they know what protection they are actually receiving.

OFWs should always review coverage limits, exclusions, waiting periods, and claim procedures carefully. It is also important to confirm whether the policy applies worldwide or only in specific countries. Understanding these details helps prevent surprises during medical emergencies or claim filing.

If any part of the policy is unclear, OFWs should ask questions before signing. Clarifying details in advance is better than assuming coverage exists. Asking early helps avoid denied claims and ensures the policy truly meets personal and family protection needs.

Why Financial Literacy Matters When Choosing OFW Insurance

Insurance works best when supported by strong financial habits. OFWs who understand how money flows in and out of their budget are better prepared to maintain coverage without stress. Financial awareness helps prevent missed payments and long term policy lapses.

Learning budgeting, emergency fund management, and long term planning allows OFWs to choose insurance premiums they can sustain. These skills help protect daily living needs while keeping coverage active. Education plays a key role in making insurance decisions practical, confident, and aligned with personal goals.

Building Insurance Awareness Through Practical Learning

Many OFWs find insurance confusing simply because they were never taught how it works or how to compare policies properly.

Learning the basics of personal finance, insurance planning, and risk management can significantly improve decision making and prevent costly mistakes.

A helpful resource for OFWs who want to strengthen their financial knowledge is Udemy, where they can explore practical financial education courses that explain insurance concepts in clear, beginner friendly lessons designed for real life use.

Using education as a foundation helps OFWs avoid buying the wrong insurance and improves confidence when discussing policies with providers.

Insurance and Career Stability Go Hand in Hand

One often overlooked part of OFW insurance 2026 is the link between career stability and coverage choices. As work conditions improve, insurance planning becomes more effective. Stable employment helps OFWs maintain consistent premiums and avoid coverage gaps caused by income disruption.

Higher skills often lead to better job opportunities and improved benefits. With stronger negotiating power, OFWs may experience lower work risks and more predictable income. This stability can make insurance easier to maintain and more affordable over time.

Upskilling does not replace the need for insurance, but it supports long term financial security. Career growth strengthens earning ability, which helps OFWs sustain coverage while preparing for future goals and unexpected challenges.

How OFWs Can Balance Insurance Costs with Daily Expenses

Many OFWs worry that insurance premiums will reduce the amount they can send home. Balancing protection and daily expenses requires careful planning. Understanding income limits helps overseas workers maintain coverage without sacrificing essential family needs or personal living costs.

Prioritization is the key to managing insurance expenses. Health and accident coverage should come first since they address immediate risks. Life insurance follows once basic protection is secured. Optional add ons should only be considered when income is stable and monthly obligations are comfortably met.

Automated payments help prevent missed premiums and accidental policy lapses. Regular annual reviews allow OFWs to adjust coverage as income or responsibilities change. These simple habits make insurance easier to manage while supporting long term financial stability.

What to Do When Making an Insurance Claim Abroad

Making an insurance claim abroad can be stressful, especially when navigating unfamiliar systems and language barriers. Understanding the process in advance helps OFWs stay calm and organized during emergencies. Preparation reduces delays and improves the chances of a successful claim.

OFWs should keep digital copies of insurance policies, emergency contact numbers, and claim forms. Sharing basic policy details with trusted family members is also helpful. This preparation ensures quick access to important information when immediate action is required.

Choosing insurers that offer online support and international assistance can simplify the claims process. Access to customer service across time zones allows OFWs to receive guidance faster and avoid unnecessary confusion during urgent situations.

OFW Insurance Trends to Watch in 2026

Insurance providers continue adapting to changes in the global workforce. In 2026, many policies now offer flexible payment options, digital claims processing, and coverage that works both overseas and in the Philippines. These improvements make insurance easier to manage for mobile overseas workers.

Mental health coverage is gaining greater recognition among insurance providers. This shift is important for OFWs who face emotional strain, isolation, and long working hours abroad. Expanded coverage helps support overall well being and encourages workers to seek help without fear of high costs.

Preparing for the Future Beyond Employment Abroad

OFW insurance 2026 should continue even after overseas employment ends. Planning for coverage during retirement or permanent return to the Philippines helps prevent protection gaps. Early preparation ensures healthcare access and financial security remain stable during major life transitions.

Transition plans should include health insurance that remains valid in the Philippines and life insurance that supports long term family goals. Maintaining continuous coverage allows returning OFWs to focus on rebuilding life at home without worrying about unexpected medical or financial emergencies.

Final Thoughts on Choosing the Best OFW Insurance in 2026

Insurance is more than a requirement or a regular expense for overseas Filipino workers. It serves as protection, responsibility, and peace of mind while working far from home. Proper coverage helps secure income, supports access to healthcare, and reduces financial stress during emergencies. When chosen carefully, insurance allows OFWs to focus on their work and family goals without constant worry about unexpected risks.

