Best Retirement Plans for OFWs in 2026

Planning for retirement is one of the most important financial responsibilities of an Overseas Filipino Worker. While working abroad offers higher income opportunities, it also comes with uncertainty, contract limits, health risks, and changing global job markets. This is why choosing the best retirement plans for OFWs in 2026 is not optional anymore. It is essential.

Many OFWs delay retirement planning because daily expenses, family support, and emergency needs take priority. However, the earlier an OFW prepares, the more secure and flexible their future becomes. Retirement is not only about old age. It is about financial freedom, peace of mind, and the ability to return home without fear of running out of money.

This in-depth guide will help you understand the best retirement plans for OFWs in 2026, how each option works, who it is best for, and how to combine multiple strategies for stronger long-term security. This article is written to educate real OFWs, not just to rank on search engines.

Why Retirement Planning Is Critical for OFWs in 2026

OFWs face a very different retirement reality compared to local workers. Most overseas jobs are contract-based, physically demanding, and dependent on global economic conditions. Unlike regular employment in the Philippines, many OFWs do not automatically receive pensions unless they take action themselves.

Several trends make retirement planning more urgent in 2026:

- Rising cost of living in the Philippines

- Increasing healthcare expenses as people age

- Limited working years abroad due to age limits or health

- Exchange rate fluctuations that affect savings value

- Family dependency that often continues after returning home

Without a clear retirement plan, many returning OFWs are forced to work again locally, rely on family support, or spend their savings too quickly. The goal of retirement planning is to prevent these situations and give you control over your future.

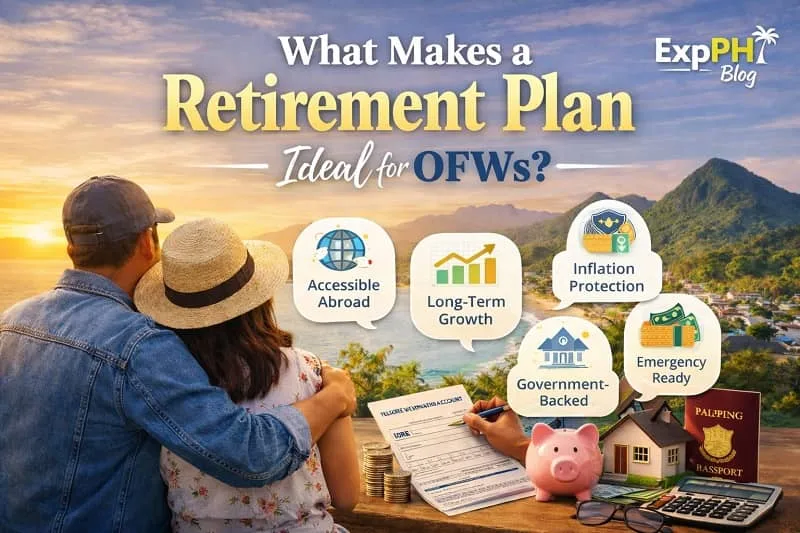

What Makes a Retirement Plan Ideal for OFWs

Not all retirement plans work well for overseas Filipino workers. The best retirement plans for OFWs are flexible, accessible from abroad, and designed for long-term financial security while accounting for the unique challenges of overseas employment.

The most effective OFW retirement plans usually include the following key features:

- Flexible contribution options

- Accessibility from abroad

- Long-term growth potential

- Protection against inflation

- Availability of funds during emergencies

- Government-backed or regulated when possible

An ideal OFW retirement plan should also be portable. This allows OFWs to continue contributing and managing their retirement savings regardless of their country of employment, job contract, or changes in work location.

Government-Backed Retirement Plans for OFWs

Government-backed retirement programs remain a trusted foundation for OFW retirement planning. These plans offer regulation, stability, and predictable benefits, making them suitable for long-term financial security. They are especially helpful for OFWs who prefer lower risk and structured contributions.

SSS Flexi Fund and SSS Pension for OFWs

The Social Security System is one of the strongest retirement pillars for OFWs. The SSS Flexi Fund is a voluntary savings option that allows overseas Filipinos to earn higher returns on top of their regular SSS contributions.

