How to Build a Strong Financial Foundation Using OFW Income in 2026

Building a secure and stable future is one of the biggest goals of every Overseas Filipino Worker. Working abroad often comes with higher income, but higher income alone does not guarantee long-term financial security. Without a clear system, even a strong salary can disappear through poor spending habits, unmanaged debt, and lack of planning.

This guide is designed to help OFWs understand how to build a strong financial foundation using their hard-earned income in 2026. It focuses on OFW Financial Planning that is realistic, practical, and aligned with real OFW life situations such as contract-based work, family obligations, remittances, and future reintegration in the Philippines.

This is not about quick riches or risky shortcuts. This is about control, clarity, and confidence with your money so your years abroad truly lead to long-term stability.

Understanding the Importance of OFW Financial Planning

Financial planning is more critical for OFWs than for most workers because income abroad is often temporary. Contracts end, job markets change, and personal circumstances evolve. OFW Financial Planning helps turn temporary overseas income into permanent financial security.

A strong financial foundation allows you to:

- Handle emergencies without panic

- Support your family without sacrificing your future

- Prepare for life after overseas work

- Build assets instead of depending only on salary

Without planning, many OFWs reach the end of their contracts with little savings despite years of hard work. The goal is to avoid that situation by being intentional from the start.

Setting Clear Financial Goals Before Anything Else in OFW Financial Planning

Clear financial goals give structure and purpose to OFW Financial Planning. They guide how income is saved, spent, and protected. Without defined goals, money is often used reactively instead of strategically, making long-term stability harder to achieve despite strong overseas earnings.

Defining Short-Term, Medium-Term, and Long-Term Financial Goals Clearly

Breaking goals into time-based categories makes planning more practical and achievable. Each category supports a different stage of financial stability and helps OFWs balance immediate needs with future security.

- Short-term goals

Focus on building an emergency fund, paying high-interest debt, and stabilizing monthly remittances to reduce stress and improve cash flow. - Medium-term goals

Include saving for education, preparing business capital, or purchasing land or a home to create long-term value. - Long-term goals

Center on retirement planning, permanent return to the Philippines, and building reliable income sources beyond employment.

Writing goals down with clear amounts and timelines increases commitment. Saving one million pesos in five years creates stronger motivation than vague intentions.

Aligning Financial Goals With Your OFW Contract Timeline

OFW work is usually contract-based, so financial goals should match the length of each contract. A two-year contract should have clearly defined targets for savings, debt reduction, and skill development within that specific period.

This method keeps expectations realistic and progress measurable. It prevents frustration caused by distant or unclear goals and helps OFWs maximize every contract before renewal or transition.

Building a Solid Budget That Works Overseas in OFW Financial Planning

A strong budget is the backbone of OFW Financial Planning. It helps OFWs control spending, manage remittances, and prioritize future goals. A clear budgeting system turns overseas income into a structured plan that supports stability, flexibility, and long-term financial security.

Understanding Your Real Net Income Before Budgeting Decisions

Many OFWs focus on gross salary, but effective OFW Financial Planning begins with net income. Net income is what remains after taxes, housing, food, transportation, and required deductions. Knowing your true take-home pay allows accurate planning and removes guesswork from financial decisions.

Creating a Purpose-Based Budget for Better Money Control

Purpose-based budgeting assigns a clear role to every peso you earn. Instead of grouping expenses loosely, this method ensures income is directed toward both present needs and future security. It prevents savings and protection from being ignored when spending increases.

- Living expenses abroad

- Family support and remittances

- Savings and investments

- Insurance and protection

- Personal growth and skills

This approach strengthens discipline and keeps financial priorities clear throughout your overseas employment.

Establishing an Emergency Fund as Your First Safety Net in OFW Financial Planning

An emergency fund is a critical foundation of OFW Financial Planning. Overseas work involves risks like job loss, medical issues, or sudden return home. Having reserved cash protects your savings, avoids debt, and keeps long-term financial plans stable during unexpected situations.

Why Emergency Funds Matter More for OFWs Working Abroad

OFWs face higher uncertainty because employment depends on contracts and foreign regulations. An emergency fund provides immediate financial support during crises. It allows you to cover basic needs without borrowing money or selling investments that were meant for future security.

How Much Should OFWs Save for Emergencies

OFWs should aim to save three to six months of essential expenses. Those supporting families are safer with six months. Keep the fund liquid and easy to access, ideally in a secure bank account that is separate from daily spending.

