Debt Management Strategies That Actually Work

Debt is one of the most common financial stressors today, especially for Overseas Filipino Workers who juggle family obligations, remittances, and long-term goals across borders. Many people search for quick fixes, but lasting financial stability comes from applying Debt Management strategies that are realistic, proven, and sustainable over time.

This guide breaks down debt management in a way that works for real people, not just ideal scenarios. Whether you are dealing with credit cards, personal loans, online lending apps, or overseas financial commitments, the principles remain the same. When applied consistently, debt management becomes a tool for freedom rather than a source of fear.

This article focuses on practical steps you can start today, common mistakes to avoid, and strategies that align with long-term financial health.

Understanding Debt Management and Why It Matters

Debt Management is not about avoiding debt completely. It focuses on controlling how debt influences income, decisions, and future plans. When applied properly, it reduces financial stress, improves cash flow, and restores confidence. It helps individuals make informed choices while protecting long-term financial stability.

What Debt Management Really Means

Debt management is the structured process of organizing, prioritizing, and repaying debts in a clear and realistic way. It involves budgeting, choosing effective repayment strategies, managing interest costs, and changing habits that cause repeated borrowing. The goal is control, not restriction.

For OFWs, debt management also involves:

- Managing multiple currencies

- Handling remittance responsibilities

- Balancing short-term family needs with long-term security

- Avoiding high-interest emergency borrowing while abroad

Debt management works best when actions are planned early rather than taken only during financial pressure.

Why Ignoring Debt Makes Things Worse

Ignoring debt does not solve the problem. Interest continues to increase, penalties build up, and financial stress grows. Over time, unmanaged debt can affect mental health, work focus, and family relationships. Delayed action often leads to fewer options and higher repayment difficulty.

Debt management allows you to:

- Reduce total interest paid

- Avoid legal or collection issues

- Improve creditworthiness

- Free up money for savings and investments

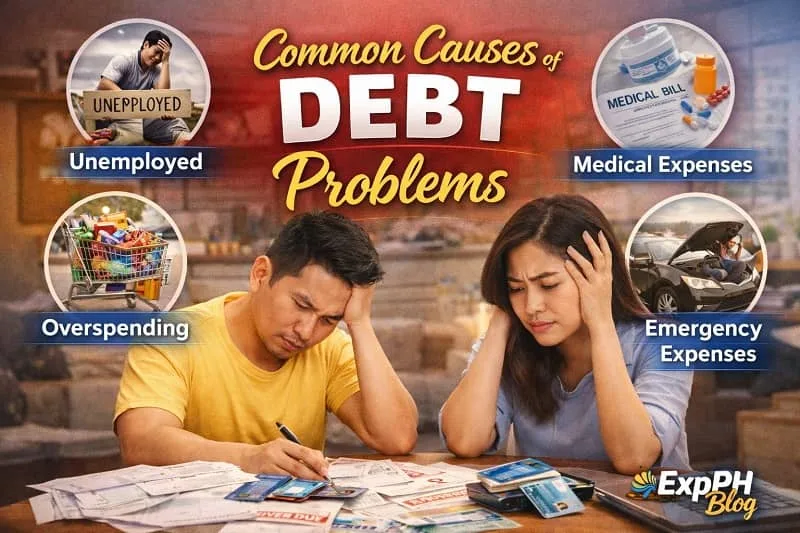

Common Causes of Debt Problems

Understanding why debt builds up helps address the real cause instead of only treating the symptoms. Debt often grows from daily decisions, financial habits, and lack of planning. Identifying these causes allows better debt management and prevents repeated borrowing over time.

Lifestyle Inflation

As income increases, spending often increases as well. This is common among OFWs who want to improve their family’s living conditions. Without clear limits, higher expenses slowly replace savings and lead to recurring debt that becomes difficult to control.

Emergency Expenses Without Savings

Unexpected medical costs, job interruptions, or family emergencies can force borrowing when no emergency fund is available. Without savings, even short-term problems turn into long-term debt, making recovery harder and increasing financial stress over time.