Key benefits of the SSS Flexi Fund include:

- Government-backed security

- Competitive interest rates compared to regular savings

- Option to withdraw funds before retirement if needed

- Tax-free earnings

OFWs who maintain consistent SSS contributions may qualify for monthly pensions upon retirement. SSS also provides disability and survivorship benefits, offering financial protection for both the member and their family.

For official contribution rules, eligibility, and updated policies, OFWs should refer directly to the Social Security System official website. This source is especially useful for confirming payment schedules, benefit computation, and recent program updates.

Pag-IBIG MP2 Savings Program

The Pag-IBIG Fund MP2 Savings Program is a strong retirement option for OFWs who want stable growth with low risk. It is a voluntary savings plan that usually offers higher dividends than regular Pag-IBIG savings.

MP2 works well for OFWs because it provides the following benefits:

- Five-year maturity period

- Lump sum or annual dividend payout options

- Government-backed program

- Tax-free dividends

This program is ideal for OFWs seeking medium-term retirement growth without heavy market exposure. It works best as part of a balanced retirement plan alongside pensions and long-term investments.

Private Retirement and Investment Options for OFWs

While government programs provide stability, private retirement options focus on growth and diversification. Combining both helps OFWs balance security with higher long-term returns. This approach reduces reliance on a single source and strengthens overall retirement preparation across different life stages.

Mutual Funds and UITFs

Mutual funds and Unit Investment Trust Funds allow OFWs to invest in professionally managed portfolios across stocks, bonds, and other assets. These options are suitable for long-term wealth building and help protect savings against inflation when chosen based on proper risk tolerance.

These investment options are suitable for OFWs who:

- Have long-term investment horizons

- Can tolerate moderate market fluctuations

- Want inflation-beating growth

Equity funds often suit younger OFWs with longer timelines, while balanced or bond funds are more appropriate for those approaching retirement who prefer stability and capital preservation.

PERA Investment Accounts

The Personal Equity and Retirement Account is a voluntary retirement savings program regulated by the government and managed by accredited private institutions. It is designed to encourage disciplined long-term investing with retirement as the primary goal.

PERA offers the following benefits:

- Tax incentives

- Long-term investment focus

- Designed specifically for retirement

Although still underutilized, PERA remains one of the most structured retirement vehicles for OFWs who are consistent, disciplined, and focused on long-term financial independence.

Real Estate as a Long-Term Retirement Asset

Many OFWs include real estate in their retirement plans because it can provide long-term value and stability. Property ownership may generate rental income or serve as a fully paid home after returning to the Philippines, reducing future living expenses.

Rental Properties for Passive Income

Rental properties in developing cities can provide steady monthly income during retirement. However, OFWs should carefully evaluate the responsibilities involved and avoid relying on property income alone without proper financial planning.

Important factors OFWs must consider include:

- Property management challenges

- Maintenance and vacancy risks

- Initial capital requirements

This approach works best when combined with liquid investments that cover emergencies and periods without rental income.

Retirement Home Planning

Owning a fully paid retirement home can significantly reduce long-term living costs. OFWs who plan early gain more flexibility in choosing locations, managing construction costs, and avoiding housing expenses during retirement years.

Insurance-Based Retirement Plans for OFWs

Insurance-based retirement plans serve two main purposes, financial protection and long-term savings. For OFWs, these products help manage risks such as illness or death while supporting structured savings that can supplement retirement income over time.

VUL Insurance Plans

Variable Universal Life insurance combines life protection with investment components. Although often misunderstood, VUL plans can work for OFWs who need insurance coverage while maintaining disciplined long-term savings through regular premium payments.

VUL plans are best suited for:

- OFWs with dependents

- Those who struggle with investment discipline

- Long-term policy holders

Traditional Endowment Plans

Endowment plans provide guaranteed payouts after a fixed term, offering predictability and lower risk. While returns are modest, these plans appeal to conservative OFWs who value certainty and stable benefits over higher but uncertain investment growth.

Skill-Based Retirement Preparation for OFWs

Retirement does not always mean completely stopping work. Many OFWs plan to shift toward lighter and more flexible income sources after returning home. Preparing skills early allows them to stay productive while maintaining financial stability during retirement years.

Why Skills Matter in Retirement Planning

Financial products alone may not provide enough protection throughout retirement. Practical skills create income resilience, especially when investment returns decline or unexpected expenses arise. Skills also give retirees more control over how and when they earn.