Managing Debt Without Sacrificing Progress in OFW Financial Planning

Debt management plays a major role in OFW Financial Planning. While some debt can be manageable, uncontrolled borrowing slows progress. A clear strategy helps OFWs reduce financial pressure, protect savings, and ensure income growth supports long-term stability instead of constant repayment.

Prioritizing High-Interest Debt for Faster Financial Recovery

High-interest debt can quickly drain income and delay financial goals. Credit cards, informal loans, and payday borrowing should be addressed early. Making debt reduction part of your financial system allows OFWs to regain control and redirect money toward savings and future planning.

Avoiding Lifestyle Inflation While Working Overseas

As OFW income rises, spending often increases at the same pace. This habit limits savings and delays progress. Maintaining a simple lifestyle allows income growth to strengthen financial security while still enjoying reasonable comfort and stability abroad.

Protecting Your Income With Proper Financial Safeguards in OFW Financial Planning

Protecting income is a core part of OFW Financial Planning. Overseas work carries health and safety risks that can quickly erase savings. Proper safeguards help ensure that unexpected events do not destroy years of effort or derail long-term financial goals.

Understanding Health and Life Insurance Basics for OFWs

Health and life insurance protect both the OFW and the family left behind. Medical emergencies or accidents can happen without warning. Insurance coverage helps manage costs, prevents debt, and keeps long-term financial plans stable during difficult situations.

For official guidance on financial consumer protection and basic financial literacy in the Philippines, OFWs may refer to the Bangko Sentral ng Pilipinas Financial Education and Learning Program at https://www.bsp.gov.ph/Pages/InclusiveFinance/EFLP.aspx.

Growing Income Beyond Your OFW Salary in OFW Financial Planning

Relying only on OFW salary limits financial security. Contracts can end and global demand can shift without notice. In 2026, OFW Financial Planning should include income growth strategies that reduce dependence on physical overseas work and create more stable long-term earning potential.

Why Income Growth Matters for OFWs in 2026

Income growth protects OFWs from contract uncertainty and job changes. Depending on one employer increases risk. Developing additional income streams helps maintain financial stability, supports future goals, and prepares OFWs for transitions during and after overseas employment.

Investing in Skills That Increase Earning Power

Skills development is one of the most reliable ways to grow income. Learning high-demand skills opens access to better-paying roles, remote work, and freelance opportunities. This approach allows OFWs to increase earning power without relying only on location-based employment.

Using Online Learning to Strengthen Your Career

Online learning platforms offer practical and affordable ways to improve skills without leaving your job. Many OFWs use these platforms to learn freelancing, IT skills, digital marketing, bookkeeping, and other income-generating abilities.

A trusted option is Udemy, which offers flexible online courses that OFWs can take at their own pace. Courses in freelancing, digital skills, and professional certifications can support long-term income growth and strengthen OFW Financial Planning.

You can explore relevant courses here: https://www.udemy.com

Smart Saving Strategies for OFWs in OFW Financial Planning

Smart saving habits help OFWs turn steady income into long-term security. A clear saving system reduces impulse spending and builds consistency. When savings are treated as a priority rather than leftovers, financial goals become easier to reach and maintain over time.

Separating Savings From Spending Accounts

Mixing savings with daily spending makes it easy to use money meant for the future. OFWs should keep savings in a separate account to protect progress. Automating transfers adds discipline and removes the need to rely on constant self-control.

Saving With a Clear Purpose in Mind

Purpose-driven savings are easier to sustain because each goal has meaning. Labeling savings for education, housing, or business capital creates focus. This clarity improves motivation, builds discipline, and encourages consistent contributions even during busy or challenging periods abroad.

Understanding Basic Investment Principles in OFW Financial Planning

Investing plays an important role in long-term wealth, but timing matters. OFW Financial Planning works best when investments follow strong foundations. Proper preparation reduces risk, builds confidence, and ensures investment decisions support stability rather than creating unnecessary pressure or financial anxiety.

Investing Only After Building a Strong Financial Foundation

Emergency funds and basic protection should come before any investment activity. Investing too early can cause stress during emergencies. A solid foundation allows OFWs to stay invested during market changes without being forced to withdraw funds at the wrong time.

Avoiding Get-Rich-Quick Schemes and Risky Offers

OFWs are frequent targets of scams that promise fast profits. If returns sound unrealistically high, caution is necessary. Focus on investments you understand, with risks that match your comfort level and long-term financial goals.