High-Interest Credit Products

Credit cards, salary loans, and online lending apps can trap borrowers in ongoing repayment cycles. High interest rates and short payment terms cause balances to grow quickly, making it harder to reduce debt even with regular payments.

Lack of a Clear Financial System

Many people earn enough income but lack a clear financial system. Without tracking expenses and income, spending becomes unclear. Small leaks add up over time, allowing debt to grow slowly until it becomes difficult to manage.

Core Principles of Debt Management That Actually Work

These core principles apply to everyone regardless of income level or location. Debt management succeeds when actions are consistent, realistic, and based on clear awareness. Following these foundations helps reduce stress, prevent setbacks, and create steady progress toward long-term financial stability.

Face the Numbers Honestly

Debt management begins with full clarity. List every debt with its balance, interest rate, due date, and required payment. Avoid guessing or ignoring details. Seeing the full picture reduces anxiety and allows smarter decisions based on facts instead of fear.

Stop Adding New Debt

Repayment plans fail when new debt continues to enter the system. Pause unnecessary borrowing and delay non-essential purchases whenever possible. Even a short break from borrowing can significantly improve progress and help existing payments reduce balances faster.

Build a Basic Safety Buffer

While paying debt, set aside a small emergency buffer. This protects you from borrowing when unexpected expenses appear. Even a modest amount creates stability, supports consistent repayment, and prevents setbacks that slow debt management progress.

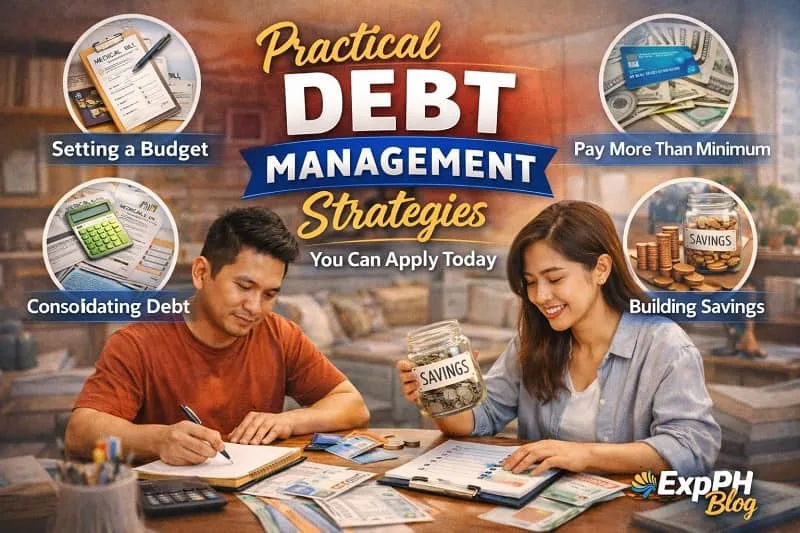

Practical Debt Management Strategies You Can Apply Today

Debt management works best when strategies are simple and easy to follow. Two proven methods stand out because they focus on behavior, consistency, and progress. These approaches help reduce overwhelm while creating a clear system for paying off debt steadily and sustainably.

The Debt Snowball Method

The debt snowball method focuses on motivation and consistency. It is designed to help people stay committed by creating visible progress early. This strategy works well for those who feel discouraged by long repayment timelines and need confidence boosts to continue.

How It Works

- List debts from smallest to largest balance

- Pay minimums on all debts

- Focus extra money on the smallest balance

- Roll payments forward as each debt is cleared

Why It Works

Early wins create momentum and confidence. Each cleared debt builds motivation, making it easier to stay consistent. Over time, this emotional boost supports long-term success and helps people avoid quitting before meaningful progress is achieved.

The Debt Avalanche Method

The debt avalanche method prioritizes saving money on interest. It is ideal for people who prefer a logical and cost-focused approach. This strategy rewards patience by reducing the total amount paid over time while still maintaining structured repayment.