The best OFW insurance 2026 is one that matches your work conditions, lifestyle, and family needs. It should adapt as income changes and responsibilities grow. By understanding risks, avoiding common mistakes, improving financial knowledge, and reviewing policies regularly, OFWs can protect what matters most while building a safer and more stable future for themselves and their loved ones.

Explore more practical guides related to OFW financial planning and protection:

- Best Investment Options for Filipinos Supporting OFW Income in 2026

- Common Financial Mistakes OFWs Should Avoid in 2026

- Best Low-Capital Businesses OFWs Can Start in 2026

- Best Financial Goals OFWs Should Set for 2026

- Best Passive Income Ideas for OFWs in 2026

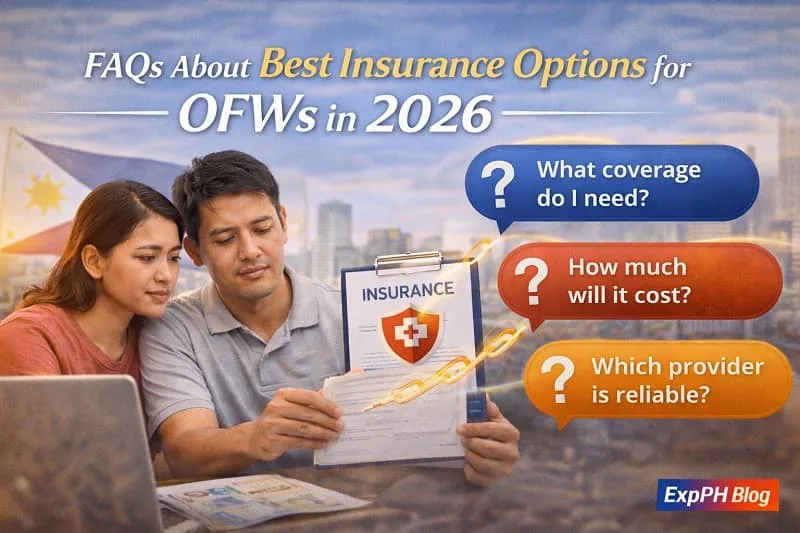

FAQs About Best Insurance Options for OFWs in 2026

What is the best insurance option for OFWs in 2026?

The best option depends on job type, country, and family needs, but most OFWs benefit from health, life, and accident insurance combined.

Is OFW insurance mandatory in 2026?

Yes, agency hired OFWs are required to have mandatory insurance, but voluntary private insurance is still recommended for broader and longer term protection.

Why is health insurance important for OFWs abroad?

Healthcare abroad can be very expensive, and health insurance helps cover hospital bills, treatments, and emergencies without draining savings or remittances.

Can OFWs buy insurance while already working overseas?

Yes, many insurers allow OFWs to apply online while abroad, as long as requirements, medical disclosures, and documentation are properly completed.

Does OFW insurance cover both overseas and Philippine use?

Some policies offer worldwide coverage, while others are country specific, so OFWs should confirm coverage validity in both locations before purchasing.

How much does OFW insurance usually cost?

Costs vary based on age, coverage type, and benefits, but basic OFW insurance plans are designed to be affordable with flexible payment options.

What happens if an OFW changes jobs or countries?

Some policies remain valid, while others require updates, so OFWs should inform their insurer immediately to avoid coverage gaps or claim issues.

Is life insurance necessary for single OFWs?

Yes, life insurance still helps cover debts, funeral costs, and future family responsibilities, even if the OFW is currently single.

How often should OFWs review their insurance policies?

OFWs should review insurance at least once a year or after major life changes, such as job shifts, marriage, or having dependents.

What is the biggest mistake OFWs make with insurance?

Relying only on mandatory insurance and not checking exclusions is the most common mistake, which can lead to unexpected costs during emergencies.

Test your knowledge about Best Insurance Options for OFWs in 2026 and see how prepared you are.

Results

#1. What is the main goal of OFW insurance 2026?

#2. Which insurance is most critical for OFWs abroad?

#3. Who requires mandatory insurance coverage?

#4. What insurance supports families if an OFW passes away?

#5. Which risk is common for labor intensive OFW jobs?

#6. Why should OFWs review insurance yearly?

#7. What mistake do many OFWs make?

#8. Which insurance helps during emergencies abroad?

#9. What helps OFWs choose better insurance?

#10. When should insurance planning start?

Your effort to learn today helps protect your future and your family.

We would love to hear from you. Please comment below and share your quiz experience or score with us.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: Best Insurance for OFWs 2026 What Families Should Have Today

Pingback: Best Retirement Plans for OFWs in 2026 Guide for OFW Future!