Preparing for Life After Overseas Work in OFW Financial Planning

Planning for life after overseas employment is a vital part of OFW Financial Planning. Overseas work is temporary, but financial responsibilities continue. Preparing early helps OFWs transition smoothly, avoid income shocks, and build a stable lifestyle when returning to the Philippines permanently.

Planning Your Exit Strategy Early and With Purpose

Every OFW should plan ahead for the end of overseas work. This includes deciding where to live, how to earn income, and how to maintain daily expenses. A clear exit strategy gives direction and prevents financial stress during career transitions.

Reintegration With Financial Confidence and Stability

Returning home is easier when finances are well prepared. Adequate savings, strong skills, and reliable income sources provide independence. Financial readiness allows OFWs to reintegrate confidently, support their families, and adjust to life in the Philippines without pressure.

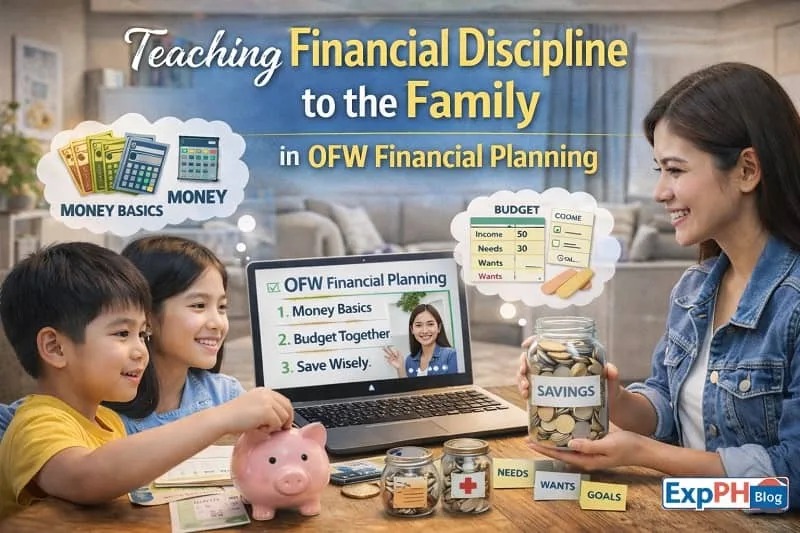

Teaching Financial Discipline to the Family in OFW Financial Planning

Family involvement plays a major role in successful OFW Financial Planning. Support from home should strengthen long-term goals rather than create pressure. Teaching discipline helps families understand limits, respect priorities, and protect the results of years of overseas work.

Aligning Family Expectations With Financial Reality

Family support is important, but it must remain sustainable. Open discussions about income limits and financial goals help prevent misunderstandings. Clear boundaries allow OFWs to support loved ones while still protecting savings and future plans without unnecessary stress.

Encouraging Financial Literacy at Home

Teaching basic financial habits at home helps preserve overseas income. Simple lessons on budgeting, saving, and spending build responsibility. When families understand money management, they become partners in financial progress rather than unintentional obstacles.

Common Mistakes OFWs Should Avoid in OFW Financial Planning

Many OFWs earn well but still struggle financially due to repeated mistakes. These habits weaken long-term stability and reduce the impact of overseas income. Recognizing and avoiding common errors helps strengthen discipline, protect earnings, and build a more secure financial foundation.

Frequent Financial Mistakes That Limit OFW Progress

Avoiding these mistakes allows OFWs to make better decisions and stay aligned with long-term goals. Each issue below can quietly drain income if not addressed early.

- Sending money without a clear budget

- Ignoring personal financial goals

- Relying only on salary income

- Falling for unverified investment offers

- Delaying planning until the final contract

Being aware of these patterns helps OFWs stay in control. Correcting them early supports stronger OFW Financial Planning and leads to lasting financial security.

Final Thoughts on OFW Financial Planning in 2026

Building a strong financial foundation using OFW income in 2026 requires intention, discipline, and consistent action. Overseas work offers higher earning potential, but income alone does not guarantee security. Only structured OFW Financial Planning can turn temporary contracts into long-term stability. When money is guided by clear goals and practical systems, OFWs gain control, confidence, and direction over their financial future.

By setting clear goals, managing income carefully, protecting against risks, developing valuable skills, and preparing early for life after overseas work, OFWs can turn years abroad into lasting security. Your income has power when used wisely. With the right plan, it can support your family today and sustain your future for many years ahead.

You may want to explore these related readings.