Skill-based income can:

- Supplement pensions and savings

- Reduce dependency on family

- Provide purpose and productivity in retirement

Learning High-Value Skills Before Retirement

OFWs who invest in skill development before retiring gain a strong advantage. Learning freelancing, online business, or financial management skills helps ensure a smoother transition from overseas employment to flexible and sustainable income sources.

Online Skill Training for Future Income Stability

This is where structured learning platforms become valuable. Online courses allow OFWs to prepare for post-retirement income while still working abroad.

A helpful resource for this is Udemy, which offers practical courses in freelancing, online business, personal finance, and digital skills that OFWs can use even after returning to the Philippines.

You can explore relevant courses on Udemy to help build future-ready skills that support long-term financial stability.

Learning skills alongside building retirement funds creates a more resilient and flexible retirement plan.

Building a Balanced Retirement Strategy for OFWs

The best retirement plans for OFWs do not rely on one solution alone. A balanced approach spreads risk and creates more reliable long-term security. Combining different income sources helps protect savings while supporting financial stability throughout retirement.

A strong OFW retirement strategy often includes:

- Government-backed pension or savings

- Private investments for growth

- Insurance for protection

- Property or rental income

- Skills for post-retirement earnings

This combination helps reduce financial risk and builds long-term stability, allowing OFWs to adapt to changing needs, market conditions, and life circumstances during retirement.

Common Retirement Mistakes OFWs Must Avoid

Even high-income OFWs can struggle with retirement planning when common mistakes are overlooked. Poor financial habits, delayed action, and lack of planning often reduce long-term security, regardless of income level or years spent working abroad.

Some of the most damaging retirement mistakes include:

- Relying only on savings accounts

- Delaying retirement contributions

- Supporting extended family without limits

- Not planning for healthcare costs

- Ignoring inflation impact

Avoiding these mistakes is just as important as choosing the right retirement plans. Awareness and discipline help OFWs protect their savings and build a more secure and sustainable retirement future.

How Early Should OFWs Start Retirement Planning

The best time for OFWs to start retirement planning was as early as possible. The next best time is now. Early action builds strong financial habits and gives retirement funds more time to grow steadily.

OFWs in their twenties and thirties benefit most from compounding growth and long investment horizons. Those in their forties and fifties should prioritize capital protection, income planning, and reducing financial risks as retirement approaches.

Regardless of age, consistent contributions and disciplined planning matter more than perfect timing. Taking regular action helps OFWs build confidence and financial stability throughout their working years and into retirement.

Retirement Planning Checklist for OFWs in 2026

This simple checklist helps OFWs stay organized and focused while preparing for retirement. Reviewing these items regularly ensures that savings, protection, and income plans remain aligned with long-term goals and changing life situations.

Use this checklist as a practical guide:

- MP2 or PERA investment in place

- Active SSS contribution or Flexi Fund enrollment

- Emergency fund equivalent to six months expenses

- Clear post-retirement income plan

- Skills development in progress

- Health insurance coverage

Completing these steps helps OFWs build a stronger and more secure retirement foundation.

Conclusion: Choosing the Best Retirement Plans for OFWs in 2026

Retirement planning is one of the most valuable commitments an OFW can make for themselves and their family. The best retirement plans for OFWs in 2026 are not about choosing a single product. They focus on building a complete system that supports long-term stability, flexibility, and financial confidence throughout different life stages.

By combining government-backed programs, private investments, insurance protection, real estate planning, and skill development, OFWs can create a retirement plan that adapts to changing needs. No matter where you are working today, starting now helps secure dignity, independence, and peace of mind for the years ahead.

Expand your reading with these related guides to deepen your retirement and financial planning knowledge as an OFW.