How It Works

- List debts from highest to lowest interest rate

- Pay minimums on all debts

- Focus extra money on the highest interest debt

Why It Works

By focusing on debts with the highest interest first, this method reduces the total interest paid over time. Payments work more efficiently, helping balances decrease faster. Both repayment methods are effective. The best choice is the one you can follow consistently without causing stress or burnout.

Budgeting as the Backbone of Debt Management

Without a budget, debt management becomes guesswork. A clear budget shows where money goes and where adjustments are needed. It creates structure, improves control, and supports consistent repayment. Budgeting turns financial decisions into planned actions rather than reactions to daily expenses.

Creating a Realistic Budget

A realistic budget reflects actual spending habits, not ideal ones. It works best when based on honest numbers and regular review. The goal is balance, not restriction, so the budget remains sustainable and supportive of long-term debt management goals.

Include:

- Fixed expenses

- Variable expenses

- Debt payments

- Savings contributions

For OFWs, budgets should also consider remittance schedules and possible exchange rate changes to avoid shortfalls.

Zero-Based Budgeting for Debt Focus

Zero-based budgeting gives every peso or dollar a specific purpose. This method works well during aggressive debt repayment phases because it limits waste. By assigning income intentionally, it improves accountability and reduces financial leaks that slow debt management progress.

Managing Debt While Supporting Family as an OFW

Debt management becomes more complex when family support is involved. OFWs often balance remittances with personal financial goals. Without clear planning, obligations can grow faster than income. A structured approach helps support loved ones while protecting long-term stability.

Setting Financial Boundaries Kindly

Supporting family does not require sacrificing your future security. Clear and respectful communication sets realistic expectations. Share your debt management goals and timelines honestly. This approach builds understanding and reduces pressure while keeping financial responsibilities balanced and sustainable.

Prioritizing Long-Term Security

Debt freedom makes it easier to provide support consistently over time. Short-term sacrifices often create long-term stability. By focusing on future security, OFWs can avoid repeated borrowing and build a stronger financial foundation for both themselves and their families.

Avoiding Guilt-Based Borrowing

Many OFWs borrow because of guilt or emotional pressure. Debt management requires decisions based on sustainability rather than emotion. Choosing long-term stability over short-term relief helps prevent deeper debt and protects overall financial health.

Negotiating With Creditors and Lenders

Many people avoid negotiating with creditors, but it can be effective when handled properly. Open communication shows responsibility and willingness to pay. When done early, negotiation may reduce pressure, improve payment terms, and make debt management more manageable over time.

When Negotiation Makes Sense

Negotiation works best when your financial situation changes and payment becomes difficult. Being honest and proactive increases your chances of success. Lenders are more responsive when borrowers communicate early instead of waiting until payments are missed.

Negotiation works best when:

- You are experiencing financial hardship

- You have a consistent payment history

- You act early rather than react late

What You Can Request

When negotiating, focus on realistic adjustments that support repayment. Clear requests show seriousness and responsibility. Many lenders are more flexible than expected when approached respectfully and with a clear plan.

You may ask for:

- Lower interest rates

- Payment restructuring

- Temporary relief options

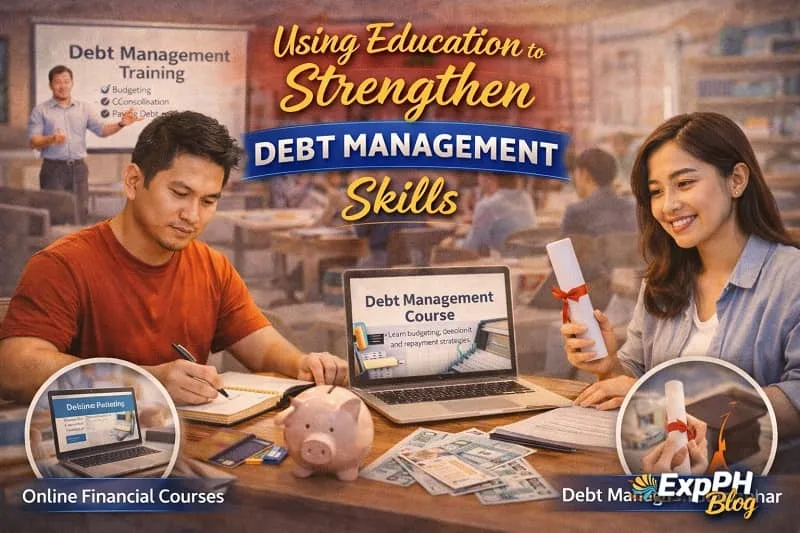

Using Education to Strengthen Debt Management Skills

Debt management improves when you understand money behavior, not just numbers. Education helps explain why decisions are made and how habits form. With better knowledge, people gain control, reduce mistakes, and apply debt management strategies with confidence instead of relying on trial and error.

Why Financial Education Matters

Many debt problems come from habits and beliefs rather than income level. Learning personal finance principles builds awareness and consistency. Education helps people replace harmful patterns with healthier ones, making debt management easier to maintain and more effective over the long term.

A Structured Learning Resource That Helps

Some people learn best through guided instruction instead of scattered advice. Structured learning provides clarity and direction. It connects budgeting, debt repayment, and behavior into one system, which helps learners apply debt management strategies in real situations without feeling lost.

Guided Learning for Debt Management Skills

If you prefer a step-by-step approach, a practical personal finance course on Udemy can explain budgeting systems, debt payoff methods, and money psychology in one place. Courses break complex topics into clear actions, which is helpful for OFWs managing finances across countries. Learning at your own pace supports real progress when paired with action.

Avoiding Debt Management Scams and False Promises

Not all debt solutions are legitimate. Some target people who feel stressed or desperate about money. Knowing how to spot warning signs protects you from losing more funds and keeps your debt management efforts focused on real solutions that support long-term financial stability.

Red Flags to Watch Out For

Be cautious when a service makes unrealistic claims or avoids clear explanations. These warning signs often indicate scams or unreliable programs that can worsen your situation instead of helping resolve debt problems.

Be cautious if a service:

- Promises instant debt elimination

- Asks for large upfront fees

- Discourages direct contact with creditors

- Lacks transparency

Verifying Financial Advice

Always verify financial advice using trusted sources. In the Philippines, the Bangko Sentral ng Pilipinas offers consumer education resources with verified guidance on loans, credit, and borrower rights. Using official information helps you make safer decisions and avoid misleading debt management offers. Relying on credible institutions protects you from misinformation.

Tracking Progress and Staying Motivated

Debt management is a long-term process that requires patience and consistency. Progress may feel slow at times, but steady effort builds results. Tracking improvement helps maintain focus, reduces frustration, and reinforces positive habits that support lasting financial change.

Measuring What Matters

Tracking the right indicators helps you see real progress beyond monthly payments. Clear measurements show improvement even when balances move slowly. This keeps motivation strong and supports better decision-making throughout your debt management journey.

Track:

- Total debt balance

- Interest saved

- Number of accounts cleared

- Cash flow improvements

Progress is not always linear, but consistent effort compounds over time.

Celebrating Small Wins

Acknowledging small milestones builds motivation and confidence. Celebrate progress in simple ways without adding new expenses. When achievements feel visible and rewarding, it becomes easier to stay committed and continue applying debt management strategies consistently.

What to Do After You Become Debt-Free

Debt management does not end when balances reach zero. This stage marks a new phase of financial responsibility. The habits built during repayment should continue, helping protect progress, support long-term goals, and prevent falling back into unnecessary debt.

Redirecting Payments to Savings and Investments

After clearing debt, redirect previous payments toward building wealth. Using the same discipline helps strengthen financial security and future readiness. Consistent contributions create stability and replace debt habits with positive money practices.