- Best Retirement Planning Tips for Filipinos With OFW Income in 2026

- Beginner’s Guide to Investing in the Philippines

- How to Set Realistic Financial Goals for 2026

- Best OFW Success Habits to Build in 2026

- OFW Life Planning Checklist for 2026

FAQs About OFW Financial Planning

What is the importance of OFW Financial Planning in 2026?

It helps OFWs turn temporary overseas income into long-term stability by guiding budgeting, saving, protection, and future planning aligned with contracts and family responsibilities abroad.

How can OFWs start building a financial foundation while working abroad?

Start by tracking net income, listing essential expenses, setting savings targets, and assigning every peso a clear purpose to balance needs, goals, and obligations effectively.

How much emergency fund should an OFW ideally have?

Save three to six months of essential expenses to handle job loss, emergencies, or sudden repatriation without debt or disrupting long-term financial plans stability goals.

What role does debt management play in OFW Financial Planning?

OFWs should prioritize high-interest debts first, avoid lifestyle inflation, and maintain consistent payments so income growth supports savings, protection, and future investments for long-term security.

Why is relying only on OFW salary risky?

It reduces reliance on a single contract, increases earning potential, supports career flexibility, and creates backup income options during job changes or market shifts globally.

How do skills and education support financial stability for OFWs?

Online courses allow OFWs to upgrade skills flexibly, qualify for higher-paying roles, and prepare for freelancing or remote work alongside overseas employment opportunities long-term sustainability.

Should OFWs invest while still working overseas?

Yes, investing should start only after emergency funds, insurance, and stable budgeting are established to reduce risk and avoid financial stress for OFWs abroad long-term.

What are effective saving strategies for OFWs?

Separate savings accounts, automate transfers, label goals clearly, and treat savings as mandatory expenses to prevent spending and maintain consistency over time abroad for OFWs.

How can OFWs manage family expectations about remittances?

By setting limits, explaining long-term goals, and promoting financial literacy, families can support sustainable remittances without harming the OFW’s future security plans savings stability goals.

What is the most important advice for OFWs planning finances in 2026?

Begin early, stay disciplined, review plans regularly, and focus on skills, protection, and savings so overseas income builds lasting financial confidence for OFWs in 2026.

Test your knowledge about OFW Financial Planning and see how well you understand building a strong financial foundation using OFW income in 2026.

Results

#1. What is the first step in OFW Financial Planning?

#2. Why is an emergency fund important for OFWs?

#3. How many months should an OFW emergency fund cover?

#4. Which expense should be prioritized first?

#5. Why should OFWs avoid lifestyle inflation?

#6. What makes OFW income risky long-term?

#7. What supports long-term income growth for OFWs?

#8. When should OFWs start investing?

#9. Why is family communication important in financial planning?

#10. What is the main goal of OFW Financial Planning?

Every step you take toward learning brings you closer to financial confidence and a stronger future.

Share your quiz experience and score in the comments. We would love to hear from you.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 10 Smart OFW Budget Adjustments to Make When Costs Increase.

Pingback: 7 Proven OFW Budgeting Tips to Beat Rising Living Costs 2026

Really insightful guide, thank you for breaking things down so clearly for OFWs who are serious about planning beyond just one contract. I’m curious how you view the balance between building a financial safety net and investing in mobility. For example, do you think it ever makes sense for an OFW who is already working remotely or planning a digital nomad path to prioritize relocation tools like international mobility consulting or premium services before fully reaching the “3–6 months emergency fund” target, or should those kinds of expenses always come only after the core foundation such as emergency fund, insurance, and debt reduction is completely in place?

Thank you for raising this thoughtful question. This is something many OFWs quietly struggle with, especially those exploring remote work or long term mobility.

In most cases, I strongly recommend building the core financial foundation first. That means completing at least three to six months of emergency savings, securing proper insurance, and reducing high interest debt. For contract based OFWs, income stability is never guaranteed, so protection must come before expansion.

That said, there are rare situations where mobility related expenses can be treated as an investment rather than a lifestyle upgrade. For example, if an OFW already has stable remote income, minimal debt, and at least a partial safety buffer, and the relocation expense directly increases earning capacity or access to better contracts, then it can be a calculated move.

The key question is this: Is the expense protecting income or increasing income, or is it simply upgrading lifestyle?

For most OFWs, foundation first, growth second remains the safest and most sustainable strategy. Once the safety net is solid, mobility becomes an opportunity rather than a financial risk.

Thank you again for bringing depth to the discussion.