- Best Insurance Options for OFWs in 2026

- How OFWs Can Prepare for Life After Working Abroad in 2026

- Best Insurance Types Filipinos and OFW Families Should Have in 2026

- Best Home-Based Business Ideas for Returning OFWs in 2026

- Best Work-From-Home Opportunities for OFWs in 2026

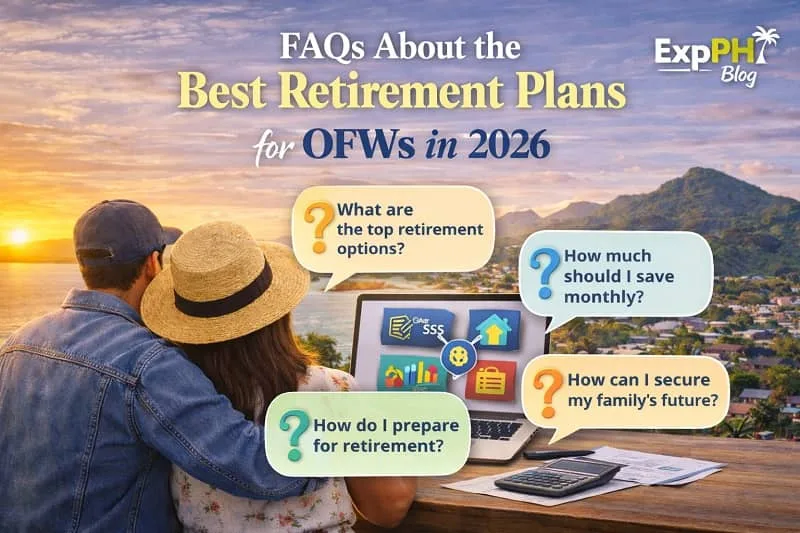

FAQs About the Best Retirement Plans for OFWs in 2026

What are the best retirement plans for OFWs in 2026?

The best retirement plans for OFWs in 2026 combine SSS or Pag-IBIG savings, private investments, insurance protection, and skills preparation for long-term income security.

Why should OFWs start retirement planning early?

Starting early allows OFWs to maximize compound growth, build consistent savings habits, reduce financial pressure later, and create more flexible retirement options over time.

Is SSS still a good retirement option for OFWs?

Yes, SSS remains a reliable option because it offers pension benefits, disability coverage, and voluntary programs like Flexi Fund designed specifically for overseas Filipino workers.

Can OFWs rely only on savings for retirement?

Relying only on savings is risky because inflation and rising living costs reduce purchasing power, making investments and structured retirement plans more effective long-term solutions.

Are private investments safe for OFW retirement planning?

Private investments can be safe when diversified properly, aligned with risk tolerance, and combined with government-backed programs to balance growth and stability.

What role does insurance play in OFW retirement planning?

Insurance provides financial protection against illness, accidents, or death, helping preserve retirement savings and protect dependents from unexpected financial burdens.

Is real estate a good retirement plan for OFWs?

Real estate can be effective if managed properly, providing rental income or a debt-free home, but it should complement, not replace, other retirement investments.

How can skills help OFWs during retirement?

Skills allow OFWs to earn flexible income after retirement, support small businesses or freelancing, and stay financially independent even without full-time employment.

What mistakes should OFWs avoid in retirement planning?

OFWs should avoid delaying contributions, ignoring inflation, relying on one income source, overspending, and failing to plan healthcare and emergency expenses.

How can OFWs build a balanced retirement plan?

A balanced plan includes pensions, investments, insurance, savings, and skill development, ensuring income stability, flexibility, and financial security throughout retirement.

Test your knowledge about retirement planning for Overseas Filipino Workers and see how prepared you are for the future.

Results

#1. What is the main goal of OFW retirement planning?

#2. Which government program offers pensions for OFWs?

#3. Which Pag-IBIG program suits long-term savings?

#4. Why is inflation a retirement risk?

#5. Which option provides diversified investments?

#6. What is PERA designed for?

#7. Why should OFWs develop skills early?

#8. Which asset can provide rental income?

#9. What mistake should OFWs avoid?

#10. What creates a balanced retirement plan?

We appreciate you investing time in learning about your future.

Smart planning today leads to a more confident tomorrow. Share your quiz experience in the comments and tell us which question made you think the most. Your feedback helps us improve our Learning Hub for fellow OFWs.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: Best OFW Retirement Planning Tips for Filipinos in 2026 Guide

Pingback: OFW Family Support: Best Ways to Help Families in 2026 Today

Pingback: Best Countries to Settle After OFW Life in 2026 Guide Tips.

Pingback: Best OFW Reintegration Program Plan for Returning OFWs in 2026

Pingback: Ultimate OFW Roadmap for a Better Future in 2026 | OFW Guide