Use the same discipline to build:

- Emergency funds

- Retirement savings

- Education funds

- Small investments

Preventing Future Debt Relapse

Avoiding future debt requires ongoing awareness and structure. Maintaining healthy habits keeps finances stable and reduces risk during unexpected events. Debt freedom works best when supported by clear systems and mindful decisions.

Maintain:

- Budgeting habits

- Emergency buffers

- Conscious spending decisions

Debt freedom is a foundation that supports lasting financial growth rather than a final goal.

Conclusion: Debt Management Is a Skill You Can Master

Debt Management is not about being perfect with money. It is about building awareness, creating structure, and staying consistent over time. Anyone can improve their financial situation by applying proven strategies with patience and realistic expectations. Progress comes from small, repeated actions that slowly replace stress with control and clarity. When debt is managed intentionally, financial decisions become easier and more confident.

For OFWs and local earners alike, debt management offers stability, confidence, and peace of mind. The journey may take time, but each step forward reduces pressure and increases freedom. Starting is the most important move. With the right system, education, and mindset, debt management becomes a practical and lasting life skill.

These posts continue the learning experience.

- Understanding Personal Finance in the Philippines

- Best Saving Strategies for Filipinos With Overseas Income in 2026

- Simple Financial Systems Small Businesses Should Set Up Early

- Best Business Niches Returning OFWs Can Focus on in 2026

- How OFWs Can Avoid Debt Traps Abroad

FAQs About Debt Management

What is debt management and why is it important?

Debt management is organizing, prioritizing, and paying debts systematically. It helps reduce financial stress, avoid penalties, improve cash flow, and support long-term financial stability.

Which debt management strategy works best for beginners?

Beginners often succeed with the debt snowball method because small early wins build motivation, consistency, and confidence, making long-term debt repayment easier to maintain.

How long does debt management usually take to work?

Debt management results vary by income, debt size, and consistency. Most people see progress within months, while full debt freedom often takes several years.

Can debt management work with a low income?

Yes. Debt management focuses on prioritization, budgeting, and behavior. Even small, consistent payments combined with expense control can steadily reduce debt over time.

Is debt management better than debt consolidation?

Debt management focuses on habits and repayment structure, while consolidation combines debts. Effectiveness depends on discipline, interest rates, and whether spending behavior improves.

Should I stop saving while paying off debt?

No. A small emergency fund supports debt management by preventing new borrowing during unexpected expenses, which helps maintain repayment momentum and financial stability.

How does debt management help Overseas Filipino Workers?

Debt management helps OFWs balance remittances, foreign income, and family support while controlling debt, managing exchange risks, and protecting long-term financial goals.

Can debt management improve my credit score?

Yes. Consistent payments, reduced balances, and lower credit utilization through debt management can gradually improve your credit score over time.

What mistakes should I avoid in debt management?

Avoid ignoring debts, adding new loans, skipping budgets, relying on quick fixes, and quitting early. Consistency and realistic planning are essential for success.

When should I seek professional help for debt management?

Seek help when debts feel overwhelming, payments are missed, or stress affects daily life. Financial education or counseling can restore structure and confidence.

Test your understanding of practical debt management strategies

Results

#1. What is the main goal of debt management?

#2. Which method focuses on small wins first?

#3. What should you do before repaying debt?

#4. Why is budgeting essential for debt management?

#5. Which habit prevents new debt?

#6. What is a common debt management mistake?

#7. Which debt costs most long term?

#8. Why should OFWs prioritize debt management?

#9. What helps maintain motivation during repayment?

#10. What should replace debt payments after payoff?

Thank you for taking the time to learn with us.

Your commitment to learning is a powerful step toward financial confidence. Comment below and share your quiz experience with us.

A Filipino web developer with a background in Computer Engineering. Founder of ExpPH Blog and ExpPH Business Guide, creating practical content on OFW guidance, business, finance, freelancing, travel, and lifestyle. Passionate about helping Filipinos grow, he shares insights that educate, empower, and inspire readers nationwide.

Pingback: 7 Smart Ways to Survive an OFW Financial Emergency Abroad.